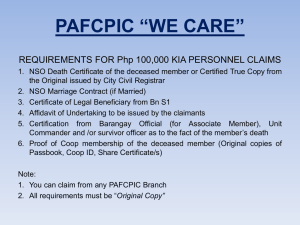

Lsn 18:

advertisement

Lesson 18 Electronic Payment Systems Overview • Data Transaction Systems • Securing the Transaction • Real World Examples Data Transaction Systems • Stored Account Systems – Modeled after existing electronic payment systems such as credit/debit card transactions – New way of shifting funds electronically over the internet (Paving Cow Paths) • Stored Value Payment Systems – Use bearer certificates much like hard cash – Bearer certificates reside within PCs or smart cards Stored Account Systems • Uses existing infrastructure for transactions • Actual monetary value never leaves bank • Accounting in the future through clearing houses and settlement systems • Hallmarks are: – High accountability – Traceability Stored Account Systems(2) • Payment systems have defined their own secure technologies • 1995: $13 trillion, in 3 billion transactions by 4 clearing houses • Fed Reserve Fedwire transfers $1 trillion/day • Fraud exists now but risk management models in place Stored Account Systems(3) • Protocols for supporting credit card types of transactions have been defined and implemented for E-commerce – First Virtual’s Internet Payment System – Cyber Cash’s Secure Internet Payment System – Secure Electronic Transaction (SET) • Many new technologies emerge daily • Security and convenience will rule the market place--it’s a balancing act Stored Value Payment Systems(SVPS) • Attempts to replace cash with electronic equivalent….E-Cash – No More Cow Paths • Instantaneous transfer of value, does not require bank approval • Security stakes are much higher than stored account systems • Attributes: absence of control and auditing SVPS(2) • Possible to counterfeit E-Cash • Typically used in small-value transaction – Small value transaction market = $8 trillion • Lack of privacy bothers some • Finding new cow paths not easy SVPS(3) • Author says: “most exciting, innovative, and risk forms of accepting payment” • Replaces currency with digital equivalent • Value placed directly on hardware tokens such as PCs or Smart Cards • Goal: have the advantages of hard currency systems over an electronic medium Attributes of Hard Currency ADVANTAGES • Not easily traceable • Instantaneous payment • No bank interference • • • • • DISADVANTAGES Costly to transport Costly to protect Easily lost or stolen Can be forged Parties must be in close proximity to exchange SVPS Pros/Cons Pros • Instantaneous (no approval needed) • Potentially Anonymous (traceability hard) • Supports low-value payment Cons • Secret key from one can be used for many • Secret key extraction makes counterfeit money indistinguishable for ECash • SVPS must strike balance between privacy and tracking illicit activity How E-Cash Works • E-Cash stored in an electronic device, called a hardware token – Secure processor and non-volatile memory • Consumers load money into token – Token’s value counter is incremented – Or Value loaded as register-based cash & electronic coins • Payment can be made on-line or off-line E-Cash Online Payment • Purchaser deals directly with seller’s hardware token device • Bank must be an intermediary – Allows for traceability • The H/W devices must be interoperable Off-line Payment • Buyer’s H/W token interfaces with seller’s device – IR, dial-up modem, or the Internet • Sellers device increases by transaction amount • Buyers’s device decreases by transaction amount • Safeguards needed to prevent “counter” malfunction • E-Cash ultimately must be sold back to issuing bank E-Cash Representation • A value stored in a counter of a H/W token (aka register-based) • From of cryptographic tokens called electronic coins Register Based Basic unit = 1 cent Token cntr = 10000 Token value = $100.00 E-Coin System “A Purse” Cents = count + digital signature $ = count + digital signature 5$ = count + digital signature Token value is sum of all Securing E-Cash • Security concerns for SV PS>> SAPS – Main reason: lack of traceability fraud potential • Main concern: potential to illegally add value to the H/W token • Physical Attacks on H/W token • Protocol based attack that mimics a paying device Physical Attacks Physical • An attempt to alter non-volatile memory – Device needs to be shielded so its tamper resistant – or device needs to be tamper evident Protocol Attacks Protocol • Device counter illegally incremented by “fake” paying device – Secure authentication needed to ensure “fakes” don’t work – Best way is for both devices to share a symmetric cryptographic key – All devices do not use a master key – Secret key = master key + device unique ID Protocol Attacks(2) • Key must be resistant to replay attacks – Wiretap captures key and “replays” the session – Challenge/Response systems can thwart replay attacks • Gives motive for the token bearer to recover secret key – Greed is a powerful sin Alternative Approach • PKE is an alternate – Compromise of public key will not allow reconstruction of secret key – Response to challenge is digital signature • Disadvantage is that token cannot contain public keys for all paying devices • Advantage is ability to prove that accumulated value is legit – Digital signatures from paying devices authorize the accumulated values Securing the Transaction WEB Protocols • SSL: provides secure channel between Web clients and Web servers – Layered approach--remember protocol stack – Secures channel by providing end-to-end encryption of the data – Prevents “easy” packet sniffing • S-HTTP: application level protocol Protocol and Security: SSL NOT SECURE SECURE HTTP SMTP FTP HTTP SSL TCP TCP IP IP Protocol and Security: SHTTP NOT SECURE HTTP SECURE HTTP Security TCP TCP IP IP Securing the Transaction(2) • Certificate Authority (CA) – Endorses identity of the Web server (or user) – No assurance of the quality