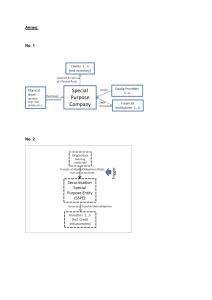

Concept Paper: The Case for Securitization in Kenya Executive Summary This concept paper explores the transformative potential of securitization in Kenya’s financial landscape. It provides a comprehensive overview of securitization, outlining its process, objectives, and benefits. By leveraging securitization, institutions can address critical challenges such as liquidity constraints, government debt, and underdeveloped investment markets, while fostering economic resilience. The paper delves into specific applications of securitization in Kenya, including microfinance institutions, auto loan companies, mobile money receivables, and bank loans. These models showcase how securitization can unlock capital, diversify investment options, and attract both local and foreign investors. Furthermore, a comparative analysis highlights Kenya’s advantages over other emerging markets, emphasizing the country’s conducive regulatory framework, growing market demand, and dynamic credit needs. The paper concludes that securitization is not only viable but essential for addressing Kenya’s fiscal and economic challenges, offering a pathway to a more robust and inclusive financial system. An Overview of Securitization What is it? Securitization is the process by which sovereign entities(governments) or financial institutions convert their illiquid assets such as loans, mortgages and other receivables in to tradable securities. This process involves several key steps and entities that will be expounded upon below. How does it work? 1. Origination- A lender, also known as the originator, (which can be any companies or entities that are characterized by financial stability as well as standardized and centralized servicing of debt) give loans to lenders and overtime develop a portfolio of illiquid return earning assets 2. Special Purpose Vehicle- The originator then sells this portfolio of loans to a Special Purpose Vehicle. The special purpose vehicle (SPV) is an independent, specially formed, single-purpose entity that purchases the loans from the originator. The SPV must be insulated to ensure that events that happen to the originator, such as bankruptcy, do not affect it. This is referred to as making the SPV ‘bankruptcy remote’. Secondly, it must be ensured that the transfer of funds from the originator to the SPV cannot be interfered with. This is achieved through a ‘true sale’ of receivables. 3. Structuring and Credit Enhancement- The SPV divides these loans into slices called tranches which are arranged based on common characteristics such as size, term or risk levels determined by a Credit Rating Agency. The SPV may enhance the creditworthiness of the securities through mechanisms such as over collateralization, third party guarantees, among several others. 4. Issuance of securities- The SPV finally issues the relevant Asset Backed Securities to investors, whose capital investment is used by the SPV to pay the Originator for the loans. 5. Distribution- Investment banks or brokers facilitate the sale of these securities to investors, such as pension funds, insurance companies, and retail investors. 6. Servicing and Monitoring- A servicer, often the original lender, manages the underlying assets, ensuring loan repayments and distributing cash flows to investors. 7. Repayment and Maturity- Investors receive periodic payments based on the performance of the underlying assets until the maturity of the assets. What was the purpose of Securitization Securitization was invented to address key challenges in financial markets, particularly the need for liquidity, risk management, and efficient capital allocation. Its origins trace back to the United States in the 1970s when banks faced liquidity shortages and interest rate mismatches. These issues arose because banks issued fixed-rate mortgages but funded them with short-term, floating-rate deposits, leading to financial strain during periods of inflation. The process of securitization, which involves pooling illiquid financial assets like mortgages or loans and converting them into marketable securities, allowed banks to offload these assets. This freed up capital, enabling them to issue more loans and manage risks better. It also created new investment opportunities for institutional investors by offering securities with varying risk profiles, tailored to their preferences. Over time, securitization expanded globally as a tool to enhance liquidity, diversify risk, and meet the growing demand for credit in both developed and emerging markets. Why is Securitization relevant to the Kenyan Market? Securitization offers a transformative opportunity for Kenya’s financial system, especially in addressing critical challenges such as liquidity constraints, government debt burden, and underdeveloped investment markets. The regulatory frameworks