PROVISIONS,

CONTINGENT

LIABILITIES AND

CONTINGENT ASSETS

Kiara Cerisse C. Singian, CPA

Learning Objectives

▪ State the recognition criteria for provisions.

▪ Differentiate the accounting requirements of a provision, a contingent liability and a

contingent asset.

▪ Describe the available measurement bases for a provision.

▪ Account for provisions.

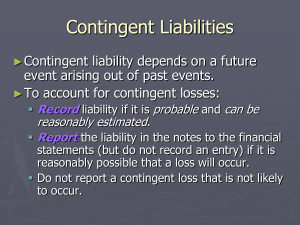

Provisions

▪ A provision is a liability of uncertain timing or amount.

▪ Provisions differ from other liabilities because of the uncertainty about the timing or

amount of expenditure required in settlement. Unlike for other liabilities, provisions

must be estimated. Although, some other liabilities are also estimated, their

uncertainty is generally much less than for provisions.

▪ Other liabilities, such as accruals, are reported as part of “Trade and other

payables” whereas provisions are reported separately.

Provision vs. Contingent liability

Provision

Contingent liability

▪ Present obligation

▪ Possible obligation

▪ Probable and measured reliably

▪ Present obligation but not probable or

Present obligation but not measured

▪ Recognized (accrued in the statement of

financial position)

reliably

▪ Not recognized (not accrued in the

statement of financial position)

Recognition of provisions

▪ A provision is recognized when all of the following conditions are met:

1.

The entity has a present obligation (legal or constructive) as a result of a past

event;

2.

It is probable that an outflow of resources embodying economic benefits will be

required to settle the obligation; and

3.

A reliable estimate can be made of the amount of the obligation.

Range of outcome

Present obligation is

Recognize or accrue a

outflow of economic

both probable and reliably

estimable.

Provide appropriate

The future event is likely to

As a rule of thumb,

means more than 50%

Present obligation is

Disclose only a contingent

liability.

Present obligation is remote

Do nothing.

Do not recognize or accrue

liability.

The future event is less

occur. The occurrence is

less.

The future event is least

occur or the chance of the

event occurring is very

occurrence is 10% or less.

Measurement

Nature of the outflow

Measurement basis

1. General rule

➢ Best estimate

2. Involves a large population of items

➢ Expected value (Probability Weighted

3. Each possible outcome in a range is as

any other

➢ Mid-point

Present value

▪ Where the effect of the time value of money is material, the amount of a provision

shall be the present value of the expenditures expected to be required to settle the

obligation.

Expected disposal of assets

▪ Gains from the expected disposal of assets shall not be taken into account in

measuring a provision. Gains shall be recognized only when the assets are actually

disposed of.

Reimbursements

▪ Where some or all of the expenditure required in settling a provision is expected to

be reimbursed by another party, the reimbursement is recognized only when it is

virtually certain that reimbursement will be received if the entity settles the

obligation.

▪ The reimbursement shall be treated as a separate asset.

▪ In the statement of profit or loss and other comprehensive income, the expense

relating to a provision may be presented net of the amount recognized for a

reimbursement.

Changes in provisions

▪ Provisions shall be reviewed at the end ▪ If it is no longer probable that an outflow

of each reporting period and adjusted to of resources embodying economic

reflect the current best estimate.

benefits will be required to settle the

obligation, the provision shall be

reversed.

Product warranties and guarantees

▪ If a customer has the option to purchase ▪ If a customer does not have the option

a warranty separately (for example,

to purchase a warranty separately, the

because the warranty is priced or

warranty is accounted for in accordance

negotiated separately), the warranty is

with PAS 37 Provisions, Contingent

accounted for in accordance with PFRS

Liabilities and Contingent Assets unless

15 Revenue from Contracts with

the promised warranty provides the

Customers.

customer with a service in addition to

the assurance that the product complies

with agreed-upon specifications.

