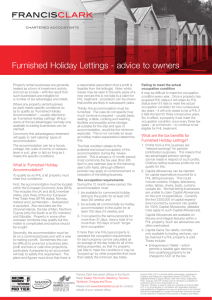

FURNISHED HOLIDAY LETS An Update

advertisement

FURNISHED HOLIDAY LETS An Update - Know where you stand! From 6 April 2012 many of the favourable tax rules applicable to Furnished Holiday Lettings (FHLs) in the UK and EEA were withdrawn by the UK Government. We take a look here at the changes in rules and outline some on-going advantages that FHLs enjoy. Firstly, how do you qualify as a FHL as of 6 April 2012. From 6 April 2012, to qualify as an FHL, your property must meet the following qualifying conditions during a relevant period (usually the tax year): • • • • • • There must be a commercial letting – i.e. a view to realise profits; Your FHL must be available for letting to the public each year for 210 days or 30 weeks (increased from 140 days or 20 weeks previously) – this is know as the availability threshold; Your FHL must actually be let to the public each year for 105 days or 15 weeks (increased from 70 days or 10 weeks) – this is known as the occupancy threshold; Your FHL must be in the EEA (including the UK); Your FHL must not be let for periods of longer-term occupation (i.e. to the same person for more than 31 consecutive days) for more than a total of 155 days during the year; Where the qualifying conditions are not met during the relevant period the FHL rules will not apply to the property for that tax year. For those who have more than one FHL property “averaging” is permitted. Benefits of Qualifying as FHL from 6 April 2012 • Income Tax • Capital Allowances Generally, capital allowances are not available on residential let property, but they can be claimed for capital expenditure on “plant and machinery” used in your FHL. This will include furniture, furnishings, bed linen, etc. • Capital Gains Tax • Entrepreneurs’ Relief (ER) A qualifying FHL will be a trade for ER purposes. Availability of ER will be subject to the necessary conditions being met. On a qualifying business disposal you will benefit from the 10% CGT rate (up to the lifetime limit of £10 million) of Capital Gains. • Rollover Relief Property that is a qualifying asset for Rollover Relief. Broadly this means that any gain on the disposal of an FHL property can be rolled into the acquisition of another FHL property within three years to defer the Capital Gain arising. • Holdover Relief An FHL property qualifies as a business asset for Holdover Relief. The importance of this is not only the ability to hold over the gain on a Potentially Exempt Transfer of an FHL property, but also that a successful holdover claim made does not preclude the donee from subsequently claiming Principal Private Residence Relief is he occupies the property himself. • Inheritance Tax • Business Property Relief (BPR) Provided an FHL satisfies certain conditions, there is some scope for it to qualify for 100% BPR to mitigate IHT charges. • Pensions Income from an FHL is treated as relevant earnings for an individual when calculating the maximum relief for their pension contributions. • Planning Points • Elections to consider There are two elections you can make to help you reach the occupancy threshold. If you have more than one property the ‘averaging’ election might be helpful and if you have a property that reaches the occupancy threshold in some years but not in others, you could use a ‘period of grace’ election to help you to reach the threshold. The new period of grace election allows you to treat a year as a qualifying FHL year where you genuinely intended to meet the occupancy threshold but were unable to meet it. In the year before the first year you want to be treated as a qualifying FHL year the property must have reached the occupancy threshold, either on its own or because of an averaging election. If in the following year the property still doesn’t meet the occupancy threshold then, providing an election has been made for the earlier year, that year can also be treated as a qualifying FHL year. This means that you can have two years running where you failed to let for enough days. If the property still doesn’t meet the required letting level in the fourth year (after two years being treated as qualifying) then that property is no longer a FHL property. The two years in which the property was treated as qualifying, still do. We understand that further guidance on some of the more technical areas of the rules will be published in HMRC’s Property Income Manual in due course. Overview Review your property portfolio. Have you got taxable profits in some property portfolios yet losses in others ? Maybe you need to reconsider the need to qualify as an FHL. Losses on FHL businesses can only be set against the same FHL business . Whilst the HMRC Manuals state that the claim to qualify as an FHL is a beneficial claim it does not state it is a compulsory one, therefore where you have losses on residential property portfolios you may have profits on your FHL’s or vice versa. In this situation it may be more tax effective not to make a claim as an FHL and utilise the losses against residential property surpluses. Alternatively you may be considering the sale of your FHL whereby Entrepreneurs relief may be beneficial. For a free no obligation chat about how we may be able to assist you with your accounting and taxation requirements please call Simon Jeffrey on 01829 733333 or e-mail simon.jeffrey@hlbtarp.co.uk.