Modifications to the Foreign Trade General Rules

advertisement

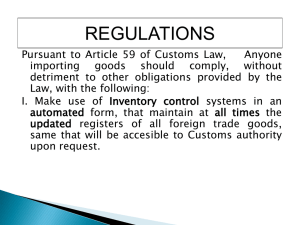

WMTA Monthly Meeting February 2011 Virtual transactions have been a fundamental practice for maquiladoras and IMMEX Companies. These transactions allow IMMEX companies to transfer temporary imported goods to other IMMEX companies. The companies that receive the goods may submit them to an industrial or services process. Virtual transactions are also important in order to have their goods considered as exported within the legally established periods of time. (VAT & Simplification Process). The legal base of virtual transactions relies on Article 112 of the Mexican Customs Law and on Rule 4.3.25 of the General Rules of Customs and Foreign Trade. Last December 24, 2010, the General Rules for Customs and Foreign Trade where modified in order to add Rule 4.3.25, modifying the procedure for virtual transactions established on Rule 5.2.5., eliminating Rule 5.2.3. and 5.2.8. IMMEX Companies shall submit their temporary import customs declarations to the company that will receive the goods. The company that receives the goods shall present its respective return customs declaration within the next day, at the most. Virtual Transaction involving abroad companies. Temporary imported goods by an IMMEX Company, when the delivery of the goods takes place in Mexico with another IMMEX Company. Sale Return, Export USA Mexico Temporary Import Virtual Transaction IMMEX IMMEX Delivery of Goods § I. b) Is modified in order to mention that for virtual transactions of goods transported in one vehicle, the maximum weight shall be 25 Tons. In the event of double containers, the maximum weight shall be 50 tons. Companies who transfer goods weighting more than 25 or 50 tons, may apply a weekly or monthly consolidated virtual customs declaration regarding the goods transferred. In the event of consolidated virtual transactions, these operations shall be closed on a weekly basis, or within the first 10 days of each month. IMMEX Companies shall return the goods received or make a definite import within the next six months after the date the virtual transaction took place. (Not applicable to Certified Companies, 36 months) This was a huge change, as this six month period was reduced from the original 18 month period in order to return the goods involved in these virtual transactions. The six month return period will not be applicable in the following events: a) Goods received from Certified Companies (36 months). b) Goods received from Mexican suppliers (18 months). c) Goods mentioned on Article 108, § II and III of the Mexican Customs Law. § I. c) establishes the limitation for companies to transfer goods in the same condition as they were imported. This was a important change, as the previous rules didn’t mention this limitation. This limitation is not applicable to Certified Companies, nor to Services IMMEX Companies that transfer goods. In order for Virtual Transactions to be considered as valid, we must take into consideration the following: Virtual Transactions shall be reflected in the companies' Inventory Control System mentioned in the Appendix 24 of Exhibit 22 of the General Rules for Customs and Foreign Trade. 1. 2. 3. 4. 5. 6. Customs Authority, in order to verify that virtual transactions are being made in accordance to the legal frame may request the following documents: The transportation of the goods (Bill of Lading / “Carta Porte”). The payment of transportation (Invoice, Diesel Expenses or Contract). The physical exit of the goods of the Company that transfers them (Load Sheet). The physical entry of the goods to the Company that receives them (Signed and Stamped Load Sheet). Invoice or “Nota de Remision”. The transformation and reparation processes before its transfer. In the event the Authority requests these documents and the companies fail to prove such information, virtual transactions may be considered as invalid. It is important to previously validate the consolidated customs declarations before the physical transfer of the goods takes place. The “Nota de Remision” or Invoice shall include the IMMEX number of the companies involved in virtual transactions and the customs declaration number. NAME OF THE COMPANY THAT ISSUES THE "NOTA DE REMISION" Address TIJUANA, B.C. TEL. 01 (664) TAX ID NOTA DE REMISION No. IMMEX Number: Name of the Company that will receive the goods TIJUANA, B.C. TAX ID DAY MONTH YEAR ADDRESS IMMEX Number: MEASURE AMOUNT UNIT UNITARIO MODEL DESCRIPTION Number of Customs Declaration of the Consolidated Operation: PRICE Customs Entry Port: BULKS : Indicate the rules that will govern the Transaction Art. 29-A CFF TOTAL IMMEX Companies with a Service program shall indicate the “MS” Identification Code as a General Rule, with the following Complementary Codes: 1. Distribution or storage 2. Classification, inspection or verification 3. Procedures that do not change the goods characteristics. 4. Preparation of kits with promotional purposes 5. Repair 6. Laundry 7. Embroidering and printing of clothes. 8. Shielding, modifying or adapting vehicles. 9. Waste Recycling. 10. Product design & engineering. 11. Software design. 12. Services regarding information technology. 13. Sub contracting services regarding information technology. 14. Other services Different Customs Declaration per comlementary code • Ricardo Rebeil • Brokerage & Logistic Solutions, Inc. • rr@bls-usa.com • (619) 671-0276