Leases-Accounting( AS-19)

advertisement

")

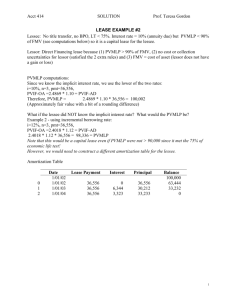

Leases-Accounting( AS-19) Finance Lease:-risk and reward transferred to lessee. Operating Lease:- Ownership not transferred to lessee. Leases-Accounting( AS-19) Definitions Guaranteed Residual Value • In respect of lessee-amount which is guaranteed by or on behalf of lessee In respect of lessor- amount which is guaranteed by or on behalf of lessee or by an independent third party Unguaranteed residual Value- difference between residual value and Guaranteed residual value. Leases-Accounting( AS-19) Gross Investment • • Minimum lease payment ( from the standpoint of lessor) and Any Unguaranteed residual value accruing to the lessor Interest rate implicit :- the discount rate at which fair value of leased asset at the inception is equal to PV of ( Min. lease payment + any unguaranteed residual value) Contingent Rent- lease rent fixed on the basis of % of sales, market rate etc. Leases-Accounting( AS-19) Minimum Lease Payment Total lease rent to be paid by lessee + any guaranteed residual valuecontingent rent-cost of service and tax to be paid by and reimbursed to lessor+ residual value guaranteed by third party( in case of lessor). Leases-Accounting( AS-19) Accounting for Finance Lease In the books of Lessee:-Leased Asset to be recognised as lower of • • • • • Fair Value of the leased asset at the inception Present Value of Minimum Lease payment Each lease payment should be apportioned as finance charge and principal amount. Depreciation to be charged on the leased asset.(AS-6) under SLM Finance Charge Dr. Lease liability account Dr. To Lease rent Leases-Accounting( AS-19) Accounting for Finance Lease In the books of Lessor:-To be recognised as a Receivable at an amount equal to net investment with credit to sale of asset. Net Investment= Gross investment-Unearned finance income Unearned Finance Income= Gross investment- present value of Gross Investment. Leases-Accounting( AS-19) Accounting for Operating Lease. In the books of Lessor:- Record Leased out asset as fixed asset in the Balance Sheet. Charge depreciation as per AS-6 Recognise lease income in P & L account using SLM. Other operating costs to be debited to P & L account Leases-Accounting( AS-19) Accounting for Operating Lease. In the books of Lessee:- Lease payment to be recognised as expense in the P & L account. Disclosures in Financial Statements: Total of future MLP in not later than one year Later than one year not later than 5 years. Later than 5 years. General Description of the leasing arrangement.