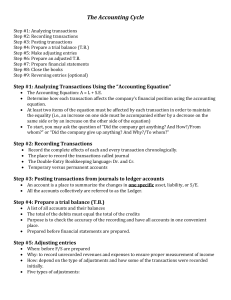

4 Accrual Accounting Concepts Kimmel ● Weygandt ● Kieso Accounting, Sixth Edition 4-1 CHAPTER OUTLINE LEARNING OBJECTIVES 4-2 1 Explain the accrual basis of accounting and the reasons for adjusting entries. 2 Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for accruals. 4 Prepare an adjusted trial balance and closing entries. 4-3 LEARNING OBJECTIVE 1 Explain the accrual basis of accounting and the reasons for adjusting entries. Accountants divide the economic life of a business into artificial time periods Periodicity/Time Period Assumption. Jan. 4-4 Feb. Mar. Apr. ..... Dec. Generally a month, a quarter, or a year. LO 1 ACCRUAL VERSUS CASH BASIS Accrual-Basis Accounting ► Transactions recorded in the periods in which the events occur. Companies recognize revenues when they perform services (rather than when they receive cash). Expenses are recognized when incurred (rather than when paid). 4-5 LO 1 ACCRUAL VERSUS CASH BASIS Cash-Basis Accounting Revenues are recorded when cash is received. Expenses are recorded when cash is paid. Cash-basis accounting is not in accordance with generally accepted accounting principles (GAAP). Only micro-businesses might use it as well as government entities (MoF accrual accounting project) 4-6 LO 1 MoF accrual accounting project Saudi Arabia’s adoption of the accrual basis accounting program aims to play an effective role in providing financial data that help measure performance, analyze gaps and seize available opportunities in light of financial performance. The Kingdom’s transition from cash to accrual accounting was not just a technical requirement. It will help developing effective financial policies. In addition, the successful shift will allow the government entities to have an integrated financial system, based on international accounting standards for public sector called: 4-7 International Public Sector Accounting Standards (IPSAS) ACCRUAL VERSUS CASH BASIS Illustration: Suppose that Fresh Colors paints a large building in 2016. In 2016, it incurs and pays total expenses (salaries and paint costs) of $50,000. It bills the customer $80,000, but does not receive payment until 2017. 2016 ILLUSTRATION 4-2 Accrual-versus cash-basis accounting 4-8 2017 LO 1 Recognizing Revenues and Expenses Illustration 3-1 GAAP relationships in revenue and expense recognition 4-9 LO 1 THE NEED FOR ADJUSTING ENTRIES Adjusting entries 4-10 Ensure that the revenue recognition and expense recognition principles are followed. Necessary because the trial balance may not contain up-to-date and complete data. Required every time a company prepares financial statements. LO 1 Types of Adjusting Entries Deferrals Accruals Prepaid Expenses + Supplies 1. Accrued Revenues. + Depreciation Expenses paid in Revenues for services cash and recorded as assets before they performed but not yet are used or consumed. received in cash. 1. (Expenses paid in advance) 2. Unearned Revenues. Cash received before services are performed. (Revenues received in advance) (Owned Revenues, no cash yet) 2. Accrued Expenses. Expenses incurred but not yet paid in cash. (Owned Expenses, no cash yet) Illustration 3-2 Categories of adjusting entries 4-11 LO 1 Adjusting Entries for Deferrals Made to record expenses or revenues that are recognized at a date later than the point when cash was originally exchanged. There are two types: Prepaid expenses (including supplies and depreciation) OR 4-12 Unearned revenues LO 3 Prepaid Expenses Expenses paid in cash before they are used or consumed. Cash Payment BEFORE Expense Recorded Prepayments often occur in regard to: 4-13 insurance rent supplies equipment advertising buildings LO 2 Prepaid Expenses Prepaid Expenses Costs that expire either with the passage of time or through use. Adjusting entry: ► Increase (debit) to an expense account and ► Decrease (credit) to a prepaid expense account. 