CERTIFIED FINANCIAL PLANNER CERTIFICATION

PROFESSIONAL EDUCATION PROGRAM

Investment Planning

Session 3

Types & Measurements of

Risk, Standard Deviation,

Beta, CAPM

©2015, College for Financial Planning, all rights reserved.

Session Details

Module

2

Chapter(s) 1, 2, 3

LOs

2-3

Calculate a weighted average return. Also

calculate the standard deviation and mean

return of a single asset, and understand how

the range of returns is calculated within one,

two, and three standard deviations.

2-4

Calculate coefficient of variation, and

understand its application.

2-8

Calculate required return using the capital

asset pricing model (CAPM), and understand

its application.

3-2

Risk

• Standard deviation: variability

• Beta: volatility

Total Risk

Standard Deviation

(Variability)

Systematic Risk

Beta

(Volatility)

Unsystematic Risk

3-3

Standard Deviation (Normal Distribution)

M (mean/average return) = 10%

σ (standard deviation)

= 15%

68% of returns

95% of returns

99% of returns

-3 σ

-2 σ

-1 σ

- 35%

- 20%

- 5%

Mean Return

10%

+1 σ

+2 σ

+3 σ

25%

40%

55%

2-4

Standard Deviation

• For normally distributed returns, calculate the standard

deviation range, add and subtract the standard

deviation amount from the mean return.

Example: Mean return of 10%, Std deviation of 15%

• One standard deviation: 10 + 15 = +25, and

10 – 15 = – 5

• Two standard deviations: 25 + 15 = +40, and

– 5 – 15 = – 20

• Three standard deviations: +55 to -35

3-5

Standard Deviation Concepts

• Normal distribution

• Skewness (security

•

•

•

returns are positively

skewed)

Kurtosis

Leptokurtic

Platykurtic

3-6

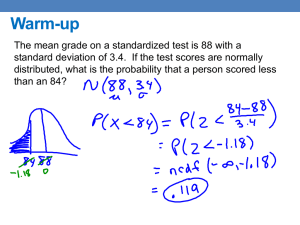

Standard Deviation Question

Scorpio Inc. has a mean return of

19%, and a standard deviation of

25.

What is the probability that the

stock will have a return greater

than 19% if the returns are

normally distributed?

3-7

Standard Deviation Question

Libra Inc. has a mean return of

11%, and a standard deviation

of 9.

Assuming the returns are

normally distributed, what is the

probability that the stock will

have a return greater than

20%?

3-8

Standard Deviation of a Single Asset

Use the calculator!

(rn r)

2

n 1

3-9

Calculating Standard Deviation

Single Asset (2)

• Formula #4 on diagram

• Calculation is simple on

the 10BII+ or 12C

Assume Acme Industries has

the following annual returns:

• + 15%

• + 22%

• - 7%

• + 10%

What is the standard deviation and mean return?

3-10

Calculating Standard Deviation

Single Asset (2)

Keystrokes are:

1, SHIFT, P/YR

15, ∑+

22, ∑+

7, +/-, ∑+

10, ∑+

SHIFT, 8

(g, “.” on 12C)

Answer = 12.36

For the mean return the keystrokes would be:

SHIFT, 7

(g, “0” on 12C)

Answer = 10%

3-11

Coefficient of Variation

Risk per unit of return

CV

σ

x

3-12

Coefficient of Variation Example

CV(A) = 6%/10% = 0.60

CV(B) = 9%/12% = 0.75

B has a higher mean, but also has a higher CV, which

means you take higher risk per unit of return.

Asset A

Asset B

Std Dev.

6%

9%

Mean.

10%

12%

Remember that you can easily calculate both standard

deviation and mean return for a single asset with your

financial calculator, as we did previously.

3-13

Beta Coefficients

• Measures the volatility of a stock (or portfolio)

•

relative to the market (a benchmark); so, the

greater the correlation, the more accurate beta

becomes.

Since R-squared measures systematic risk, it

can be used to determine beta

reliability; generally you are looking

for an R-squared of 70 or higher

in order for beta to be considered

reliable.

β

3-14

Beta

Beta of 1 means the asset has the same

volatility as the benchmark.

What would be the approximate price movement

of the Acme Fund if it has a beta of .85, and the

benchmark it is being compared to has a return of

15%?

Answer: 15% x .85 = 12.75%

What if Acme’s beta were 1.25?

Answer: 15% x 1.25 = 18.75%

3-15

Weighted Average Using Beta

What is the weighted beta of the following portfolio?

• $40,000 in AAA, beta of 1.2

• $20,000 in TTT, beta of 0.9

• $15,000 in ZZZ, beta of 0.8

Shortcut on 10BII+ calculator:

1.2, INPUT (ENTER on 12C)

40,000, ∑+

.9, INPUT

20,000, ∑+

.8, INPUT

15,000, ∑+

SHIFT, 6 (g, 6 on 12C)

Answer = 1.04

3-16

The Capital Asset Pricing Model

• CAPM also has a micro component that looks at

•

individual stock returns – the Security Market

Line – SML

This micro component is also used to help value

stocks

r rf (rm rf )β

3-17

The Capital Asset Pricing Model

The risk-free rate is 3.5%, and the market’s

expected return is 8%. Your stock has a beta

of 1.1.

What is the required return?

• r = 3.5 + (8.0 – 3.5)1.1

• r = 3.5 + 4.95

• r = 8.45

What is the market risk premium?

• 4.5% (8.0 – 3.5)

3-18

Required Return Calculations

What is the required return for the following

securities? The risk-free rate is 4%, and the

market return is 8%.

Fund

Beta

Triad

0.9

Triangle

1.1

Trapeze

2.0

Tango

1.4

Tangent

1.0

Required

Return

3-19

Question 1

Jake wants to know the beta coefficient for his portfolio of

stocks, shown below:

Current Market

Value

Beta

Alto Associates

$33,000

1.1

Bolero Enterprises

$12,500

1.0

Cactus Co.

$45,000

0.9

Dire Straights Int’l

$29,000

1.6

Stock

What is the beta coefficient for Jake’s portfolio?

a. 1.14

b. 1.19

c. 1.23

d. 1.28

3-20

Question 2

Triad Industries has a mean return for the

past five years of 12%, with a standard

deviation of 9%.

Assuming the returns are evenly distributed,

what is the probability that Triad will have a

return greater than 21%?

a. 3%

b. 12%

c. 16%

d. 24%

3-21

Question 3

Your client has narrowed his choice down to the following

three mutual funds, and wants your opinion concerning

which one to choose based on the fund that will provide the

lowest amount of risk per unit of return.

Fund

Mean

Return

Standard Deviation

ABC

8%

12

DDD

10%

14

EFG

7%

10

Which fund should your client choose?

a. Fund ABC

b. Fund DDD

c. Fund EFG

3-22

Question 4

A mutual fund you are considering has a beta of

0.75, a standard deviation of 11, a correlation

coefficient of .90 with the Russell 2000, an Rsquared of .65 with the S&P 500, and an

expected return of 12%.

Which one of the following is the fund’s

coefficient of variation?

a. .92

b. 1.09

c. 1.15

d. 1.25

3-23

Question 5

The current return of the market is 11%. The

current market risk premium is 7%, and the

risk-free rate is 4%.

If the beta of your stock is 1.1, what is your

required return?

a. 7.30

b. 11.70

c. 12.10

d. 16.10

3-24

CERTIFIED FINANCIAL PLANNER CERTIFICATION

PROFESSIONAL EDUCATION PROGRAM

Investment Planning

Session 3

End of Slides

©2015, College for Financial Planning, all rights reserved.

0

0