Basel III American style - slide show presentation

advertisement

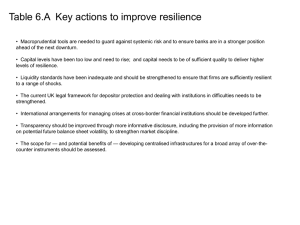

Capital American Style: The Federal Banking Agencies’ Regulatory Capital Proposals June 28, 2012 Charles M. Horn Dwight C. Smith Morrison & Foerster LLP Adriaan Van der Knaap StormHarbour Securities Ltd. Introduction On June 12, 2012, the Federal banking agencies (the OCC, Federal Reserve Board and FDIC) (the “Agencies”) formally proposed three sets of significant changes to the U.S. regulatory capital framework: The Basel III Proposal, which applies the Basel III capital framework to almost all U.S. banking organizations The Standardized Approach Proposal, which applies certain elements of the Basel II standardized approach for credit risk weightings to almost all U.S. banking organizations The Advanced Approaches Proposal, which applies changes made to Basel II and Basel III in the past few years to large U.S. banking organizations subject to the advanced Basel II capital framework. Deadline for comments on all three proposals is Sept. 7, 2012. We understand there have been some informal discussions regarding extension of the deadline. 2 Today’s Presentation The Agencies’ proposals Basel III Proposal – the components of capital Standardized Approach Proposal – risk-weightings of on-balance and off-balance sheets assets, commitments and contingencies Advanced Approaches Proposal – regulatory capital proposals affecting large, internationally active banking organizations Implementation and phase-in requirements Impact of the proposals Nature and composition of capital (“numerator” impact) Composition and costs of on- and off-balance sheet activities (“denominator” impact) Impact on banking organization behaviors 3 Basel III Proposal Applicability All U.S. banks that are subject to minimum capital requirements, including Federal and state savings banks Bank and savings and loan holding companies other than “small bank holding companies” (generally bank holding companies with consolidated assets of less than $500 million) Top-tier domestic bank and savings and loan holding companies of foreign banking organizations Does not apply to foreign banking organizations, but does apply (with a few exceptions) to U.S. bank subsidiaries, and top-tier U.S. bank holding company subsidiaries, of foreign banking organizations 4 Basel III Proposal Components of Capital: Tier 1 Capital -- common equity Tier 1 capital and additional Tier 1 capital Total Tier 1 capital, plus Tier 2 capital, would constitute total riskbased capital Proposed criteria for common equity and additional tier 1 capital instruments, and Tier 2 capital instruments, are broadly consistent with the Basel III criteria. 5 Basel III Proposal Common Equity Tier 1 Capital elements: Common stock and related surplus net of treasury stock satisfying 13 criteria Retained earnings Accumulated other comprehensive income (“AOCI”) Qualifying common equity Tier 1 minority interest Common equity Tier 1 criteria are generally designed to assure that the capital is perpetual and is unconditionally available to absorb first losses on a going-concern basis, especially in times of financial stress. 6 Basel III Proposal Additional Tier 1 Capital elements: Qualifying capital instruments (and related surplus) that satisfy 13 separate criteria (14 for advanced approaches banking organizations) Tier 1 minority interests that are not included in a banking organization’s common equity Tier 1 capital Qualifying TARP and Small Business Jobs Act preferred securities that previously were included in Tier 1 capital The 13/14 criteria generally are designed to assure that the capital instrument can absorb going-concern losses and does not possess credit sensitive or other terms that would impair its availability in times of financial stress. 7 Basel III Proposal Tier 2 Capital elements: Qualifying instruments that satisfy 10 separate criteria (11 for advanced approaches banking organizations) Qualifying total capital minority interest not included in Tier 1 capital Allowance for loan and lease losses (“ALLL”) up to 1.25% of standardized total risk-weighted assets excluding ALLL (Advanced approaches bank may include excess of eligible credit reserves over total expected credit losses not to exceed 0.6 percent of its total credit RWA.) Qualifying TARP and Small Business Jobs Act preferred securities that previously were included in Tier 2 capital Tier 2 capital elements are designed to assure adequate subordination and stability of availability. 8 Basel III Proposal Significant Exclusions from Tier 1 Capital Non-cumulative perpetual preferred stock, which presently qualifies as simple Tier 1 capital, would not qualify as common equity Tier 1 capital, but would qualify as additional Tier 1 capital. Cumulative preferred stock would no longer qualify as Tier 1 capital of any kind. Certain hybrid capital instruments, including trust preferred securities, no longer will qualify as Tier 1 capital of any kind. Some of these results are mandated more by the DoddFrank Act (section 171, or the “Collins Amendment”) than by Basel III itself. 