4-14 LO 2 Prepaid Expenses_1 Illustration: On October 1, Pioneer Advertising Inc. paid $600 for a one-year fire insurance policy. Pioneer recorded the payment by increasing (debiting) Prepaid Insurance. This account shows a balance of $600 in the October 31 trial balance. Insurance of $50 ($600 ÷ 12) expires each month. Oct. 1 Prepaid Insurance 600 Cash Oct. 31 Insurance Expense Prepaid Insurance 4-15 600 50 50 LO 2 Prepaid Expenses_1 Illustration 3-6 4-16 LO 2 Prepaid Expenses_2 (Supplies) Illustration: Pioneer Advertising Inc. Inc. purchased supplies costing $2,500 on October 5. Pioneer recorded the purchase by increasing (debiting) the asset Supplies. This account shows a balance of $2,500 in the October 31 trial balance. An inventory count at the close of business on October 31 reveals that $1,000 of supplies are still on hand. Oct. 31 Supplies Expense Supplies 4-17 1,500 1,500 LO 2 Prepaid Expenses_2 Illustration 3-5 4-18 LO 2 Prepaid Expenses_3 (Depreciation) Buildings, equipment, and motor vehicles (long-lived assets) are recorded as assets, rather than an expense, in the year acquired. Depreciation is the process of allocating the cost of an asset to expense (depreciation) over its useful life. Depreciation does not attempt to report the actual change in the value of the asset. 4-19 LO 2 Prepaid Expenses_3 (Depreciation) Illustration: For Pioneer Advertising, assume that depreciation on the equipment is $480 a year, or $40 per month. Oct. 31 Depreciation Expense 40 Accumulated Depreciation 40 Accumulated Depreciation is called a contra asset account. 4-20 Helpful Hint All contra accounts have increases, decreases, and normal balances opposite to the account to which they relate. LO 2 Prepaid Expenses_3 (Depreciation) Illustration 3-7 4-21 LO 2 Prepaid Expenses_3 (Depreciation) Statement Presentation 4-22 Accumulated DepreciationEquipment is a contra asset account. Appears just after the account it offsets (Equipment) on the balance sheet. ▼ HELPFUL HINT All contra accounts have increases, decreases, and normal balances opposite to the account to which they relate. ILLUSTRATION 4-9 Balance sheet presentation of accumulated depreciation LO 2 Unearned Revenues Receipt of cash recorded as a liability before services are performed. Cash Receipt BEFORE Revenue Recorded Unearned revenues often occur in regard to: 4-23 rent magazine subscriptions airline tickets customer deposits LO 2 Unearned Revenues Adjusting entry is made to record the revenue for services performed during the period and to show the liability that remains at the end of the accounting period. Results in a decrease to unearned revenues account (so debited because it is a liability account) and an increase to revenue account (so credited because it is a revenue account). 4-24 LO 2 Unearned Revenues Illustration: Pioneer Advertising Inc. received $1,200 on October 2 from R. Knox for advertising services expected to be completed by December 31. Unearned Service Revenue shows a balance of $1,200 in the October 31 trial balance. Analysis reveals that the company performed $400 of services in October. Oct. 2 Cash 1,200 Unearned Service Revenue Oct. 31 Unearned Service Revenue Service Revenue 4-25 1,200 400 400 LO 2 Unearned Revenues Illustration 3-11 4-26 LO 2 Debit Assets Expenses Credit Liabilities Equity * Revenues Prepaid Expenses Unearned Revenues Supplies Depreciation Expense 4-27 Accumulated Depreciation DO IT! 2 Adjusting Entries for Deferrals The ledger of Hammond, Inc. on March 31, 2017, includes these selected accounts before adjusting entries are prepared. Debit Credit Prepaid Insurance Supplies Equipment Accumulated Depreciation—Equipment Unearned Service Revenue $ 3,600 2,800 25,000 $5,000 9,200 An analysis of the accounts shows the following. 1. Insurance expires at the rate of $100 per month. 2. Supplies on hand total $800. 3. The equipment depreciates $200 a month. 4. During March, services were performed for $4,000 of the unearned service revenue reported. Prepare the adjusting entries for the month of March. 4-28 LO 2 DO IT! 2 Adjusting Entries for Deferrals The ledger of Hammond, Inc. on March 31, 2017, includes these selected accounts before adjusting entries are prepared. Debit Credit Prepaid Insurance Supplies Equipment Accumulated Depreciation—Equipment Unearned Service Revenue $ 3,600 2,800 25,000 $5,000 9,200 Prepare the adjusting entries for the month of March. 1. Insurance expires at the rate of $100 per month. SOLUTION Insurance Expense Prepaid Insurance 4-29 100 100 LO 2 DO IT! 2 Adjusting Entries for Deferrals The ledger of Hammond, Inc. on March 31, 2017, includes these selected accounts before adjusting entries are prepared. Debit Credit Prepaid Insurance Supplies Equipment Accumulated Depreciation—Equipment Unearned Service Revenue $ 3,600 2,800 25,000 $5,000 9,200 Prepare the adjusting entries for the month of March. 2. Supplies on hand total $800. SOLUTION Supplies Expense Supplies 4-30 2,000 2,000 LO 2 DO IT! 2 Adjusting Entries for Deferrals The ledger of Hammond, Inc. on March 31, 2017, includes these selected accounts before adjusting entries are prepared. Debit Credit Prepaid Insurance Supplies Equipment Accumulated Depreciation—Equipment Unearned Service Revenue $ 3,600 2,800 25,000 $5,000 9,200 Prepare the adjusting entries for the month of March. 