of Web content – Users implicitly trust any sites that come loaded in their browser The Little Yellow Lock = Warm Fuzzy Secure Payment Protocols (SPP) vs WEB Protocols • SPPs provide a method to assure a merchants payment • SPPs provide consumers assurance of credit card confidentiality • Web protocols (like SSL) leave payment details up to the merchant • Web protocols do not assure merchant will safeguard credit card number Real World Examples • First Virtual • Cybercash • Secure Electronic Transactions (SET) • Others First Virtual(FV) • WWW.fv.com--circa 1994 • Does not use cryptography or secure communications • Based on exchange of email messages and customer honesty • Protocol I simple • 1996: 180,000 buyers, 2650 merchants FV IN ACTION(1) First Value 1. Establish acct-$2 with VISA/MC 0. FV Merchant Setup 6. VPIN, Transaction via email 2. Virtual PIN 3. Request Product 4. Send VPIN? Customer 5. VPIN SENT FV Merchant FV IN ACTION(2) SEVERAL DAYS LATER First Value 3. MC/VISA Charge 1. Transaction Confirmation? 3. Or Return product 2. Yes, No, Fraud Customer FV Merchant CyberCash • Cybercash is a downloadable applications software • Consumers must generate public/private key pair based on RSA encryption technology • Merchants must also install CyberCash Library • Software free to stimulate acceptance • Future: could be integrated into browsers • More to come…CyberCoin, and E-Cash Soln CyberCash(2) • Uses Cryptography to protect transaction data during a purchase (does not use SSL) • Provides a secure protocol for credit card purchases over the internet • Uses existing back-end credit card infrastructure for settling payment • Payment details of credit card transaction are specified and implemented in the protocol CyberCash(3) Merchant’s Perspective • There is no separate back-office system for batch processing card transaction • Payment assured for each transaction before product sold – Much like point-of-sale(POS) credit card transactions in physical stores CyberCash(4) • Credit card number is protected--even from merchants • Card number encrypted with CyberCash public key • Only consumer, cybercahs and bank sees the credit card number CYBERCASH IN ACTION Customer 2. Go E-Shopping, Request Product Merchant 3. Invoice Sent 5. Send Payment Info 1. Register Credit Card 4a. Select Cybercash Pay button in browser 4b. Select Credit card from 6a. Strip Order Form 6b. Digitally Sign Info E-wallet 4c. Encrypt payment CYBERCASH info with CyberCash Public Key 4d. Digitally Sign Payment BANK info BANK CYBERCASH IN ACTION Customer 2. Go E-Shopping, Request Product Merchant 3. Invoice Sent 5. Send Payment Info 7. Transmit Payment info 8. Decrypt payment info & verify signatures Bank EDI CYBERCASH 9. Brokering 20 SECONDS TOTAL 10. Approval/Deny 9. Brokering BANK Card Holder BANK Secure Electronic Transaction (SET) • SET is an emerging open standard for secure credit card payments over the internet • Created by Mastercard and Visa • Specifies the mechanism for securely processing internet-based credit card orders • Does not specify the implementation • Does not specify the shopping or order process for ordering goods, payment selection, and the platform or security procedures SET Security Assurances • Confidentiality -- secures payment info • Data integrity -- uses digital signatures • Client Authentication -- uses digital certificates: identity plus public key • Merchant authentication -- uses digital certificate SET Steps 1. The customer opens an account with a certificate authority. 2. An issuing authority, like a bank, issues a digital certificate authenticating a customer. 3. Other third-party merchants also receive their digital certificate when they open their transaction accounts. 4. The customer places an order. SET Steps 5. Customer verifies the merchant’s digital certificate . 6. Customer sends encrypted purchase details. 7. When the merchant receives the order, the customer’s own digital certificate is checked for authenticity as well. SET Steps 8. The merchant then returns its own certificate, order details, customer payment information, and the bank’s digital certificate back to the bank to be used to authenticate the transaction. 9. The bank will then verify the merchant certificate and order information. 10. The bank will digitally sign and return an authorization back to the merchant. 11. When these transactions are finished, the order is completed. SET IN ACTION 4. Place Order 5. Merchant Certificate Sent Customer Merchant 6. Send encrypted purchase details w/ Certificate 2. Buyer Opens Acct 1. Merchant receives Digital Certificate 3. Buyer receives Digital Certificate BANK 7. Sends order to Bank w/ customer payment info & digital certificate SET IN ACTION 4. Place Order 5. Merchant Certificate Sent Buyer Merchant 6. Send encrypted purchase details w/ Certificate 2. Buyer Opens Acct 9. Bank digitally signs & sends auth to merchant 3. Buyer receives Digital Certificate 7. Sends order to Bank w/ customer payment info & digital certificate 10. ORDER COMPLETE BANK 8. Bank verifies merchant certificate and order info SET Summary • • • • Large industry backing Supports credit card transactions on-line Does not support debit card payments Does not address stored-value payment solutions • Does not use SSL, but it could • Implementations: – Cybercash – RSA Data Security’s: S/PAY Other Examples • DigiCash’s e-cash: stored-value cryptographic coin system • CyberCoin--CyberCash’s payment system for on-line commerce – Designed for small-value payments • Smart Cards – Conditional Access for Europe (CAFÉ) – Mondex – Visa Cash Summary • Data Transaction Systems – Stored Account Systems – Stored Value Payment Systems • Securing the Transaction – SSL, S-HTTP and Secure Payment Protocols (SPP) • Real World Examples – FV, CyberCash, SET, E-Cash, and others