SESSION 2

The Conceptual

Framework

National company law

National accounting standards

GAAP (e.g.

Local stock exchange requirements (HOSE, NYSE, LSE)

IFRSs)

Non-mandatory

International accounting standards (WTO, TPP)

sources

Statutory requirements in other countries (France, Soviet union, US)

Accruals basis

Accounting basis

Going concern

Underlying assumption

Nature

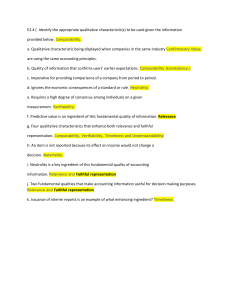

Relevance

Materiality

Fundamental

Complete

Faithful

Substance

Qualitative

Neutral

representation

over form

characteristics of

Free from error

useful financial

Comparability

information

Verifiability

Conceptual

Enhancing

Timeliness

framework

Understandability

Cost constraint

Pervasive and subjective constraint

Financial position

Probable economic benefit

Recognition

Profit or Loss

Measured with reliability

Historical cost

Elements of financial

Current cost (Replacement cost)

statements

Realisable value

Measurement

Fair value

Settlement value

Present value of future cash flows (value in use)

Links

Accounting regulations in Vietnam

http://ketoanthienung.org/tin-tuc/van-ban-phapluat-ke-toan-moi-nhat.htm

Vietnamese Accounting Standards

https://thuvienphapluat.vn/tintuc/vn/thoi-su-phapluat/chinh-sach-moi/7051/he-thong-26-chuan-mucke-toan-viet-nam

International Financial Reporting Standards

http://www.ifrs.org/issued-standards/list-ofstandards/

1 Conceptual framework and GAAP

A conceptual framework: a statement of generally

accepted theoretical principles which form the

frame of reference for financial reporting.

A conceptual framework will form the theoretical

basis for determining which events should be

accounted for, how they should be measured and

how they should be communicated to the user.

Users of accounting information consist of

investors, employees, lenders, suppliers and other

trade creditors, customers, government and their

agencies and the public.

Generally Accepted Accounting

Practice (GAAP)

GAAP signifies all the rules, from whatever source, which

govern accounting.

In individual countries this is seen primarily as a

combination of:

• National company law

• National accounting standards

• Local stock exchange requirements

Although those sources are the basis for the GAAP of

individual countries, the concept also includes the effects

of non-mandatory sources such as:

• International accounting standards

• Statutory requirements in other countries

Advantages

Lack of a conceptual framework producing

• contradictions and inconsistencies

Some standards may concentrate on profit or loss

whereas some may concentrate on the valuation of

net assets (statement of financial position).

• large number of highly detailed standards

• bolster standard setters against political pressure

http://cafef.vn/tai-chinh-ngan-hang/vamc-co-giupcac-ngan-hang-giam-no-xau-cai-thien-tinh-hinhtai-chinh-2014012112001239313.chn

Disadvantages

(a) Variety of users different purpose

(b) It is not clear that a conceptual framework

makes the task of preparing and then

implementing standards any easier than

without a framework.

The Conceptual Framework is not an IFRS and

so does not overrule any individual IFRS. In the

(rare) case of conflict between an IFRS and the

Conceptual Framework, the IFRS will prevail.

Accruals basis

The effects of transactions and other events are

recognised when they occur (and not as cash or

its equivalent is received or paid) and they are

recorded in the accounting records and reported

in the financial statements of the periods to

which they relate.

Going concern

Going concern is the underlying assumption in

preparing financial statements.

The entity is normally viewed as a going

concern, that is, as continuing in operation for

the foreseeable future. It is assumed that the

entity has neither the intention nor the

necessity of liquidation or of curtailing

materially the scale of its operations.

Qualitative characteristics of useful financial

information

The Conceptual Framework states that qualitative

characteristics are the attributes that make financial

information useful to users.

Chapter 3 of the Conceptual Framework distinguishes

between fundamental and enhancing qualitative

characteristics, for analysis purposes.

• Fundamental qualitative characteristics distinguish useful

financial reporting information from information that is not

useful or misleading.

• Enhancing qualitative characteristics distinguish more

useful information from less useful information.

The two fundamental qualitative characteristics are

relevance and faithful representation.

Relevance

Relevant information is capable of making a

difference in the decisions made by users.

The relevance of information is affected by its

nature and its materiality.

Materiality. Information is material if omitting it

or misstating it could influence decisions that

users make on the basis of financial information

about a specific reporting entity.

Faithful representation

Financial reports represent economic phenomena in

words and numbers. To be useful, financial information

must not only represent relevant phenomena but must

faithfully represent the phenomena that it purports to

represent.

To be a faithful representation information must be

complete, neutral and free from error.