3. The equipment depreciates $200 a month. SOLUTION Depreciation Expense Accumulated Depreciation 4-31 200 200 LO 2 DO IT! 2 Adjusting Entries for Deferrals The ledger of Hammond, Inc. on March 31, 2017, includes these selected accounts before adjusting entries are prepared. Debit Credit Prepaid Insurance Supplies Equipment Accumulated Depreciation—Equipment Unearned Service Revenue $ 3,600 2,800 25,000 $5,000 9,200 Prepare the adjusting entries for the month of March. 4. During March, services were performed for $4,000 of the unearned service revenue reported. SOLUTION Unearned Service Revenue Service Revenue 4-32 4,000 4,000 LO 2 Adjusting Entries for Accruals Accruals are made to record: Revenues for services performed but not yet recorded at the statement date (accrued revenues). (Owned Revenues, no cash received yet) OR Expenses incurred but not yet paid or recorded at the statement date (accrued expenses). (Owned Expenses, no cash paid yet) 4-33 LO 3 ACCRUED REVENUES Revenues for services performed but not yet received in cash or recorded. Adjusting entry results in: Revenue Recorded BEFORE Cash Receipt Accrued revenues often occur in regard to: 4-34 rent interest services performed LO 3 ACCRUED REVENUES Illustration: In October, Pioneer Advertising Inc. performed services worth $200 that were not received from clients in October. Oct. 31 Accounts Receivable 200 Service Revenue 200 On November 10, Pioneer receives cash of $200 for the services performed. Nov. 10 Cash Accounts Receivable 4-35 200 200 LO 3 ACCRUED REVENUES Illustration 3-14 4-36 LO 3 ACCRUED EXPENSES Expenses incurred but not yet paid in cash or recorded. Adjusting entry results in: Expense Recorded BEFORE Cash Payment Accrued expenses often occur in regard to: 4-37 Interest utilities taxes salaries LO 3 ACCRUED EXPENSES Illustration: Pioneer Advertising Inc. signed a three-month note payable in the amount of $5,000 on October 1. The note requires Pioneer to pay interest at an annual rate of 12%. Thus, the accrued interest expense (interest payable) is: Illustration 3-17 Oct. 31 Interest Expense Interest Payable 4-38 50 50 LO 3 ACCRUED EXPENSES Illustration 3-18 4-39 LO 3 ACCRUED EXPENSES (Accrued Salaries) Illustration: Sierra Corporation last paid employees' salaries on October 26 but the accrued salaries at October 31 are $1,200. Thus, the accrued salaries & wages expense is: Oct. 31 Salaries and Wages Expense Salaries and Wages Payable 1,200 1,200 ILLUSTRATION 4-21 4-40 LO 3 ACCRUED EXPENSES (Accrued Salaries) Illustration 3-20 4-41 LO 3 Debit Assets Expenses Credit Liabilities Equity * Revenues Accrued Revenues (receivable) 4-42 Accrued Expenses (payable) DO IT! 3 Adjusting Entries for Accruals Micro Computer Services Inc. began operations on August 1, 2017. At the end of August 2017, management attempted to prepare monthly financial statements. The following information relates to August. 1. At August 31, the company owed its employees $800 in salaries that will be paid on September 1. 2. On August 1, the company borrowed $30,000 from a bank on a 15-year mortgage. The annual interest rate is 10%. 3. Revenue for services performed but unrecorded for August totaled $1,100. Prepare the adjusting entries needed at August 31, 2017. 4-43 LO 3 DO IT! 3 Adjusting Entries for Accruals Micro Computer Services Inc. began operations on August 1, 2017. At the end of August 2017, management attempted to prepare monthly financial statements. Prepare the adjusting entries needed at August 31, 2017. 1. At August 31, the company owed its employees $800 in salaries that will be paid on September 1. SOLUTION Salaries and Wages Expense Salaries and Wages Payable 4-44 800 800 LO 3 DO IT! 3 Adjusting Entries for Accruals Micro Computer Services Inc. began operations on August 1, 2017. At the end of August 2017, management attempted to prepare monthly financial statements. Prepare the adjusting entries needed at August 31, 2017. 2. On August 1, the company borrowed $30,000 from a bank on a 15-year mortgage. The annual interest rate is 10%. SOLUTION Interest Expense Interest Payable 4-45 250 250 LO 3 DO IT! 3 Adjusting Entries for Accruals Micro Computer Services Inc. began operations on August 1, 2017. At the end of August 2017, management attempted to prepare monthly financial statements. Prepare the adjusting entries needed at August 31, 2017. 