Avoiding-Commmon-Compliance-Errors

advertisement

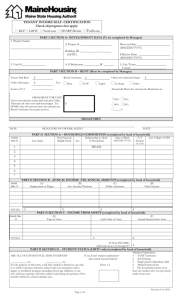

Common Section 42 Compliance Issues Presented by Matt Rayburn Compliance & Asset Manager INTRODUCTION / DISCLAIMER The purpose of this presentation is to discuss common compliance issues identified by IHCDA Compliance Auditors during tenant file reviews. This is not a full review of Section 42 compliance requirements. For additional information on IHCDA’s compliance policies, please review the 2011 Rental Housing Tax Credit Compliance Manual. For additional IRS guidance on types of noncompliance and how to remedy noncompliance, please review the 8823 Guide. TENANT FILES Tenant files not maintained in a consistent order. Tenant files do not contain all necessary documents: 1. Initial application for residency; 2. Tenant Income Certification Questionnaires for each year; 3. TICs for each year; 4. Verifications of all income and asset sources for each year; 5. Student status certifications for each year; 6. Any other documents used to verify eligibility; 7. Initial and subsequent leases and lease addenda; and 8. HAP Contract and all HAP Amendments for Section 8 voucher holders or the 50059 for project-based Section 8 tenants. LEASES •Lease contains prohibited fees or mandatory fees that are not included in the gross rent calculation on the TIC (more on both of these issues later). •Lease/lease addenda contains language stating that household will be terminated if income exceeds 140% at recertification. •Lease renewal addendum does not include new rental amount. FORMS (GENERAL COMMENTS) •Wrong forms used- IHCDA has three mandatory forms • Tenant Income Certification (TIC) = Form #22 = 1 per household • Tenant Income Certification Questionnaire = Form #23- 1 per adult member • Student Status Certification = Form #35- 1 per adult member •Forms signed but not dated •Forms backdated •Parts of forms filled in by tenant/applicant and other parts apparently filled in later by management •Whiteout or Sharpie used on forms THE TIC AND QUESTIONNAIRE Common issues with the TIC •TIC not signed by all adult household members. This is mainly a problem at recertifications when members who were previously under 18 are now older. •Effective dates do not match anniversary date of move-in •Signed and dated after the effective date Common issues with the Questionnaire •Only one form filled out per household instead of the required one per household member. •Tenant/applicant filled out all the yes/no column but did not provide any additional information on items marked as yes. TIC EXAMPLE QUESTIONNAIRE EXAMPLE THE UNDER $5000 ASSET CERTIFICATION This is the single form that is most frequently filled out incorrectly or incompletely! •Either item #2 or #3 must be checked. Both cannot be checked. •If no assets are listed on the top, item #4 must be checked. If assets are listed, item #4 cannot be checked. •Item #5 should list the total household INCOME FROM ASSETS, not the total cash value of assets. •Form must be signed by all adult household members and only one form should be completed per household. A separate form should NOT be completed by each member since we are checking that the total household assets are under $5000, not the total assets of one member. UNDER $5000 ASSET CERTIFICATION EXAMPLE VERIFICATION DOCUMENTS •Owner/management did not verify all income/assets disclosed by the household on its questionnaire •Inconsistent or vague information on questionnaire or verification documents not clarified by management •Verification documents are outdated (older than 120 days prior to effective date of certification) •Verification documents were received late (after effective date of certification) •Verification documents are incomplete, illegible, or otherwise insufficient •No evidence that management attempted third-party verifications of any kind (files all contain paystubs and bank statements) CALCULATING INCOME & ASSETS •Social Security incorrectly calculated using benefit amount before deductions •Unemployment not annualized •Year-to-date calculation not performed for employment income •Bi-weekly pay incorrectly calculated by taking bi-weekly pay amount multiplied by 24 instead of 26 •Confusion on bank accounts: savings must use current balance and checking must use 6 month average balance STUDENT STATUS •File does not contain third-party verification proving a member is a part-time student when full-time status would make the household ineligible. •File does not contain third-party verification proving an exemption is met. •File does not contain a separate student status certification for each adult household member. •Household was not all full-time students at move-in but later became all full-time students but was allowed to stay in the unit. Unlike income, student status is an ongoing eligibility determination. COMMON MISCONCEPTION • The student status rule does not apply unless all household members are full-time students. We still see companies incorrectly believe they must find an exemption if any members are full-time students or if there is a part-time student. UTILITY ALLOWANCES •PHA utility allowance not updated on time. NOTE: It is not the PHA’s responsibility to contact you when there is an update. Therefore, you need to check regularly. •PHA utility allowance confused with allowances on IHCDA’s website. •Utility company estimate confused with consumption estimate. •Rents not adjusted within 90 days of a utility allowance update. If new utility allowances cause a rent adjustment, this must be done for all affected households, even those in mid-lease. NON-OPTIONAL FEES NOT INCLUDED IN GROSS RENT CALCULATION Non-optional fees (a.k.a. mandatory fees, required fees, or condition of occupancy fees) must be included in the gross rent calculation Gross rent = tenant-paid rent portion + utility allowance + non-optional fees This total sum must be at or below the applicable rent limit Common Issues Mandatory fees not clearly defined within the lease Mandatory fees not listed on the TIC / included in gross rent calculation Most common examples Mandatory renter’s insurance Month-to-month tenancy fees Fees for services that are a condition of occupancy PROHIBITED FEES •Application fees in excess of the actual out-of-pocket expense incurred (e.g. the cost of running a credit and criminal background check). This cannot include fees for staff time spent reviewing applications or for completing income verification paperwork associated with Section 42. •Fees for preparing a unit for occupancy (e.g. redecorating fees) •Fees for the use of items included in eligible basis • Common examples include: swimming pools, clubhouses, parking, storage, etc. •Rent for residential manager, security, or maintenance units if the unit is treated as “a facility reasonably required for a project” instead of a qualified tax credit unit. APPLICABLE FRACTION VIOLATIONS •Applicable fraction off based on floor space fraction. Generally in this scenario the applicable fraction is correct based on unit fraction but is still out of compliance because larger units were rented to market households. •Applicable fraction incorrectly interpreted as a project rule instead of a building by building rule. •NOTE: Applicable fraction violations are generally detected during annual owner certification reviews, not during tenant file audits. TAX CREDIT & HOME COMBOS A full discussion of the issues that arise when combining these programs is beyond the scope of this discussion. Here are a few of the common errors found by IHCDA staff when the programs are mixed: •The lower limits (usually the HOME limits) must be used for the units that are affected by both programs. •The HOME-assisted households must be given Fair Housing and Lead-based Paint brochures upon move-in and a signed receipt must be maintained in the household’s file. •The assets of HOME-assisted households must be third-party verified regardless of whether or not the total is less than $5000. CONTACT INFORMATION Matt Rayburn Compliance and Asset Manager mrayburn@ihcda.in.gov 317-233-9564 Section 42 Compliance Staff Jeff Ivory, Senior Compliance Auditor- jivory@ihcda.in.gov Anika Davis, Compliance Auditor- andavis@ihcda.in.gov George McMannis, Compliance Auditor- gmcmannis@ihcda.in.gov Ryan Splichal, System Specialist- rysplichal@ihcda.in.gov