Liability for premiums

▪ A customer option to acquire additional ▪ A customer option that does not provide

goods or services for free or at a

the customer with a material right is not

discount is accounted for under PFRS 15 accounted for under PFRS 15; and

if the option provides the customer a

therefore, accounted for in accordance

material right that the customer would

with PAS 37.

not receive without entering into that

contract.

Guarantee for indebtedness of others

▪ A provision for the guarantee for indebtedness of others is recognized when it

becomes probable that the entity will be held liable for the guarantee, such as when

the original debtor defaults on the loan.

Contingent assets

Contingent asset is probable Contingent asset is possible

Contingent asset is remote

Disclose only a contingent

Do not recognize or accrue.

Do nothing.

Do nothing.

APPLICATION OF CONCEPTS

Application of Concepts

Fact Pattern:

Transcribe Co. is engaged in transport services. A lawsuit was filed against Transcribe

Co. regarding a road accident that occurred late in December 20x1. Transcribe Co.'s

legal counsel believes that Transcribe Co. will probably lose the case and pay

damages. Sufficient data is available to make a reliable estimate of the damages.

Should Transcribe Co, accrue a provision on December 31, 20x1? Provide a brief

explanation of your answer.

Application of Concepts

1. Answer: Yes. All the elements of the recognition criteria are met:

a. Present obligation arising from past event – an accident already happened, and a lawsuit was filed

against the entity.

b. Probable outflow – the entity expects to lose the case and pay damages.

c. Reliable estimate – the problem states that “Sufficient data is available to make a reliable

estimate of the damages.”

Application of Concepts

Fact Pattern:

Transcribe Co. is engaged in transport services. A lawsuit was filed against Transcribe

Co. regarding a road accident that occurred late in December 20x1. Transcribe Co.'s

legal counsel believes that Transcribe Co. will probably lose the case and pay

damages. Sufficient data is available to make a reliable estimate of the damages.

Transcribe Co.'s best estimate of the payment for damages is P4M. What is the entry

to accrue the provision?

Application of Concepts

Dec.

31,

20x1

Probable loss on lawsuit

Estimated liability on pending lawsuit

4,000,000

4,000,000

Application of Concepts

Fact Pattern:

Transcribe Co. is engaged in transport services. A lawsuit was filed against Transcribe

Co. regarding a road accident that occurred late in December 20x1. Transcribe Co.'s

legal counsel believes that Transcribe Co. will probably lose the case and pay

damages. Sufficient data is available to make a reliable estimate of the damages.

Transcribe Co.'s legal counsel believes that there is a 20% chance that Transcribe Co.

will win the case. If, however, Transcribe Co. will lose, there is a 30% chance that it will

pay damages of P9M (the amount sought by the plaintiff) and a 70% chance that it will

pay damages of P4M (the amount awarded to the plaintiff in a similar case that was

recently concluded). Other outcomes, are unlikely. A 4% risk adjustment factor is

considered appropriate to reflect the uncertainties in the cash flow estimates. The

court decision is expected to be finalized in December 20x2. The appropriate discount

rate is 12%. What is the entry to accrue the provision?

Application of Concepts

Dec.

31,

20x1

Probable loss on lawsuit

Estimated liability on pending lawsuit

4,085,714

4,085,714

Application of Concepts

Fact Pattern:

Transcribe Co. is engaged in transport services. A lawsuit was filed against Transcribe

Co. regarding a road accident that occurred late in December 20x1. Transcribe Co.'s

legal counsel believes that Transcribe Co. will probably lose the case and pay

damages. Sufficient data is available to make a reliable estimate of the damages.

Transcribe Co.'s legal counsel believes that Transcribe Co. will probably pay damages

of not less than P2M but not more than P7M. The probability of any amount within the

range is as likely as any other amount within that range. The plaintiff is offering an

out-of-court settlement of P6.2M but Transcribe Co. does not agree. What is the entry

to accrue the provision?

Application of Concepts

Dec.

