Local Council Tax Scheme consultation presentation

advertisement

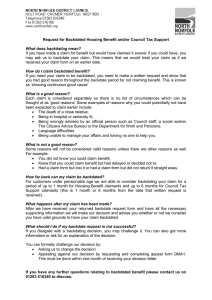

Council Tax Support Scheme 2015/16 Councillor Darren Rodwell Leader of the Council Jonathan Bunt Chief Finance Officer Siân Peters Director Revenues & Benefits Elevate East London 11th December 2014 Introduction Changes to Council Tax Support: • History: Abolition of Council Tax Benefit and localisation • Council Tax Support replaced Council Tax Benefit in April 2013 • Year 1 of localisation: drop in subsidy, drop in support • Year 2: zero subsidy but higher retention of business rates • Year 3: £54m savings to be made by this Council: • The Council must collect more revenue to pay for services • This is an opportunity to explain the changes and get your views on our revised scheme Funding, Demographic & Legislative Pressures £m Gap brought forward Funding cuts Growing demand 1 38.1 3 New responsibilities & legislation 5.2 Pay & inflation 7.1 Other 2.5 Council Tax Business Rate pooling Total (2.4) (1) 53.5 History of Savings 2010-2014 The options to save £54m have to be seen in the context of the savings already made: Year £m 2010/11 22.4 2011/12 28.2 2012/13 19.0 2013/14 16.6 2014/15 7.7 Total 93.9 Inevitably means harder choices over the next three years. Internal & Efficiency Saving Proposals The council has endeavoured to protect the public from service cuts as much as possible. Several efficiency savings and internal changes have been proposed to help bridge the gap. Examples Include: Description of saving £m Review of office accommodation 0.8 Freeze staff pay increments & reduce redundancy payments 0.7 Restructuring councils borrowing & investments 7.4 Alternative management model – leisure services 1 IT efficiencies 1.5 Lean back office functions e.g. Finance, Human Resources & management structures 2.0 Income generation & alternative funding sources 6.8 Total 20.2 Other Saving Proposals Due to the size of the funding cuts and pressures the council faces, efficiency savings alone have not been enough to bridge the gap. Harder choices are having to be made. Examples of these include: Description of saving £m Council tax support scheme 0.7 Ceasing green garden waste collections 0.2 Stop supported living arrangements 0.8 Redesign of street cleansing services 0.3 Children’s social care savings 2.5 Reduction in support to quality childcare and early years provision 0.4 Reduce children in need support 0.5 Reduce primary mental health workers 0.3 Changes to youth services provision 0.6 Reduction in children centre service provision 1.2 Total 7.5 Legal Requirements Government requirements • Pensioners are protected • Councils must try to ensure people are ‘better off’ in work • Residents must have the opportunity to comment on the scheme – online survey, public meetings etc. Council Tax Support – The Current Scheme What is it? – it is a means-tested reduction to a household’s Council Tax bill Scheme: Since April 2013 same principles as Council Tax Benefit but with an 85% maximum reduction for working age residents which means everyone, except pensioners, must pay some of their bill. Simple: easy to administer, collect and understand Fair: support is across all customers (except pensioner who must be protected) April 2015 - Changes Proposed… Maximum Reduction decreased to 75% • What this means • Working age residents pay at least 25% towards their Council Tax bill • The average bill will increase from £151.87 to £242.99 per year (£20.45 per month over 12 months based on a Band D property) • Is the only proposed change that will affect all customers (except pensioners) • Why reduce the maximum support? • It is fairer to reduce support evenly across all customers Impact – case study 1 Ms Green – Band C property • Ms Green is a 27 year old single parent with two children living with her aged under 5 • The amount the rules say she needs to live on (her applicable amount) is £218.38 per week • Her income is £176.98. She has £0 excess income. • She currently receives full support (85%) so pays £2.53 per week Council Tax (£131.54 per year) • Under the proposed new scheme she will only receive a reduction of 75% so will have to pay £4.22 per week (£219.23 per year) Changes Proposed continued… Abolish Second Adult Rebate • Known as the “Alternative Maximum Reduction” in the scheme • What is it? • It is a reduction awarded based on the income of a second adult who is not a partner and lives in the property; and • Where the customer wouldn’t otherwise receive a reduction to their bill because they have sufficient income (means) to pay it. • Reductions are set at 25%, 15% and 7.5% depending on how much income