• Substance over form

This is not a separate qualitative characteristic under the

Conceptual Framework. The IASB says that to do so would

be redundant because it is implied in faithful

representation. Faithful representation of a transaction is

only possible if it is accounted for according to its

substance and economic reality.

Enhancing qualitative characteristics

• Comparability relevance

• Verifiability faithfulness

• Timeliness relevance

• Understandability relevance

Classifying, characterising and presenting

information clearly and concisely makes it

understandable.

Comparability

Comparability is the qualitative characteristic

that enables users to identify and understand

similarities in, and differences among, items.

Information about a reporting entity is more

useful if it can be compared with similar

information about other entities and with

similar information about the same entity for

another period or date.

The cost constraint on useful financial

reporting

This is a pervasive constraint, not a qualitative

characteristic. When information is provided, its

benefits must exceed the costs of obtaining and

presenting it. This is a subjective area and there are

other difficulties: others, not the intended users,

may gain a benefit; also the cost may be paid by

someone other than the users. It is therefore

difficult to apply a cost-benefit analysis, but

preparers and users should be aware of the

constraint.

Asset. A resource controlled by an entity as a result

of past events and from which future economic

benefits are expected to flow to the entity.

Liability. A present obligation of the entity arising

from past events, the settlement of which is

expected to result in an outflow from the entity of

resources embodying economic benefits.

Equity. The residual interest in the assets of the

entity after deducting all its liabilities.

Recognition of the elements of financial

statements

Items which meet the definition of assets or liabilities

may still not be recognised in financial statements

because they must also meet certain recognition criteria.

Recognition. The process of incorporating in the

statement of financial position or statement of profit or

loss and other comprehensive income an item that meets

the definition of an element and satisfies the following

criteria for recognition:

(a) It is probable that any future economic benefit

associated with the item will flow to or from the entity

(b) The item has a cost or value that can be measured

with reliability

Assets which cannot be recognised

The recognition criteria do not cover items which

many businesses may regard as assets.

A skilled workforce is an undoubted asset but

workers can leave at any time so there can be no

certainty about the probability of future economic

benefits.

A company may have come up with a new name for

its product which is greatly increasing sales but, as

it did not buy the name, the name does not have a

cost or value that can be reliably measured, so it is

not recognised.

Measurement of the elements of

financial statements

A number of different measurement bases are

used in financial statements. They include:

– Historical cost

– Current cost

– Realisable (settlement) value

– Present value of future cash flows

Historical cost. Assets are recorded at the amount of cash or cash equivalents paid or

the fair value of the consideration given to acquire them at the time of their

acquisition. Liabilities are recorded at the amount of proceeds received in exchange

for the obligation, or in some circumstances (for example, income taxes), at the

amounts of cash or cash equivalents expected to be paid to satisfy the liability in the

normal course of business.

Current cost (replacement cost). Assets are carried at the amount of cash or cash

equivalents that would have to be paid if the same or an equivalent asset was

acquired currently.

Liabilities are carried at the undiscounted amount of cash or cash equivalents that

would be required to settle the obligation currently.

Fair value, which is defined by IFRS 13 as 'the price that would be received to sell an

asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date'.

• Realisable value. The amount of cash or cash equivalents that could currently be

obtained by selling an asset in an orderly disposal.

• Settlement value. The undiscounted amounts of cash or cash equivalents

expected to be paid to satisfy the liabilities in the normal course of business.

Present value. A current estimate of the present discounted value of the future net

cash flows in the normal course of business

Example

A machine was purchased on 1 January 20X8 for $3m. That was its original cost. It has a

useful life of 10 years and under the historical cost convention it will be carried at original

cost less accumulated depreciation. So in the financial statements at 31 December 20X9

it will be carried at:

$3m – (0.3 x 2) = $2.4m (carrying value, net book value)

The replacement cost of the machine will be the cost of a new model less two year's

depreciation. The cost of a new machine may now be $3.5m. Assuming a ten-year life, the

replacement cost will therefore be $2.8m.

The current cost of the machine, which will probably also be its fair value, will be fairly

easy to ascertain if it is not too specialised. For instance, two year old machines like this

one may currently be changing hands for $2.5m, so that will be an appropriate fair value.

The net realisable value of the machine will be the amount that could be obtained from

selling it, less any costs involved in making the sale. If the machine had to be dismantled

and transported to the buyer's premises at a cost of $200,000, the NRV would be $2.3m.

The present value of the machine will be the discounted value of the future cash flows

that it is expected to generate. If the machine is expected to generate $500,000 per

annum for the remaining eight years of its life and if the company's cost of capital is 10%,

present value will be calculated as:

$500,000 x 5.335* = $2667,500

* Cumulative present of $1 per annum for eight years discounted at 10%

0

0