exist and so do the two most fundamental drivers of Securitizations success according to several authors such as A Saayman(2005) which are: (i) when regulations favour securitisation or (ii) when there exists a strong demand for and supply of asset- and mortgage-backed securities. By embracing securitization, Kenya can unlock capital, attract foreign and local investments, and strengthen its financial sector amidst growing regulatory and economic pressures. Addressing Liquidity Challenges Kenya’s banking sector is grappling with liquidity pressures as highlighted by the December 2024 report on the capital shortfalls facing 12 banks. These institutions must raise a combined Ksh11.85 billion by December 2025 to meet the new minimum core capital requirement of Ksh3 billion, with the threshold set to rise to Ksh10 billion by 2029. This regulatory pressure underscores a pressing need for innovative solutions to bolster capital reserves and enhance resilience. The solution that the Central Bank of Kenya gave was to lower the minimum reserve requirements for Banks but this can have devastating effects on the macroeconomic stability of Kenya. Securitization provides a more practical lifeline by enabling banks to convert illiquid assets, such as loan portfolios, into tradeable securities. By selling these securities to investors, banks can free up capital, reduce their balance sheet risks, and meet regulatory requirements without relying solely on costly equity financing or mergers. Smaller institutions like Consolidated Bank and HFC, which face significant shortfalls, could particularly benefit from this mechanism to stabilize and grow. Easing the Government’s Debt Burden Kenya’s public debt, exacerbated by borrowing for infrastructure projects and recurrent expenditure, is placing immense strain on the economy. Securitization offers a way to ease this burden by shifting financing for key projects to the private sector. For example: 1. Infrastructure Financing: Instead of relying on government-backed loans, securitization can package future toll road revenues, airport fees, or energy project receivables into securities sold to private investors. 2. Affordable Housing: Mortgage-backed securities (MBS) can attract investments into the housing sector, allowing the government to focus its resources on other pressing priorities. 3. Reducing Guarantees: With securitization, the government can limit the need for direct guarantees on debt, thus mitigating fiscal risks. Diversifying Investment Options Kenya’s investment landscape remains relatively narrow, with limited options for institutional and retail investors. Securitization can change this by introducing new asset classes like: Mortgage-Backed Securities (MBS): Opening avenues for housing finance companies to raise funds while offering investors stable, long-term returns. Asset-Backed Securities (ABS): Allowing businesses to monetize receivables from sectors like agriculture, fintech, and trade, thus spurring economic activity. Infrastructure-Backed Securities: Providing stable, inflation-linked returns, appealing to both local pension funds and international investors. Securitization also aligns well with Kenya’s aspirations to attract more foreign direct investment (FDI). Currently, FDI inflows remain low due to perceived risks and limited diversification opportunities. Asset-backed securities with predictable cash flows and credit enhancements can significantly reduce these barriers, drawing interest from international capital markets. Meeting Genuine Market Demand The Kenyan economy is characterized by a growing need for credit across sectors such as SMEs, agriculture, housing, and renewable energy. Traditional financing methods cannot keep pace with this demand due to structural limitations in the banking sector and fiscal pressures on the government. Securitization can: Expand Credit Supply: By recycling capital, financial institutions can extend more loans to underserved sectors. Lower Borrowing Costs: Investors competing for high-quality securitized assets can drive down interest rates, making credit more affordable. Boost Financial Sector Resilience: A diversified funding base ensures that banks and businesses can withstand economic shocks. Conclusion Securitization is not just an opportunity but a necessity for Kenya. It addresses the urgent liquidity needs of banks, reduces the government’s fiscal pressures, and provides a gateway to broader investment opportunities. With proper regulatory frameworks and awareness campaigns, securitization can unlock Kenya’s economic potential, reshaping the financial landscape while attracting both local and foreign investments. As regulatory deadlines and financial challenges loom, the adoption of securitization could be a decisive step toward a more resilient and vibrant economy. How does Kenya compare to other emerging