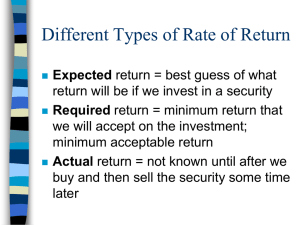

Historical Rates of Return - Kian

advertisement

Week 2 GD31403 Basic Performance Analysis Concepts What Is An Investment? • A current commitment of $ for a period of time in order to derive future payments that will compensate for: – The time the funds are committed (time value of money) – The expected rate of inflation – Uncertainty of future flow of funds (risk premium) Risk and return are 2 fundamental concepts in investment. 1-2 Required Rate of Return The minimum rate of return to compensate investors for the time, the expected rate of inflation and the uncertainty of the return. 1-3 Historical Rates of Return (1) Return over a Holding Period Holding Period Return (HPR) Ending Value of Investment HPR Beginning Value of Investment Holding Period Yield (HPY) HPY= HPR-1 *100 1-4 Historical Rates of Return Assume that you invest $200 at the beginning of the year and get back $220 at the end of the year. What are the HPR and the HPY for your investment? HPR = $220/200 = 1.1 HPY = (HPR – 1) * 100 = (1.1 -1) * 100 = 10% 1-5 Historical Rates of Return Annual Holding Period Return (Annual HPR) Annual HPR HPR 1n Annual Holding Period Yield (Annual HPY) Annual HPY= Annual HPR-1 *100 1-6 Historical Rates of Return Your investment of $250 in Stock A is worth $350 in two years, while the investment of $1000 in Stock B is worth $750 over the same holding period. What are the annual HPRs and the annual HPYs on these two stocks? Stock A Annual HPR = HPR1/n = ($350/$250)1/2 = 1.1832 Annual HPY = (Annual HPR – 1)*100 = 18.32% Stock B Annual HPR = HPR1/n = ($750/$1000)1/2 = 0.866 Annual HPY = (Annual HPR – 1)*100 = -13.4% 1-7 Historical Rates of Return When converting HPY to an annual basis, we assume a constant annual yield for each year. Stock A HPY = [($350/$250)–1]*100 = 40% (over 2 years) Annual HPY = [(1+0.40)1/2 – 1]*100 = 18.32% Ending Value = $1 * (1.1832)(1.1832) = $1.40 The annual yield assumes investor earns the same 18.32% return for the second year (compounded). 1-8 Historical Rates of Return Your investment of $100 in Stock C is worth $112 over a six-month holding period. What is the annual HPY on this stock? What is the implicit assumption in the calculation? HPY = [($112/$100)–1]*100 = 12% (over 6 months) Annual HPY = [(1+0.12)1/0.5 – 1]*100 = 25.44% Ending Value = $1 * (1.12)(1.12) = $1.2544 The annual yield assumes investor earns the same 12% for the second six-month (compounded). 1-9 Historical Rates of Return (2) Average/Mean Historical Returns The assumption of constant annual yield for each year is not realistic. Over the holding period of several years, investors will likely get different annual rates of return for an investment. How do you measure the mean/average annual return? 1-10 Historical Rates of Return Single Asset Arithmetic Mean Return (AM) n AM = å HPY i=1 n Geometric Mean Return (GM) ( )( ) ( ) 1n GM= éë 1+ HPY1 1+ HPY2 ... 1+ HPYn ùû -1 1-11 Historical Rates of Return Suppose you invested $100 three years ago and it is worth $110.40 today. The information below shows the annual ending values and HPR and HPY. This example illustrates the computation of the AM and the GM over a three-year period for an investment. Year 1 2 3 1-12 Beginning Value 100 115 138 Ending Value 115.0 138.0 110.4 HPR HPY 1.15 1.20 0.80 15% 20% -20% Historical Rates of Return n AM = å HPY i=1 n 0.15 + 0.20 - 0.20 = = 0.05 = 5% 3 GM= éë(1+ HPY1 ) (1+ HPY2 ) ...(1+ HPYn ) ùû -1 1n = éë(1+ 0.15) (1+ 0.20 ) (1- 0.20 ) ùû -1 13 = 1.03353 -1 = 0.03353 = 3.353% AM versus GM: Which one should we use? 1-13 Historical Rates of Return Suppose you invested $50 in a stock, and the price increases to $100 at the end of year 1. However, the stock is worth $50 at the end of year 2. Compute the AM and the GM over a 2-year period for the stock. Year 1 2 1-14 Beginning Value 50 100 Ending Value 100 50 HPR HPY 2.00 0.50 100% -50% Historical Rates of Return n AM = å HPY i=1 n 1- 0.50 = = 0.25 = 25% 2 ( )( = éë(1+1) (1- 0.50)ùû ) ( ) 1n GM= éë 1+ HPY1 1+ HPY2 ... 1+ HPYn ùû 12 -1 -1 = 1-1 = 0% AM versus GM: which one is more sensible? 