the second adult has • Why remove it from the scheme? • To avoid awarding reductions to people whom can afford their bill Impact – case study 2 Mr Brown – Band C property • Mr Brown is 36 years old. He has a net weekly income of £635.12 • The amount the rules say he needs to live on (his applicable amount) is £72.40 per week • After ‘disregards’ he has an excess income of £540.12 per week • His income is too high to qualify for a reduction but his 26 year old son Kevin lives with him and receives Jobseeker’s Allowance (Income Based) • He is entitled to a 25% alternative reduction and currently pays Council Tax of £16.86 per week (£876.94 per year) • If Second Adult Rebate is removed he will no longer receive any reduction so will have to pay £22.49 per week (£1,169.25 per year) Changes Proposed continued… Reduce the Capital Limit to £6,000 • Currently, the limit is £16,000 • What is it? • It is the maximum capital someone may have • Currently, if capital is held over £16,000 there is no entitlement to receive Council Tax Support • Why reduce the limit? • To avoid awarding reductions to people that can afford their bill • People with capital over £6,000 are expected to use this to pay their bill Impact – case study 3 Mr and Mrs Scarlett – Band C property • Mr and Mrs Scarlett are both 29 years old. They have a combined net weekly income of £216.12 and £7,223 in a savings account. • The amount the rules say they need to live on (their applicable amount) is £113.70 per week • After ‘disregards’ they have an excess income of £74.82 per week • They are entitled to a reduction and currently pay £14.97 per week (£778.44 per year) Council Tax • If the Capital Limit is reduced they will no longer receive any reduction because they will become exempt from the scheme. They will have to pay £22.49 per week (£1,169.25 per year) Changes Proposed… Final Remove Backdate Discretion • Currently, someone can request a 3 month backdated reduction • What is it? • It is a discretion that a customer can request that if awarded, can reduce their bill further by requesting their reduction be applied from an earlier date allowed under the normal scheme rules • You must show the council that you had good cause for not applying for Council Tax Support during the length of the backdate period • Why remove this discretion? • Most people ask for backdate without showing good cause • A fairer and easier to administer backdate discretion will be made available via the Discretionary Council Tax Reduction scheme Impact – case study 4 Mrs Orange – Band C property • Mrs Orange receives Income Support and applies for Council Tax Support on 17 July 2014. • She is entitled from 21 July 2014 and is awarded a weekly reduction of £16.86 per week (£607.11 reduced from her annual bill) • She will therefore pay £5.19 per week (£269.83 for the year) Council Tax • She asks the Council for her reduction to be applied from 01 June 2014 because she was in hospital from this date up until 16 July 2014. She has evidence and also was receiving Income Support for this period • Her reduction is backdated to 02 June 2014 which entitles her to an additional £118.05 reduction from her annual bill. • Her new payments are £2.92 per week (£151.77 per year) Council Tax • If the Backdate Discretion is removed, Mrs Orange would have continued to pay £5.19 per week (£269.83 for the year) Funding • There is no funding given to run this scheme but the council does get to keep more of the business rates it collects. • The proposed changes in support received from April 2015 will be dependant on individual circumstances and Council Tax Property bands • The Council have a discretionary scheme that will be published later in 2015 to help those that are in exceptional financial need. Summary • Proposed Changes o 85% to 75% passes reduced support to all o assumes those with sufficient capital to pay and therefore would not receive support anymore o Removes the backdate provision ; circumstances of exceptional hardship will be supported by a discretionary reduction scheme for council tax o Removal of the Second Adult Rebate Scheme • Pensioners remain protected • Remain on the current scheme • Your opportunity to comment on the changes Conclusion – Councillor Darren Rodwell • Difficult choices but no option but to make these proposals • Your views on the proposed revised scheme • Fill out a survey now or on line until 20th December visit: www.lbbd.gov.uk/ctss • Final decision taking into consideration all consultation will be made in January 2015 • If accepted the new changes implementation from April 2015 • Organisations like DABD, CAB can help as well as the Council Questions?