3. Revenue for services performed but unrecorded for August totaled $1,100. SOLUTION Accounts Receivable Service Revenue 4-46 1,100 1,100 LO 3 Using T-Account Debit Credit Assets Liabilities Expenses Equity * Revenues 4-47 Accrued Revenues Accrued Expenses Prepaid Expenses Supplies Unearned Revenues Depreciation Expense Accumulated Depreciation *: Dividends are debit account because they decrease equity LEARNING OBJECTIVE Analyze business transactions Adjusted trial balance 4-48 4 Prepare an adjusted trial balance and closing entries. Journalize Prepare financial statements Post Trial Balance Journalize and post closing entries Adjusting Entries Prepare a postclosing trial balance LO 4 PREPARE ADJUSTED TRIAL BALANCE After all adjusting entries are journalized and posted the company prepares another trial balance from the ledger accounts (Adjusted Trial Balance). The adjusted trial balance’s purpose is to prove the equality of debit balances and credit balances in the ledger. The adjusted trial balance is the primary basis for the preparation of the financial statements. 4-49 LO 4 ILLUSTRATION 4-26 Adjusted trial balance 4-50 LO 4 PREPARING FINANCIAL STATEMENTS Financial statements are prepared directly from the Adjusted Trial Balance. Income Statement 4-51 Retained Earnings Statement Balance Sheet LO 4 4-68 4-52 ILLUSTRATION 4-27 Preparation of the income statement and retained earnings statement from the adjusted trial balance 4-53 ILLUSTRATION 4-28 Preparation of the balance sheet from the adjusted trial balance LO 4 Group activity 4-54 Prepare the following statements: 1- Income Statement 2- Retained Earning Statement 3- Balance Sheet Income Statement 4-55 Retained Earning Statement 4-56 Balance Sheet & Equity 4-57 CLOSING THE BOOKS At the end of the accounting period, companies transfer the temporary account balances to the permanent stockholders’ equity account—Retained Earnings. ILLUSTRATION 4-29 Temporary versus permanent accounts 4-58 LO 4 Preparing Closing Entries In addition to updating Retained Earnings to its correct ending balance, closing entries produce a zero balance in each temporary account. ILLUSTRATION 4-30 The closing process 4-59 LO 4 4-60 ILLUSTRATION 4-31 LO 4 Preparing Closing Entries Illustration 4-32 Posting of closing entries 4-61 LO 4 Preparing a Post-Closing Trail Balance The purpose of the post-closing trial balance is to prove the equality of the permanent account balances that the company carries forward into the next accounting period. All temporary accounts will have zero balances. 4-62 LO 4 DO IT! 4b Closing Entries Hancock Company has the following balances in selected accounts of its adjusted trial balance. Accounts Payable Service Revenue Rent Expense Salaries and Wages Expense $27,000 98,000 22,000 51,000 Dividends $15,000 Retained Earnings 42,000 Accounts Receivable 38,000 Supplies Expense 7,000 Prepare the entries to close the revenue and expense accounts. SOLUTION 4-63 Service Revenue Income Summary 98,000 Income Summary Salaries and Wages Expense Rent Expense Supplies Expense 80,000 98,000 51,000 22,000 7,000 LO 4 DO IT! 4b Closing Entries Hancock Company has the following balances in selected accounts of its adjusted trial balance. Accounts Payable Service Revenue Rent Expense Salaries and Wages Expense $27,000 98,000 22,000 51,000 Dividends $15,000 Retained Earnings 42,000 Accounts Receivable 38,000 Supplies Expense 7,000 Prepare the entries to close income summary and dividends. SOLUTION 4-64 Income Summary Retained Earnings 18,000 Retained Earnings Dividends 15,000 18,000 15,000 LO 4 SUMMARY OF THE ACCOUNTING CYCLE 1. Analyze business transactions 4-65 9. Prepare a post-closing trial balance 2. Journalize the transactions 8. Journalize and post closing entries 3. Post to ledger accounts 7. Prepare financial statements 4. Prepare a trial balance 6. Prepare an adjusted trial balance 5. Journalize and post adjusting entries: Deferrals/Accruals ILLUSTRATION 4-33 Required steps in the accounting cycle LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-66 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-67 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-68 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-69 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-70 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-71 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-72 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-73 LO 4 SUMMARY OF THE ACCOUNTING CYCLE ILLUSTRATION 4-33 Required steps in the accounting cycle 4-74 LO 4 COPYRIGHT “Copyright © 2016 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.” 4-75