1-15 Historical Rates of Return AM versus GM When rates of return are the same for all years, the AM and the GM will be equal. When rates of return are not the same for all years, the AM will always be higher than the GM. The AM is best used as an “expected value” for an individual year The GM is the best measure of an asset’s long-term performance as it measures the compound annual rate of return. 1-16 Historical Rates of Return Portfolio 1-17 The HPY is referred to as the value-weighted mean rate of return Expected Rates of Return • In previous examples, we discussed realized historical rates of return. • In contrast, an investor would be more interested in the expected return on a future risky investment. • An investor determines how certain the expected rate of return on an investment by analyzing estimates of possible returns (by assigning probability values). 1-18 Expected Rates of Return • These probabilities are typically subjective estimates • From Business Statistics, you learned that there are 3 approaches to assign probability: – Classical approach – Relative frequency – Subjective approach 1-19 Expected Rates of Return n E(R i ) (Probabilit y of Return) (Possible Return) i 1 [(P1 )(R 1 ) (P2 )(R 2 ) .... (Pn R n )] n ( Pi )( Ri ) i 1 1-20 Expected Rates of Return Scenario 1: The investor is absolutely certain of a return of 5% (risk-free investment) 1.00 0.80 E ( Ri ) = 0.05 = 5% 0.60 0.40 0.20 0.00 -5% 1-21 0% 5% 10% 15% Expected Rates of Return Scenario 2: Investors expect 3 possible returns based on different economic conditions (risky investment) 1.00 0.80 0.60 0.40 0.20 0.00 (10%,0.70) ( -20%,0.15) -30% 1-22 -10% ( ) E Ri = 0.07 = 7% ( 20%,0.15) 10% 30% Expected Rates of Return Scenario 3: Risky investment with ten possible returns 1.00 0.80 0.60 E ( Ri ) = 0.05 = 5% 0.40 0.20 0.00 -40% -20% 0% 1-23 20% 40% Expected Rates of Return • Since Scenario 1 and Scenario 3 provide the same rate of return (5%), which one would you invest? • It is generally assume that most investors are risk averse- ceteris paribus, they will select the investment that offers greater certainty (less risk). 1-24 Risk of Expected Return • Risk refers to the uncertainty of an investment; therefore the measure of risk should reflect the degree of the uncertainty. • The risk of expected return reflect the degree of uncertainty that actual return will be different from the expected return. • The common measures of risk are based on the variance and the standard deviation of the estimated distribution of expected returns. 1-25 Risk of Expected Return Variance 2 Probability * Possible Return-Expected Return n i 1 n = Pi Ri E Ri 2 i 1 • Variance measures the dispersion of possible returns around the expected returns • The larger the variance, the greater the dispersion of expected returns, and the greater the risk. 1-26 2 Risk of Expected Return Standard Deviation Variance 2 • Standard deviation is the square root of the variance • Why standard deviation is the preferred measure of total risk? • For variance, the unit is the square of the unit attached to the original observation. In the case of returns, the variance will be “% squared”. • The unit associated with the standard deviation is the unit of the original data. For returns, the standard deviation will be “%”. 1-27 Risk of Expected Return • For your practice, you can try this website 1-28 Risk of Expected Return 1-29 Risk of Expected Return • For comparing alternative investments, the coefficient of variation (CV) is more suitable. • CV, a measure of relative variability, indicates the risk per unit of expected return. Coefficient of Variation CV = 1-30 Standard Deviation of Expected Returns Expected Rate of Return i E R Historical Rates of Return Which one of the following 2 stocks is riskier? Expected Return Standard Deviation Stock A 0.07 0.05 Stock B 0.12 0.07 • By comparing the standard deviation (absolute variability), Stock B appears to be riskier. • But Stock B has higher returns 1-31 Risk of Expected Return CVA 0.05 = 0.714 0.07 CVB 0.07 = 0.583 0.12 The CV shows that Stock B has less relative variability or lower risk per unit of expected return. 