31,

20x1

Probable loss on lawsuit [(2M + 7M) / 2]

Estimated liability on pending lawsuit

4,500,000

4,500,000

Application of Concepts

On December 31, 20x1, Aural Co. accrues a provision of P5M for an expected loss on

a pending labor case. On December 31, 20x2, Aural Co. reviews its estimate and

concludes that an estimate of P4.8M is more appropriate. The case is settled in 20x3

and Aural Co. pays damages of P5.1M. Provide the journal entries in 20x1 to 20x3.

Application of Concepts

Dec.

31,

20x1

Probable loss on lawsuit

Estimated liability on pending lawsuit

5,000,000

Dec.

31,

20x2

Estimated liability on pending lawsuit

Gain on revision of estimate

200,000

20x3

Estimated liability on pending lawsuit

Loss on lawsuit

Cash

4,800,000

300,000

5,000,000

200,000

5,100,000

Application of Concepts

Ear Co. provides 5-year warranty for its products. Warranty costs, related to sales, are

estimated at 2% in the year of sale and 4% in the subsequent years. The warranty

obligation has a balance of P160,000 as of January 1, 20x1. Information for 20x1 and

20x2 is as follows:

Year

Sales

Actual warranty costs

20x1

P10,000,000

P400,000

20x2

12,000,000

500,000

Requirements:

a.

Provide the journal entries in 20x1 and 20x2 to record the actual warranty costs

and the provisions for warranty obligation.

b.

Compute for the balance of the warranty obligation on December 31, 20x2.

Application of Concepts

20x1

Warranty expense (10M x 6% (a))

Warranty obligation

600,000

Warranty obligation

Cash (or other asset account)

400,000

to record the provision for warranty costs

to record the actual warranty costs

(a)

600,000

400,000

2% + 4% = 6%

20x2

Warranty expense (12M x 6%)

Warranty obligation

720,000

Warranty obligation

Cash (or other asset account)

500,000

to record the provision for warranty costs

to record the actual warranty costs

720,000

500,000

Application of Concepts

Application of Concepts

Listen Co. has an ongoing sales promotion. For every five bottle crowns returned to Listen

Co., customers receive a T-shirt. The unit cost of the T-shirt is P100. Listen Co. estimates

that 80% of sales will be redeemed. Listen Co.'s premium liability as of December 31, 20x0

is P720,000. Additional information is as follows:

Units

Sales in 20x1

500,000

Sales in 20x2

900,000

T-shirts distributed in 20x1

60,000

T-shirts distributed in 20x2

147,000

Requirements:

a.

Provide the journal entries in 20x1 and 20x2 to record the actual costs of premiums

distributed and the provisions for premium liability.

b.

Compute for the balance of the premium liability on December 31, 20x2.

Application of Concepts

20x1

Premium expense [(500K x 80% ÷ 5) x ₱100 )]

Estimated liability for premiums

8,000,000

Estimated liability for premiums

(60,000 T-shirts x ₱100)

Premiums

6,000,000

to record the provision for premiums

8,000,000

6,000,000

to record the actual premiums distributed

20x2

Premium expense [(900,000 x 80% ÷ 5) x ₱100]

Estimated liability for premiums

14,400,000

Estimated liability for premiums

(147,600 T-shirts x ₱100)

Premiums

14,760,000

to record the provision for premiums

to record the actual premiums distributed

14,400,000

14,760,000

Application of Concepts

Application of Concepts

On January 1, 20x1, Loving Co. guaranteed a bank loan of Shameless Co. amounting

to P1,000,000. On December 31. 20x1, Shameless Co. defaulted, and it has become

probable that Loving Co. will be held liable to the bank for P1,000,000. What are the

journal entries in Loving Co.'s books in 20x1?

Application of Concepts

Jan. 1, No entry

20x1

Dec.

31,

20x1

Probable loss on guarantee

Estimated liability for guarantee

1,000,000

1,000,000

QUESTIONS?

0

0