markets that have Securitized assets? Comparative Table: Obstacles to Securitization in South Africa, India, and the Environment in Kenya Aspect South Africa India Regulatory Framework Unclear and restrictive, including contradictory SARB regulations and accounting standards undermining SPVs' bankruptcy remoteness. No dedicated Clear regulations securitization law; true supporting securitization. sale and bankruptcy Legal clarity enables remote structures lacking. smooth asset transfers Stamp duties up to 10% in and investor confidence. some states Taxation High taxes, including VAT Favorable taxation Double taxation risks; no on servicer fees and stamp regime reduces tax neutrality for SPVs duties on securities transaction costs. Market Liquidity Weak debt market; low Lack of a secondary appetite for long-term market; no market makers exposure Investor Awareness Limited trust in rating agencies; securitization perceived as a tool for struggling companies Historical Issues Robust secondary markets with high liquidity and active market participants. High investor education Poor investor and active participation understanding of from institutional securitization instruments investors. High legal and structuring Stamp duties and high costs, making Cost of structuring costs hinder Transactions securitization unviable for transactions small asset pools Negative perceptions due to past scandals like the Masterbond scandal, discouraging growth Kenya Lower transaction costs due to efficient processes and reduced fees. No significant historical Positive track record in controversies, but limited implementing precedent for complex securitization projects. securitization Minimal, no guarantees No direct government Government like those in the USA (e.g., incentives for Support Ginnie Mae) securitization Analysis of Kenya's Advantage Kenya's conducive securitization environment stems from: Government initiatives encourage market growth and investor trust. 1. Robust Regulation: Clear progressive legal and regulatory frameworks provide certainty for market participants. 2. Efficient Taxation: Favorable tax policies reduce costs, enhancing profitability. 3. Market Development: Active secondary markets and a well-informed investor base support liquidity. 4. Government Incentives: Policies that foster securitization as a financing tool for infrastructure and other sectors. This contrasts with South Africa and India, where regulatory ambiguity, high costs, and market immaturity hinder securitization growth. Comparative Analysis: Market Demand for Securitization in Kenya vs South Africa Securitization relies heavily on market demand from both investors and originators. Kenya and South Africa present stark contrasts in this regard, particularly concerning the role of financial institutions, the need for liquidity, and capital accessibility. Market Demand: Kenya's Advantage In Kenya, market demand for securitization is fueled by: 1. Liquidity Constraints: o Kenyan banks and financial institutions often face liquidity challenges, driven by high demand for credit, limited access to foreign capital, and systemic reliance on short-term deposits to fund long-term loans. o Securitization offers a viable solution, enabling originators (banks, housing finance companies, microfinance institutions) to free up capital by selling loan portfolios to Special Purpose Vehicles (SPVs). This creates room for issuing new loans, ensuring they can meet credit demand. 2. Access to Capital: o Kenyan originators often struggle with obtaining affordable capital from traditional sources, such as bonds or equity markets, due to underdeveloped local capital markets. o Securitization provides a way to tap into institutional investors like pension funds and insurance companies, offering these investors high-quality securities backed by income-generating assets. 3. Growing Investor Appetite: o Kenya’s financial ecosystem has a growing pool of institutional investors who view securitization as a secure and diversified investment option. o High demand for asset-backed securities is bolstered by government initiatives aimed at promoting infrastructure development, housing, and small business financing, all of which align well with securitization. 4. Dynamic Credit Needs: o Kenya’s economy has sectors with untapped potential, such as real estate, agriculture, and fintech lending, which require innovative financing solutions like securitization. Market Demand: South Africa’s Challenges In contrast, South Africa’s securitization market faces sluggish growth in demand due to: 1. Absence of Liquidity Pressures: o South African banks are generally well-capitalized and enjoy robust liquidity, minimizing the necessity of securitization as a funding tool. o Unlike Kenyan banks, South African banks have strong asset bases and easy access to alternative funding sources, such as corporate bonds, foreign capital, and equity markets. o Historically, South African banks have preferred holding assets on their balance sheets, as they view asset size as a measure of strength and stability in a competitive market. 