1-32 Risk of Historical Rates of Return To measure the risk for a series of historical rates of returns, the same variance and standard deviation are used. The only difference is that we consider the historical holding period yields (HPY). For illustration, see Textbook (Brown and Reilly, 2009), pp.28-29. 1-33 Determinants of Required Returns • Three Components of Required Return: – The time value of money – The expected rate of inflation – The risk premium • Complications of Estimating Required Return – A wide range of rates is available for alternative investments at any time. – The rates of return on specific assets change dramatically over time. – The difference between the rates available on different assets change over time. 1-34 Determinants of Required Returns (1) The time value of money – An investor would demand the real risk-free rate (RRFR) as a compensation for deferring the use of money in current period. – RRFR assumes no inflation. – RRFR assumes no uncertainty about future cash flows. – RRFR is influenced by the long-run real growth rate of the economy. 1-35 Determinants of Required Returns (2) The expected rate of inflation – An investor would demand the rate of return to include compensation for the expected rate of inflation. – The nominal risk-free rate (NRFR) that prevails in the market are determined by RRFR, the expected rate of inflation and conditions in the capital market (supply and demand). NRFR 1 RRFR * 1 Expected Rate of Inflation 1 1-36 Determinants of Required Returns (3) Risk Premium – Most investors require higher rates of return on investments if they perceive that there is any uncertainty about the expected rate of return. – The increase in the required rate of return over the NRFR is the risk premium (RP). The risk premium can be related to fundamental factors (fundamental risk) OR systematic market risk (beta). 1-37 Determinants of Required Returns – Fundamental risk comprises business risk, financial risk, liquidity risk, exchange rate risk, and country risk. – Systematic risk refers to the portion of an individual asset’s total variance attributable to the variability of the total market portfolio. RP = f (Business Risk, Financial Risk, Liquidity Risk, Exchange Rate Risk, Country Risk) OR RP = f (Systematic Risk) 1-38 Determinants of Required Returns Risk Premium and Portfolio Theory – From a portfolio theory perspective, the relevant risk measure for an individual asset is its co-movement with the market portfolio (systematic risk or beta). – Individual assets have variance that is unrelated to the market portfolio, known as unsystematic risk. – Unsystematic risk is unimportant because it is eliminated in a large diversified portfolio. 1-39 Relationship Between Risk & Return The Security Market Line (SML) – It shows the relationship between risk and return for all risky assets in the capital market at a given time. – Investors select investments that are consistent with their risk preferences. Expected Return Security Market Line NRFR The slope indicates the required return per unit of risk Risk 1-40 (fundamental risk or systematic risk) Relationship Between Risk & Return • Movement along the SML – When the risk of an investment changes due to a change in one of its risk sources, the expected return will also change, moving along the SML. Expected Return SML NRFR 1-41 Movements along the curve that reflect changes in the risk of the asset Risk (fundamental risk or systematic risk) Relationship Between Risk & Return • Changes in the Slope of the SML – When there is a change in the attitude of investors toward risk, the slope of the SML will also change. – If investors become more risk averse, then the SML will have a steeper slope, indicating a higher risk premium for the same risk level. Expected Return R m’ New SML Original SML Rm NRFR Risk 1-42 (fundamental risk or systematic risk) Relationship Between Risk and Return • Changes in Market Condition or Inflation – A change in the RRFR or the expected rate of inflation will cause a parallel shift in the SML. – When nominal risk-free rate increases, the SML will shift up, implying a higher rate of return while still having the same risk premium. Expected Return New SML Original SML NRFR' NRFR 1-43 (fundamental risk or systematic risk) Risk