2010-06-29-qw-ny-Appel

advertisement

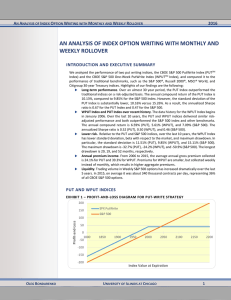

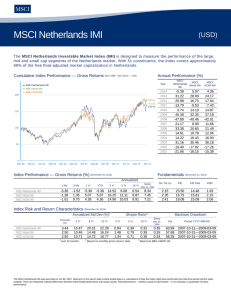

Active Asset Allocation Strategies Using ETFs Marvin Appel, MD, PhD CEO, Appel Asset Management Corp. Great Neck, NY mappel@appelasset.com Outline • Update relative strength strategies from my 2005 presentation to QWAFAFEW – Growth vs value – SPX vs EAFE—extended to include emerging markets • Covered call writing– Not all ETFs are created equal. Concept of relative strength • Divide index1 by index2. These indexes may reflect price or total return. • Rising ratio means index1 (numerator) is stronger. • Falling ratio means index2 (denominator) is stronger. • Relative strength leadership does not tell you whether either or both indexes are showing profits or losses. 6 5.5 5 4.5 index 1 index 2 4 3.5 3 2.5 2 1.5 1 1 2 3 4 5 6 7 time period 1.1 Index 1 divided by index 2 1 Rising = index 1 stronger Falling = index 2 stronger 0.9 0.8 0.7 Index 2 peak relative strength 0.6 0.5 1 2 3 4 5 6 7 Hypothetical ideal relative strength switching model 9 index 1 index 2 ideal switch 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 time period 1.1 Index 1 divided by index 2 Index 2 peak relative strength 1 Rising = index 1 stronger Falling = index 2 stronger 0.9 0.8 0.7 model in index 1 model in index 2 0.6 0.5 1 2 3 4 5 6 7 Recognizing new trends in relative strength 10 9 8 7 6 5 4 3 2 1 0 40% drop 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Growth versus value model • Select value and growth benchmarks for either large or small caps (eg: Russell 2000 value and growth indexes) • Calculate the monthly total return indexes and find the ratio as of the last day of each month. • Look for 10% reversals in the ratio to define new long term trends. Trend-following strategy: large-cap value versus large-cap growth Russell 1000 Indexes and switching strategy, 1979-2010 (total returns) 1000 Russell 1000 Value Index: 12%/year, 56% drawdown Russell 1000 Growth Index: 10.2%/year, 62% drawdown Source: Mutual Fund Expert as of 5/31/2010 1/1/09 7/1/07 1/1/06 7/1/04 1/1/03 7/1/01 1/1/00 1/1/97 7/1/95 1/1/94 7/1/92 1/1/91 7/1/89 1/1/88 7/1/86 1/1/85 7/1/83 1/1/82 7/1/80 1/1/79 100 7/1/98 Switching strategy: 12.9%/year, 50% drawdown History of value/growth model signals for large cap (Russell 1000) Indexes 1.9 1.7 1.5 Russell 1000 Value / Growth Rising = value stronger Falling = growth stronger 1.3 1.1 0.9 0.7 0.5 1/31/79 Model in value Model in growth 7/23/84 1/13/90 7/6/95 12/26/00 6/18/06 Trend-following strategy: small-cap value versus small-cap growth 10000 Russell 2000 Value Index: 13.5%/year, 55% drawdown Russell 2000 Growth Index: 8.9%/year, 63% drawdown Switching strategy: 14.3%/year, 58% drawdown 1000 Source: Mutual Fund Expert as of 5/31/2010 5/4/09 10/4/07 3/4/06 8/4/04 1/4/03 5/3/01 10/3/99 3/3/98 8/3/96 1/3/95 5/2/93 3/2/90 8/2/88 1/2/87 5/1/85 10/1/83 3/1/82 8/1/80 1/1/79 100 10/2/91 Russell 2000 Indexes and switching strategy, 1979-2010 (total returns) History of value/growth model signals for small-cap (Russell 2000) Indexes 4.5 4 3.5 3 Russell 2000 Value / Growth Rising = value stronger Falling = growth stronger 2.5 2 1.5 1 Model in value 0.5 Model in growth 0 1/31/79 7/23/84 1/13/90 7/6/95 12/26/00 6/18/06 Foreign (developed country) versus U.S. stock model • Use MSCI EAFE as the benchmark for foreign stocks and S&P 500 as the U.S. benchmark. • Calculate the ratio of EAFE / S&P 500 (priceonly data) on the last day of each month. • A new trend is defined by a 15% reversal in relative strength. MSCI U.S. versus EAFE 7,500.000 750.000 Aug 02, 2009 Jul 02, 2007 Jun 02, 2005 May 02, 2003 Apr 02, 2001 Mar 02, 1999 Feb 02, 1997 Nov 01, 1992 Oct 01, 1990 Sep 01, 1988 Aug 01, 1986 Jul 01, 1984 Jun 01, 1982 May 01, 1980 Apr 01, 1978 Mar 01, 1976 Feb 01, 1974 Jan 01, 1972 Dec 01, 1969 75.000 Jan 02, 1995 MSCI EAFE: 9.8%/year, 56% drawdown MSCI US: 9.4%/year, 51% drawdown Switching model: 10.4%/year, 58% drawdown Source: MSCI Barra (http://www.mscibarra.com/products/indices/international_equity_indices/gimi/stdinde)x/performance.html) History of EAFE / U.S. switch model 3.5 3 Rising = foreign stocks stronger Model in foreign stocks Model in U.S. stocks 2.5 Falling = U.S. stocks stronger 2 1.5 1 Apr-08 Nov-02 May-97 Nov-91 Jun-86 Dec-80 Jun-75 Dec-69 0.5 A Quarterly Asset Allocation Strategy for