9 Basel III Proposal Regulatory Capital Adjustments – Common Equity Tier 1: Accumulated net gains/losses on specified cash flow hedges included in AOCI Unrealized gains and losses on AFS securities Unrealized gains on AFS securities includable in Tier 2 would be eliminated. Unrealized gains and losses resulting from of changes in banking organization creditworthiness 10 Basel III Proposal Deductions from Tier 1 common equity capital: Goodwill, net of associated deferred tax liabilities (“DTLs”) Intangible assets other than mortgage servicing assets (“MSAs”), net of associated DTLs Deferred tax assets (“DTAs”) Securitization gain-on-sale Defined benefit plan assets (excluding those of depository institutions (“DIs”)) Advanced approaches banks: expected credit losses exceeding eligible credit reserves Savings association impermissible activities Items subject to 10%/15% common equity Tier 1 capital thresholds (certain DTAs, MSAs, significant unconsolidated FI common stock investments) 11 Basel III Proposal Deductions from Tier1/Tier2 capital: Direct and indirect investments in own capital instruments Reciprocal cross-holdings in financial institution capital instruments Direct, indirect and synthetic investments in unconsolidated financial institutions. Three basic types: Significant Tier 1 common stock investments Significant non-common-stock Tier 1 investments Non-significant investments (aggregate 10% ceiling) The “corresponding deduction” approach Volcker Rule covered fund investments (from Tier 1)(when Volcker Rule regulatory capital requirements are final) Insurance underwriting subsidiaries 12 Basel III Proposal Minority Interests: Limits on type and amount of qualifying minority interests that can be included in Tier 1 capital Minority interests would be classified as a common equity Tier 1, additional Tier 1, or total capital minority interest depending on the underlying capital instrument and on the type of subsidiary issuing such instrument. Qualifying common equity Tier 1 minority interests are limited to a depository institution (“DI”) or foreign bank that is a consolidated subsidiary of a banking organization. Limits on the amount of includable minority interest would be based on a computation generally based on the amount and distribution of capital of the consolidated subsidiary 13 Basel III Proposal Minimum Capital Requirements (fully phased-in): Common equity Tier 1 capital ratio to standardized total riskweighted assets (“TRWA”) of 4.5 percent Tier 1 capital ratio to standardized TRWA of 6 percent Total capital ratio to standardized TRWA of 8 percent Tier 1 leverage ratio to average consolidated assets of 4 percent Advanced approach banking organizations must use lower of standardized TRWA or advanced approaches TRWA For advanced approaches banking organizations, a supplemental leverage ratio of Tier 1 capital to total leverage exposure of 3 percent Common equity Tier 1 capital ratio is a new minimum requirement. 14 Basel III Proposal Leverage Requirement: Ratio of Tier 1 capital (minus required deductions) to average onbalance sheet assets for all U.S. banking organizations Supplementary Leverage Requirement: Applies only to advanced approaches banking organizations Ratio of Tier 1 capital (minus required deductions) to average onbalance sheet assets, plus certain off-balance sheet assets and exposures: Future exposure amounts arising under certain derivatives contracts 10% of notional amount of unconditionally cancelable commitments Notional amount of most other off-balance sheet exposures (excluding securities lending and borrowing, reverse repurchase agreement transactions, and unconditionally cancelable commitments). 15 Basel III Proposal Capital Conservation Buffer: A new phased-in capital conservation buffer for all banking organizations equal to a ratio to TRWA of 2.5% common equity Tier 1 capital Unrestricted payouts of capital distributions and discretionary bonus payments to executives and their functional equivalents would require full satisfaction of capital conservation buffer requirement. Maximum amount of restricted payouts would be the banking organization’s eligible retained income times a specified payout ratio. These ratios would be established as a function of the amount of the banking organization’s capital conversation buffer capital. 16 Basel III Proposal Countercyclical Capital Buffer: A macro-economic countercyclical capital buffer of up to 2.5% of common equity Tier 1 capital to TRWA applicable only to advanced approaches banking organizations. Countercyclical capital buffer, applied upon a joint determination by federal banking agencies, would augment the capital conservation buffer. Unrestricted payouts of capital and discretionary bonuses would require full satisfaction of countercyclical capital buffer as well as capital conservation buffer. 