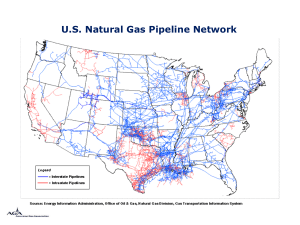

Marcellus Take-away Capacity Projects

advertisement

Florida Energy Conference Shale Revolution Presentation October 29, 2012 Devon Today Proved reserves: 3.0 billion BOE (42% liquids) Q2 2012 production: 679 MBOED Production mix: 22% oil 15% NGLs 63% natural gas Significant midstream business 2012e operating profit: ≈$385 million Enterprise value: $25 billion NYSE: DVN www.devonenergy.com Slide 2 North America Natural Gas Production BCFD 4.3 3.0 2.8 2.6 2.5 2.4 1.7 ExxonMobil Chesapeake EnCana Anadarko ConocoPhillips Note: Production based on second quarter 2012 reported results. NYSE: DVN www.devonenergy.com page 3 BP 1.6 Shell 1.5 Apache Larger than you might think… Enterprise value US$, billions FedEx Allstate Marriott General Motors Best Buy Southwest Airlines $0 $5 $10 $15 $20 Source: Enterprise value as stated on Yahoo! Finance on Jan. 3, 2012. NYSE: DVN www.devonenergy.com page 4 $25 $30 DVN Shale Revolution Shale Evolution: • • • • A Look Back Technology’s Impact US Shale Plays Efficiency NYSE: DVN www.devonenergy.com page 5 Look Back to Early 2000 Natural Gas View • In 2003, Alan Greenspan stated that the US will become a major importer of LNG – Wall Street Journal 2003 Projection of US LNG Imports 9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 0 2002 2003 2004 2005 2006 LNG Import Projection 2007 2010 2011 Actual Source: EIA, Devon NYSE: DVN www.devonenergy.com page 6 2012 Shale Drilling Evolution Traps vs. Shales Fracture stimulation 5,000’ – 15,000’ below the surface Hydrocarbon Trap Migrating Hydrocarbons Shale Organic Rich Source Layer Frack Porous & Permeable Reservoir Layer NYSE: DVN www.devonenergy.com page 7 Impermeable Sealing Layer North American Shale Gas Plays Impact of Shale Gas Plays • Shale play development has been the primary driver in U.S. Lower 48 supply. Sources: EIA, Potential Gas Committee, Ziff Energy NYSE: DVN www.devonenergy.com slide 8 U.S. shale gas production Major U.S. shale plays Barnett Fayetteville Arkoma Woodford Haynesville Marcellus Eagle Ford Ohio Utica 35 30 BCFD 25 20 15 10 5 0 2008 2009 2010 2011 2012 2013 2014 2015 Source: Wood Mackenzie (data through July 2012) NYSE: DVN www.devonenergy.com Slide 9 2016 2017 How Technology Ramped Up Growth Barnett Shale Average Annual Production (BCFD) 5.5 5.0 Total Field Production 2009 > 4.9 BCFD 4.5 4.0 3.5 3.0 Horizontal Technology Light Sand Fracture Technology 2.5 2.0 1.5 Barnett Recognized in 1981 Devon Acquires Mitchell Currently 1.1 1.0 0.5 0.0 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 Devon Other Source: IHS Energy. Gross wellhead production by operator. NYSE: DVN www.devonenergy.com page 10 Devon alone has increased its estimated resource base approaching 5X since 2002. Horizontal Drilling Technology Fracture Stimulation Shale Reservoir Frac Barrier Water Bearing Fm. NYSE: DVN www.devonenergy.com slide 11 Barnett Shale Pad development NYSE: DVN www.devonenergy.com page 12 Rigs Continue to Drill New Wells Faster, Despite Increasing Well Lateral Lengths Wells 3.5 Feet 10,000 New Wells/Rig/Month Total Length 9,000 3.0 8,000 2.5 7,000 2.0 6,000 1.5 5,000 1.0 4,000 0.5 3,000 Marcellus Fayette Barnett 2Q11 Marcellus Fayette Barnett 2Q12 13 Devon – Shale Revolution Infrastructure Revolution • Pipeline Expansion • Storage Increase • Stable Price Environment NYSE: DVN www.devonenergy.com page 14 Major pipeline infrastructure updates 2009 to 2012 Recent capacity additions (Bcfd) Rockies Express 1.80 Midcontinent Express 1.80 Gulf Crossing 1.70 SESH 1.00 Fayetteville/Greenville 1.30 Total 7.60 Committed capacity additions (Bcfd) ETC Tiger (Haynesville) 2.40 Enterprise (Haynesville) 2.10 Regency (Haynesville) 1.10 Gulf South (Haynesville) .50 Centerpoint (Haynesville) .30 Transco (Marcellus) .75 Texas Eastern (Marcellus) .45 Tennessee (Marcellus) .35 Transco (S.E. & Florida Mkts.) .56 FGT (Florida Markets) .82 Trans Canada Bison (Rockies) .48 El Paso Ruby (Rockies) Total NYSE: DVN www.devonenergy.com page 15 1.50 11.31 Marcellus Take-away Capacity Projects Owner Project New In Service 4Q11 Capacity (MMCF/D) Completion Date Status 1,455 Dominion Appalachian Gateway 484 3Q12 In Service Kinder Morgan Tennessee Northeast Supply Diversification 250 4Q12 Under Construction Spectra TEAM 2012 200 4Q12 Under Construction National Fuel Northern Access Expansion 320 4Q12 Under Construction TransCanada Eastern Mainline Expansion 446 4Q12 Under Construction Scheduled in Service 2012 1,700 Millennium 2012 Expansion 150 1Q13 FERC EIS Approval NiSource/UGI PennStar Pipeline 500 4Q13 FERC Application Kinder Morgan Tennessee Northeast Upgrade Project 636 4Q13 FERC Approval Spectra Tetco NJ/NY Expansion Project 800 4Q13 Under Construction Williams Transco Northeast Supply Link 250 4Q13 FERC Application Kinder Morgan Tennessee MPP Project 240 4Q13 In Development Spectra Tetco Uniontown to Gas City Expansion 300 4Q13 Open Season Scheduled in Service 2013 2,876 Williams Transco Northeast Connector 100 2Q14 Signed Agreements Williams Atlantic Access Pipeline 1800 4Q14 50% Capacity Signed Spectra TEAM 2014 1400 4Q14 43% Capacity Signed Spectra Ohio Pipeline Energy Network (OPEN) 1000 4Q14 In Development Scheduled in Service 2014 TOTAL UNDER DEVELOPMENT 4,300 8,876 Does not include gathering or shorter intra-regional projects. 16 Natural Gas Storage 1999 to 2015 • • Storage Capacity has increased by roughly .5 TCF over the last 10 years Storage Capacity is expected to increase by another .5 TCF by 2015 Source: Wood Mackenzie NYSE: DVN www.devonenergy.com page 17 Gas price stability As supply grows, price remains low, stable Lower 48 gas supply has grown by 20 Bcfd since 2000, up 50% • Driven by shale and infrastructure development post 2005 • Result: lower, more stable pricing U.S. Lower 48 Gas Production (BCFD) Henry Hub FOM Index Price ($/MMBtu) U.S. Lower 48 Gas Supply (BCFD) 65 60 16 Hurricanes Katrina & Rita Strong global economy Price run-up with crude oil 14 12 Cold weather 55 10 50 8 45 6 40 4 35 2 30 0 NYSE: DVN www.devonenergy.com page 18 Henry Hub FOM Index ($/MMBtu) 70 What’s Next Stable Prices have Revitalized US Industrial Sector • Steel Industry • “Cheap Natural Gas Gives Hope to the Rust Belt” – Wall Street Journal • 10 New Plants Planned with 2 additional expansions • Fertilizer Plants • 9 Plants in the making - (1 New, 4 Restarts, 4 Expansions) • Ethylene Crackers and Petrochemical Expansion • 31 Plants coming on line (17 New, 5 Restarts, 9 Expansions) • Gas to Liquids (GTL) • 4 GTL Plants in the planning process NYSE: DVN www.devonenergy.com page 19 America’s “New” Natural Gas: Choice, Reliability, Competition, Price Stability • 100+ years of natural gas supply – and growing with technology • New shale gas resources: – Efficiency Gains – Pad Drilling – Longer Laterals – Rig Efficiencies – Long-term supply stability – Wells produce for 40 - 50 years or more • Expanding technology to additional resources – What’s Next?? • New resources onshore are easier and less expensive to develop - Efficiencies • Pipeline and storage infrastructure to deliver gas on a reliable basis Bottom line: Greater energy and economic security; more stable, predictable prices NYSE: DVN www.devonenergy.com page 20