2. Limited Need for Capital Recycling: o Since liquidity constraints are minimal, South African banks do not feel pressured to offload assets to generate capital for new loans. o The well-developed local bond market allows corporates and banks to raise funds directly, reducing reliance on securitization. 3. Lack of Urgency: o South African banks have sufficient internal reserves and favorable lending conditions, meaning there is little need to explore securitization aggressively. o Regulatory and institutional challenges, including high costs and complex compliance requirements, further reduce the incentive for banks to securitize their assets. Key Comparisons Aspect Kenya South Africa Liquidity Banks face significant liquidity Banks are well-capitalized and do not face challenges, making securitization an liquidity shortages, diminishing the need attractive option to free up capital. for securitization. Capital Accessibility Limited access to affordable, longterm capital makes securitization vital for funding growth. Easy access to alternative funding sources like corporate bonds and international capital. Investor Appetite Institutional investors are eager to invest in high-quality securities to diversify their portfolios. Investor confidence is hindered by low trust in rating agencies and perceptions of securitization as a tool for distressed entities. Demand for Credit High demand for credit in underserved sectors creates opportunities for securitization. Moderate demand for securitized products due to a more mature financial market and diverse funding alternatives. Regulatory Support Proactive policies and frameworks encourage securitization as a key tool for economic development. Regulatory uncertainty and historical scandals (e.g., Masterbond) limit market growth. How Kenyan Banks Leverage Securitization 1. Portfolio Churning: o Kenyan originators can use securitization to remove illiquid assets like mortgage and SME loans from their balance sheets. This allows them to raise immediate capital while reducing risk exposure. 2. Access to Broader Markets: o By pooling loans into securities, Kenyan institutions can access a larger pool of investors, including international ones, who are keen to invest in emerging market debt. 3. Funding Infrastructure Development: o Securitization is increasingly being used to fund large-scale projects in Kenya, such as affordable housing and renewable energy, which align with government priorities. South Africa’s Missed Opportunities 1. Reluctance to Securitize: o Banks in South Africa perceive securitization as unnecessary due to their strong balance sheets and lack of liquidity constraints. o Large banks dominate the financial sector and prefer to hold onto assets rather than securitize, given the perception that size equates to stability. 2. Regulatory Barriers: o Complex regulatory requirements and the lack of supportive frameworks have made securitization less appealing compared to traditional funding methods. 3. Market Perceptions: o Historical scandals and a lack of trust in rating agencies have further discouraged investors, resulting in limited demand for asset-backed securities. Kenya’s securitization market thrives on a dynamic interplay of high demand for credit, liquidity challenges, and innovative regulatory support. In contrast, South Africa’s mature financial ecosystem, coupled with strong bank liquidity and readily available capital, creates a less conducive environment for securitization. For South Africa to realize the potential of securitization, it would require a shift in perception, stronger regulatory clarity, and strategic incentives for originators to participate actively in the market. Where can it be applied? 1. Securitization for Microfinance Institutions (MFIs) Description: Microfinance Institutions provide small loans to underserved populations, often without traditional collateral. Securitization helps MFIs access broader funding sources. 1. Asset Pooling: o The MFI identifies a pool of loans with similar characteristics, such as repayment history or borrower demographics. 2. Special Purpose Vehicle (SPV): o The loans are sold to an SPV, a separate legal entity that isolates the risk from the MFI. 3. Issuance of Securities: o The SPV issues securities (e.g., bonds) backed by the cash flows from the pooled loans. 