17 Basel III Proposal Supervisory Assessment of Capital Adequacy Banking organizations must maintain capital “commensurate with the level and nature of all risks” to which the banking organization is exposed General authority for regulatory approval, on a joint consultation basis, of other Tier 1 or Tier 2 instruments on a temporary or permanent basis 18 Basel III Proposal Changes to Prompt Corrective Action (“PCA”) Rules: PCA regulations changed to assure consistency with the new regulatory capital requirements PCA capital categories would include a separate requirement for minimum common equity Tier 1 capital for top 4 PCA categories (6.5%/4.5%/<4.5%/<3%). “Well-capitalized” DIs would have to have at least 8% Tier 1 capital (up from current 6%), and “adequately capitalized” DIs 6% Tier 1 capital (up from current 4%). “Adequately capitalized” PCA category for advanced approaches banks would include a minimum 3% supplementary leverage ratio requirement. Revisions to the definition of “tangible equity” for critically undercapitalized DIs, and HOLA/savings institutions 19 Basel III Proposal Effective Dates/Transitional Periods: Minimum Tier 1 capital ratios -- 2013-2015 Minimum total capital: no change and therefore no phase-in Regulatory capital adjustments and deductions -- 2013 -2018; goodwill deduction is fully effective in 2013 Non-qualifying capital instruments BHCs of $15 BB+ in assets -- 2013-2016 BHCs under $15BB and all DIs -- 2013-2022 Capital conservation and countercyclical capital buffers, and related payout ratios -- 2016-2019 Supplemental leverage ratio for advanced approaches banks – 2018; calculation and reporting required in 2015 PCA changes – 2015 (2018 for supplemental leverage ratio) 20 Numerator Comparisons The US Basel III Proposal is consistent with its BIS and European counterparts (EU CRD IV). “Consistent,” however, does not mean identical US proposal applies to all banks and their holding companies except “small bank holding companies.” Common Equity Tier 1 --- US Treatment US: GAAP treatment of qualifying instruments must be non-liability Common equity instruments do not expressly have to be “shares” Unrealized AFS losses and gains flow through to common equity Tier 1 capital Cash dividends paid only out of net income and retained earnings 21 Numerator Comparisons Additional Equity Tier 1 --- US Treatment GAAP treatment of qualifying instruments must be non-liability No specific going-concern loss requirements specified Cash dividends paid only out of net income and retained earnings Permanent grandfathering of US government capital investments such as TARP and Small Business Jobs Act securities Subordination disclosure requirements for advanced approaches banks Leverage ratio US banks are already subject to leverage ratio Supplemental leverage ratio applies to advanced approaches banks. 22 Numerator Comparisons Countercyclical capital buffer – US Treatment Applies only to advanced approaches banking organizations 23 Standardized Approach Proposal Introduction to the standardized approach Risk weights Credit risk mitigants Impact of the changes 24 Standardized Approach Proposal Applicability. Generally, the same banks that would be subject to the Basel III Proposal. Proposed Effective Date. Jan. 1, 2015. Banks may opt in earlier. 25 Standardized Approach Proposal Themes of the Standardized Approach Improved sensitivity to credit risk Elimination of reliance on credit ratings Behavior modification 26 Standardized Approach Proposal Risk weights – 9 broad asset classes Residential mortgages Commercial lending – “high volatility” CRE loans Off-balance sheet exposures OTC Derivatives Cleared transactions Unsettled transactions Securitization exposures Equity exposures Sovereign and foreign bank exposures 27 Standardized Approach Proposal 1. Residential first mortgages – private Category 1 (traditional) vs. Category 2 (non-traditional) Duration Payment schedule Documentation Loan-to-value ratio Eight sets of risk weights—generally higher than current rules Public policy 28 Standardized Approach Proposal Private residential mortgages riskweight chart LTV Traditional Non-traditional <60% 35% 75% >60, <80 50 100 >80, <90 75 150 >90 100 200 29 Standardized Approach Proposal Residential mortgages – other issues Restructured or modified loans Junior liens Mortgage-servicing assets 30 Standardized Approach Proposal 2. Commercial lending Current 100% default weight still applies High volatility CRE – 150% Behavior modification Enhanced equity contribution by developer Pre-sold lots Ability to cancel Past-due loans 31 Standardized Approach Proposal 3. Off-balance sheet exposures 0% -- only unconditionally cancelable commitments [10% -- eliminated] 20% -- short-term commitments (and trade-related contingent claims) 50% -- no change (long-term commitments and transaction-related contingent claims) 100% -- guarantees, repos, securities borrowing and lending transactions, financial stability letters of credit, forward agreements 32 Standardized Approach Proposal 4. OTC Derivatives Capital impact depends on measurement of exposure. Single contracts Current credit exposure plus probability of future exposure Multiple contracts subject to “qualifying master netting agreement” “Qualifying” Exposure Risk weight is a function of the counterparty’s credit risk. 50% cap eliminated 33 Standardized Approach Proposal 5. Cleared transactions Exposure Bank as clearing member Bank as clearing member client Risk weights – “qualifying central clearing party” QCCP – must be designated FMU Clearing member: 2% versus 100% Clearing member client: 2-4% versus 100% Default fund contributions 34 Standardized Approach Proposal 6. Unsettled transactions Risk of delayed settlement or delivery Exemptions DvP and PvP transactions Non-DvP and PvP transactions 35 Standardized Approach Proposal 7. Securitization exposures Operational requirements Due diligence Calculation of exposures Risk-weighting alternatives SSFA Approach Gross-Up Approach Other Treatment of gain-on-sale 36 Standardized Approach Proposal 8. Equity exposures to unconsolidated entities Current rule – 100% Exposure – adjusted carrying value Simple Risk Weight Approach – for exposures to companies (but not investment funds) Look-through approaches for investment fund exposures Full look-through Simple modified look-through Alternative modified look-through 37 Standardized Approach Proposal 9. Sovereign and foreign bank exposures Current rule – OECD membership Proposal – OECD country risk classification (“CRC”) Risk weights range from 0% to 100% for sovereigns 20% to 100% for PSEs and foreign banks Sovereign crises -- 150% Default Reduced CRC 38 Standardized Approach Proposal Credit risk mitigants Government guarantees of residential mortgages Guarantees and credit derivatives Issuers Terms Collateral Mitigants in securitizations 39 Standardized Approach Proposal Disclosures Banks with more than $50 billion in consolidated assets but not subject to advanced approaches Disclosure policy Quarterly disclosures Templates 40 Standardized Approach Proposal Impact: all asset classes affected Private residential mortgage lending Commercial lending Off-balance sheet transactions OTC derivatives Cleared transactions Unsettled transactions Securitizations Equity exposures Sovereign exposures 41 Denominator Comparisons Standardized Approach Proposal would apply to all banks and their holding companies other than “small bank holding companies.” US proposal does not allow reliance on credit rating references, as required by Dodd-Frank Act section 939A. The new US standard is “investment grade,” which is a more qualitative approach. To be investment grade, a counterparty or reference entity must have: “adequate capacity” to meet financial commitments for the projected life of the asset or exposure “adequate capacity” means risk of default is low and the full and timely repayment of principal and interest is expected 42 Denominator Comparisons Denominator impact of section 939A requirement is broad. Basel II ratings-based approach and internal assessment approaches for securitization exposures are removed Sovereign, residential mortgage and debt exposures affected Impact on eligible guarantees and guarantors, credit derivatives and credit risk mitigants Affects potential future exposure of OTC derivatives for purposes of on-balance sheet credit conversion 43 Denominator Comparisons Other US denominator variances: Risk-weightings of residential mortgage exposures is significantly more granular than under Basel II. Treatment of high-volatility commercial real estate exposures Exposures to securities firms are treated as corporate exposures, not DI exposures Basel II, however, does anticipate national application of its risk-weighting requirements, which affords the US – like any other participating jurisdiction – some latitude in Basel II’s implementation (particularly where it is being applied to non-Basel II banks!). 44 Advanced Approaches Proposal Applicability and Coverage: Applies to banking organizations that are subject to the “advanced approaches” rule under Basel II, including qualifying Federal and state savings associations and their holding companies Addresses counterparty credit risk, removal of credit rating references, securitization exposures, changes in treatment of certain exposures previously subject to deduction, and conforming technical changes Proposes to expand those banking organizations that are subject to the market risk capital rule to include savings institutions and their holding companies Proposed Effective Date: None specified 45 Advanced Approaches Proposal Counterparty Credit Risk. Changes proposed include: Revisions to the recognition of eligible financial collateral Lengthening the assumed holding periods and the calculation of certain collateralized OTC exposures under the collateral haircut and simple Value-at-Risk (VaR) approaches Increasing capital requirements associated with the internal models methodology Better identification and management of wrong-way risk associated with certain counterparty exposures 46 Advanced Approaches Proposal Counterparty Credit Risk Changes (cont.): Additional capital requirement for credit value adjustments relating to OTC derivatives exposures Changing the capital requirements for qualifying and other central counterparty (“CCP”) exposures, including capital calculations for CCP default fund contributions Requiring application of a continuous 12-month stress period in calculating market price and foreign volatility exposures under the collateral haircut method, based on internal estimates 47 Advanced Approaches Proposal Removal of Credit Rating References: Consistent with section 939A of the Dodd-Frank Act, the Advanced Approaches Proposal would remove references to credit ratings that currently exist in the advanced approaches capital rules and replace these references with alternative standards of creditworthiness. Affects, among other things, treatment of guarantors, OTC derivatives exposures, money market fund exposures, operational risk mitigants and securitization exposures This action is also consistent with removal of credit rating references in the Standardized Approach Proposal. 