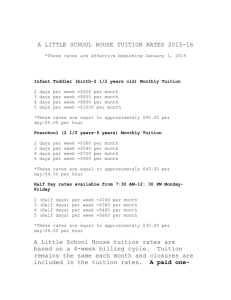

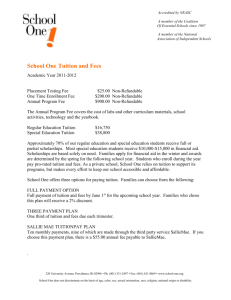

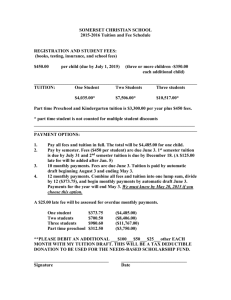

Existing Description:

advertisement

University Description-Tuition Remission: Full-time faculty, and staff members and their family members (to include same-sex domestic partners) are eligible to participate in the Tuition Remission Plan after 90 days of consecutive full-time employment with JHU. The 90day waiting period is waived for professional development computer training courses. It can also be waived for other courses for full-time faculty members if the supervisor or department head certifies that the course is a requirement of the job. The plan is limited to part-time studies and covers tuition costs of the courses offered by JHU’s academic divisions. The maximum amount available to support staff for the calendar year is $5,250 for the family and within that amount $2625 for dependents. Employees are eligible for 100% remission for both credit (up to a family total of $5,250 per calendar year) and non-credit professional development courses (for which there is no dollar limit), and 80% remission for eligible, non-credit personal enrichment courses. The specific amount available to dependents on a per course/term/quarter varies by academic division, but in general ranges from $50 to 50%, up to $2625 per year for credit courses. Additional Information: As determined by the Federal Government, $5,250 is the maximum tuition benefit an employer is allowed to contribute to tax-free tuition for an employee. Any other tuition benefit above $5,250, such as scholarship support, is considered taxable income by the Federal Government. Any form of tuition payment which comes from the University will be considered a tuition benefit UNLESS the tuition is paid directly from a sponsored research or training grant account. New and continuing part-time students who are faculty will be taxed at the end of each academic term if the amount of tuition benefits exceeds $5250. The additional tax will be deducted directly from paychecks. Tuition remission payments over $5,250 between January 1 and March 31 will result in tax withholdings beginning April 30 through June 30. Tuition remission payments over $5,250 between April 1 and June 30 will result in tax withholdings beginning July 31 through September 30. Tuition remission payments over $5,250 between July 1 and September 30 will result in tax withholdings beginning October 30 through December 31. Tuition remission payments over $5,250 between October 1 and December 31 be directly adjusted as of December 31 and reflected on the W-2 for that calendar year. Tax Liability: All Jr. Faculty who register as part-time students are subject to tax liability on tuition remission. The IRS considers any support that is not a sponsored account as “tuition remission.” It is the student’s responsibility to monitor their use of tuition remission; however, it is particularly important that their tuition charges are applied accurately or their income will be taxed. Students are provided this information on the GTPCI website at http://www.jhsph.edu/gtpci/_doc/TaxInfo.doc. Examples for 2007-08: o A continuing PhD student is promoted to faculty. The student must register for a minimum of 3 credits per term ($728/credit) and plans to take no additional coursework. NEW TAX YEAR 3rd term = $2184 - tuition is covered by tuition remission 4th term = $2184 - tuition is covered by tuition remission 1st term = $2184 - The limit of tuition benefits of $5250 is reached. The remaining $1302 is covered by the SPH and is taxable income 2nd term = $2184 - $2184 is covered by the SPH and is taxable income o The same student described above applied for a K23 and writes tuition support into the grant. If all tuition is paid for by the K23 there would be no tax liability. o A faculty member is in the MHS program part-time (faculty members in the full-time program are not eligible for tuition remission). The tuition cost is covered by tuition remission and SOM departmental support (not coming from a training grant). Tuition is based on 9 credits/term, but would increase by $728/credit for each additional credit up to 12 credits. The MHS program is 70 credits total. First year 1st term = $6552 - The limit of tuition benefits of $5250 is reached. The remaining $1302 is covered by the SPH and is taxable income 2nd term = $6552 - $6552 is covered by SPH and is taxable income END OF TAX YEAR 3rd term = $6552 - The limit of tuition benefits of $5250 is reached. The remaining $1302 is covered by the SPH and is taxable income 4th term = $6552 - $6552 is covered by SPH and is taxable income Second year 1st term = $6552 - $6552 is covered by SPH and is taxable income 2nd term = $6552 - $6552 is covered by SPH and is taxable income END OF TAX YEAR 3rd term = $6552 - The limit of tuition benefits of $5250 is reached. The remaining $1302 is covered by the SPH and is taxable income 4th term = $6552 - $6552 is covered by SPH and is taxable income o A PhD student is promoted to faculty the July before his/her second year. Second year students are required to take 5 additional courses to include the design of clinical trials. Second year 1st term = $2184 for Design of Clinical Trials - tuition is covered by tuition remission 2nd term = $2184 for a 3 credit course - tuition is covered by tuition remission END OF TAX YEAR 3rd term = $4368 for Two 3 credit courses – tuition is covered by tuition remission 4th term = $2184 for a 3 credit course - The limit of tuition benefits of $5250 is reached. The remaining $1302 is covered by the SPH and is taxable income Third year 1st term = $2184 for 3 credits thesis research - $2184 is covered by SPH and is taxable income 2nd term = $2184 for 3 credits thesis research - $2184 is covered by SPH and is taxable income END OF TAX YEAR