Foreign-Equity ETFs FT Press 2008 Three distinct areas of the world’s stock markets Through 1989, Japan strong 5000 2002-2007 EM strong 500 MSCI Europe total return 7/2/2008 10/2/2005 1/2/2003 4/2/2000 7/2/1997 1/2/1992 4/2/1989 7/2/1986 10/2/1983 1/2/1981 3/1/1978 6/1/1975 9/1/1972 12/1/1969 50 10/2/1994 1994-2001 EM weak, Japan weak, Europe strong MSCI Emerging Markets total return MSCI Japan total return Source: MSCI Barra (http://www.mscibarra.com/products/indices/international_equity_indices/gimi/stdinde)x/performance.html) Quarterly rotation among broad areas of the foreign stock market • Evaluate MSCI gross total return, US Dollar indexes at the end of each quarter for Japan, Emerging Markets and Europe • Whichever area was strongest in the prior quarter should be held in the current quarter. • Can use ETF data instead: – EWJ for Japan – EEM or VWO for emerging markets – IEV for Europe Europe / Japan / Emerging Mkts 2500 MSCI Europe: 8.4%/year, 54% drawdown MSCI Japan: -1.4%/year, 61% drawdown 2000 MSCI Emerging markets: 12.4%/year, 53% drawdown Quarterly switching model: 11.9%/year, 50% drawdown 1500 1000 500 Jan-10 Nov-08 Oct-07 Sep-06 Aug-05 Jul-04 Jun-03 May-02 Apr-01 Mar-00 Feb-99 Jan-98 Nov-96 Oct-95 Sep-94 Aug-93 Jul-92 Jun-91 May-90 Apr-89 Mar-88 0 Source: MSCI Barra (http://www.mscibarra.com/products/indices/international_equity_indices/gimi/stdinde)x/performance.html) Covered call writing • In return for a fixed payment up front, you agree to forego profits but bear losses that may occur within a limited period of time on a stock or ETF. • Example: I will accept 1.2% to forego all profits and bear all losses in the S&P 500 SPDR (SPY) between now and March 19, 2010 (12 trading days). – The maximum possible gain is the 1.2% of risk capital – Losses can be as large as the amount by which the S&P 500 SPDR (SPY) can fall between now and March 19. – But any loss will be mitigated by the 1.2% I collected. (So if the market falls 5%, my loss on the covered call position will be 3.8%.) • • • • • Not a “conservative” strategy Good strategy for flat or slowly rising markets, like the second year of bull markets. Important to choose the right ETFs or stocks It has been possible historically to achieve a significant risk reduction without loss of profitability Need to watch transaction costs 10 8 6 Buy stock at $90 Sell covered call at $2 4 2 0 -2 -4 -6 -8 Profit / loss on covered call position Profit / loss on ETF alone -10 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 • Buy 100 shares of stock and sell one option on the stock. • Gain is likely to occur, but is limited. • Losses are relatively unlimited, but in a losing month writing a covered call always reduces losses compared to owning the shares alone. Profit / Loss on position at expiration Covered call position Share Price at Expiration Sources: www.cboe.com, Investors FastTrack 1-Jun-2010 1-Jun-2009 1-Jun-2008 1-Jun-2007 1-Jun-2006 1-Jun-2005 BXM dd: -33% S&P dd: -47% 1-Jun-2004 1-Jun-2003 1-Jun-2002 1-Jun-2001 1-Jun-2000 100 1-Jun-1999 200 1-Jun-1998 300 1-Jun-1997 1-Jun-1996 1-Jun-1995 1-Jun-1994 600 1-Jun-1993 700 1-Jun-1992 800 1-Jun-1991 900 1-Jun-1990 1-Jun-1989 1-Jun-1988 Covered call writing: S&P 500 1000 S&P 500 total return (8.9%/year) S&P 500 Buy-Write Index (BXM, 9.4%/year) 500 400 BXM dd: -40% S&P dd: -55% 0 Covered call writing: Dow Jones Industrial Average 240 220 200 180 DJIA total return (4.2%/year) DJIA Buy-Write (BXD, 4.8%/year) 160 140 120 100 DJIA dd: -35% BXD dd: -30% 80 Sources: www.cboe.com, Investors FastTrack DJIA dd: -52% BXD dd: -36% Covered call writing: NDX 1200 NDX total return (10.3%/year) 1000 NDX buy-write (BXN, 7.5%/year) 800 NDX dd: -83% BXN dd: -57% 600 400 200 Sources: www.cboe.com, Investors FastTrack 30-Dec-2009 30-Dec-2008 30-Dec-2007 30-Dec-2006 30-Dec-2005 30-Dec-2004 30-Dec-2002 30-Dec-2001 30-Dec-2000 30-Dec-1999 30-Dec-1998 30-Dec-1997 30-Dec-1996 30-Dec-1995 30-Dec-1994 0 30-Dec-2003 NDX dd: -54% BXN dd: -45% Covered call writing: Russell 2000 190 170 150 Russell 2000 total return (4.4%/year) Russell 2000 Buy-Write (BXR, 3.3%/year) 130 Ru2000 dd: -59% BXR dd: -51% 110 90 70 Ru2000 dd: -37% BXR dd: -29% 50 Sources: www.cboe.com, Investors FastTrack Shorter-term ETF relative strength rankings and trading strategies are reported in my newsletter, Systems and Forecasts (www.systemsandforecasts.com)