48 Advanced Approaches Proposal Changes to Securitization Exposures: Proposed new definition of resecuritization exposures Proposed broadening of the definition of securitization exposures, while excluding certain traditional investment firms from definition Resecuritization definition would capture exposures to securitizations that are comprised of asset-backed securities (e.g., CDOs and some ABCP conduits) and which are now subject to higher risk-weightings under the 2009 changes to Basel II. Removal of ratings-based and internal assessment approaches for securitization exposures; new hierarchy for exposure treatment General use of supervisory formula approach (“SFA”) or its simplified version (“SSFA”) in calculating capital requirements for securitization exposures, as well as guarantees and credit derivatives referencing such exposures 49 Advanced Approaches Proposal Revised Capital Treatment of Certain Exposures Exposures affected: certain securitization exposures (CEIOs, high-risk exposures, low-rated exposures); eligible credit reserves shortfall; certain failed capital markets transactions New treatment – assigned a general 1,250 percent risk-weighting instead of deduction from capital Market Risk Capital Rule: Federal and state savings banks and their holding companies that meet the market risk capital rule threshold criteria would become subject to the rule. 50 Impact of These Developments In general, US financial institutions are taking a “waitand-see” attitude to the various Dodd-Frank Act and regulatory capital proposals, with some exceptions (e.g., the Volcker Rule). Most rules are not finalized and there is considerable time left to work on implementation before compliance deadlines. Further, a majority of US banks are very liquid and in excess capital positions (even factoring in the possible impact of the Basel III and Standardized Approach Proposals), which may reduce their collective sense of urgency. 51 Impact of These Developments The overall impact on the banking sector varies depending on the size of the banking organizations. The larger regional banks currently have excess liquidity and capital, and, as there is no pressure on capital, are selectively expanding their asset bases (although the current regulatory uncertainty has depressed M&A activity). The smaller banks are under the most pressure, as the uncertainty and the costs of complying with the new rules are weighing heavily on their cost ratios. The largest banks are already selling certain businesses (private equity, proprietary trading) or are reducing and re-balancing their assets (Citi/BoA) or aggressively expanding traditional lending (Wells, JPM, Citi) 52 Impact of These Developments Most banks in the US have strong capital ratios, and regulators have generally put restrictions on repatriation of common equity capital. Thus, the Basel III Proposal has not resulted in much activity as of yet to optimize capital structures. Going forward, the only hybrid capital element that will qualify as Tier I capital will be perpetual noncumulative preferred stock; some recent issuances, but limited compared to expected capacity Banks already are selectively redeeming or repurchasing trust preferred securities. As European banks generally have lower capital ratios, and have not raised as much equity since the 2008 financial crisis, there is more focus on capital raisings in Europe. 53 Impact of These Developments The changes in risk weightings and deductions from capital under the Standardized Approach Proposal will have an impact on the credit markets, although it is too early to predict the magnitude of this impact. Nonbank finance companies are actively seeking capital to enter certain loan markets. Mortgages: some mortgage products will become more expensive for banks to hold. Securitizations: impact will be a function of capital costs of directly owning assets versus an exposure to a securitized portfolio. MSAs and other deductions from capital will influence balance sheet management behaviors. Commercial real estate loans may become more expensive to hold. 54 Impact of These Developments Conclusion: there is still a lot of uncertainty, but US institutions are liquid and well capitalized, and therefore can afford to be patient and focus on organic growth of their balance sheets. In Europe, the situation is different due to liquidity issues and lower capital levels. Therefore, more immediate action in Europe is required to maintain minimum capital levels and de-leverage. 55 Concluding Remarks Questions and Answers 56