4. Investor Funding: o Investors purchase these securities, providing capital to the SPV, which in turn is used to fund new loans by the MFI. 5. Cash Flow Distribution: o Borrowers' repayments (principal and interest) are collected and distributed to investors through the SPV. Key Considerations: High credit risk requires credit enhancements like guarantees or insurance. Regulatory compliance is critical. I am currently in the process of assessing the Swift ltd Micro Finance Institution who have shown eagerness to raise funds and good promise in terms of their loan portfolio. Illustrative Diagram: MFI (Loan Originator) ↓ Transfers Loans ↓ SPV (Buys Loans & Issues Securities) ↓ Investors (Buys Securities) ↑ Borrower Repayments (Cash Flows) 2. Securitization for Auto Loan Companies (e.g., Watu Credit or Mogo) Description: Auto loan companies issue loans to customers for purchasing vehicles. Securitization allows these companies to monetize their loan books. 1. Asset Pooling: o Auto loans are bundled based on factors like vehicle type, loan term, and creditworthiness. 2. SPV Setup: o The SPV acquires the loan pool and isolates it from the auto loan company’s balance sheet. 3. Tranche Structuring: o Securities are divided into tranches (senior, mezzanine, junior) based on risk and return profiles. 4. Investor Funding: o Investors, such as pension funds or mutual funds, buy these tranches. 5. Repayment Distribution: o Borrowers’ repayments are channeled to the SPV, which distributes them to investors based on tranche hierarchy. Key Considerations: Asset depreciation risk is significant. Prepayment risk may impact cash flow predictability. Watu mainly finance through foreign debt which is expensive and liable to currency risks this offers securitizing their 2 million odd loans an attractive alternative Illustrative Diagram: Auto Loan Company ↓ Sells Loan Pool ↓ SPV (Tranches Loans into Securities) ↓ Investors (Purchase Tranches) ↑ Borrower Repayments (Cash Flows) 3. Securitization of Mobile Money Receivables Description: Mobile money platforms generate receivables from small, frequent transactions. Securitization monetizes these receivables for capital needs. 1. Receivable Pooling: o Aggregates daily or monthly mobile money receivables. 2. SPV Setup: o The SPV acquires the receivables and issues securities. 3. Dynamic Securitization: o Rolling pools may be used to securitize new receivables continually. 4. Investor Subscription: o Investors subscribe to securities with expected cash flows backed by receivables. 5. Payment Flows: o Cash flows from mobile money transactions are directed to the SPV for distribution. Key Considerations: Risks include transaction volume fluctuation and platform performance. Innovative structures like blockchain can enhance transparency. Illustrative Diagram: Mobile Money Operator ↓ Transfers Receivables ↓ SPV (Issues Securities) ↓ Investors (Purchase Securities) ↑ Customer Transactions (Cash Flows) 4. Securitization of Bank Loans Description: Banks securitize loans (e.g., mortgages, personal loans) to free up regulatory capital and diversify risk. 1. Loan Pooling: o Loans are grouped based on credit quality, interest rate, and maturity. 2. SPV Setup: o The SPV buys the loans and removes them from the bank’s balance sheet. 3. Tranche Structuring: o Securities are structured in tranches to cater to different investor appetites. 4. Credit Enhancement: o Mechanisms like over-collateralization or guarantees reduce risk. 5. Investor Funding: o Institutional and retail investors buy the securities. 6. Cash Flow Management: o Loan repayments are funneled to the SPV and allocated to investors. Key Considerations: Credit risk and prepayment risk are central concerns. Compliance with Basel III regulations is vital. Illustrative Diagram: Bank (Loan Originator) ↓ Transfers Loans ↓ SPV (Issues Structured Securities) ↓ Investors (Purchase Securities) ↑ Borrower Repayments (Cash Flows) Commonalities Across Models: 1. SPV: Essential for isolating risk. 2. Tranching: Tailors securities to different risk profiles. 3. Credit Enhancements: Improve investor confidence. 4. Cash Flow Distribution: Ensures transparent allocation of borrower repayments. Conclusion Securitization presents a vital opportunity for Kenya to enhance liquidity, diversify investment options, and attract foreign direct investment while addressing pressing financial challenges. The models outlined in this paper demonstrate how securitization can transform sectors such as microfinance, auto loans, mobile money, and banking by monetizing assets and recycling capital. However, the implementation of securitization comes with potential challenges, including regulatory compliance, credit risks, and market readiness. Solutions to these challenges are addressed in a separate presentation document, which I am prepared to share and present to the team. This supplementary presentation offers detailed strategies to navigate obstacles and optimize securitization’s success in Kenya. With a strategic approach and robust stakeholder collaboration, securitization can unlock Kenya’s economic potential and reshape its financial landscape.