Budgeting

Its purposes

1. Planning

2. Control

3. Coordination

4. Targets

5. Motivation {Through what we can achieve the motivation.}

Formation

Use and monitoring

6. Evaluation

7. Authorization.

Types of Budget:

There are many types.

1. Periodic budget

Show cost and revenue for 1 period of time.

2. Rolling budget

Continuously updating by adding a further accounting period (month and

quarter) when the earliest accounting period has expired.

3. Fixed budget

4. Flexible budget

5. Participating budget (Bottom up)

6. Activity Based budget

7. Zero Based budget

8. Imposed budget (top down)

Other Relevant Definition:

1. Feedback Control

2. Feedforward Control

Feedforward control is a mechanism in a system for preventing problems

before they occur by monitoring performance inputs and reacting to maintain

an identified level.

3. Decentralization

A decentralized organizational structure is one in which senior management

has shifted the authority for some types of decision making to lower levels in

the organization

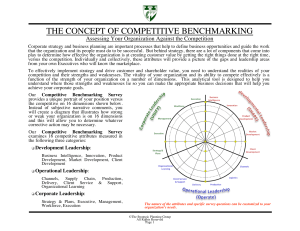

4. Benchmarking

It is a standard setting.

Benchmarking is the process of comparing your own organization, its

operations or processes against other organizations in your industry or

in the broader marketplace. Benchmarking can be applied against any

product, process, function or approach in business. Common focal

points for benchmarking initiatives include measures of time, quality,

cost and effectiveness, and customer satisfaction.

The intent of benchmarking is to compare your own operations to that

of competitors and to generate ideas for improving processes,

approaches, and technologies to reduce costs, increase profits and

strengthen customer loyalty and satisfaction. Benchmarking is an

important component of continuous improvement and

quality initiatives, including Six Sigma.

The case for benchmarking suggests that a particular process in your

firm can be strengthened. Some organizations benchmark as a means

to improve discrete areas of their business and monitor competitors'

shifting strategies and approaches. Regardless of the motivation,

cultivating an external view of your industry and competitors is a

valuable part of effective management practices in a world that is

constantly changing.

There are a number of core drivers of benchmarking initiatives in a

firm:

The most common driver for benchmarking comes from the

internal perspective that a process or approach can be improved.

Organizations will collect data on their own performance at

different points in time and under different circumstances, and

identify gaps or areas for strengthening.

Many organizations compare themselves to competitors in an

attempt to identify and eliminate gaps in service or product

delivery or to gain a competitive edge. The data gathered in a

competitive benchmarking initiative offers specific insights into

a competitor's processes and thinking.

The term "strategic benchmarking" is used to describe when a

firm is interested in comparing its performance to the best-inclass or what is deemed as world-class performance. This

process often involves looking beyond the firm's core industry

to firms that are known for their success with a particular

function or process.

Difference of Benchmarking and Reverse

Engineering:

Benchmarking involves the usage of information gathered from

world class companies in order to improve your company's

performance. Reverse engineering is the study of an actual

product by disassembling it to determine how it was created.

TYPES OF BENCHMARKING:

Internal benchmarking.

Competitive benchmarking.

Functional benchmarking.

Strategic benchmarking.

5. Balance Scorecard.

Financial Matters Iss mai har chez par is tahan faisla karna hai ka

shareholders ko faida ho.

Cashflow and gearing

Sales growth

Increase in market share.

Learning and Growth Hum is mai is tarhan dekhta hai ka hum kis

tarhan improve kar sakta hai----- Abilities, skills wagera ko.

Employees satisfaction/ retention/ productivity

Customers

Obviously, customer ko faida dena hai

Internal business process

What business process must we excel.

Efficiency

Unit cost

New product

Manufacturing process

Cycle time

6. Non-Financial performance indicator

Competiveness

Activity level

Quality of services [new accounts gain and loss, rejections in

manufacturing, repeat customers order]

Productivity

Customer satisfaction

Quality of staff experience [Staff turnover rate, days absence, job

satisfaction, training programs]

Innovation.

7. Beyond budgeting.

Beyond Budgeting is the idea of abolishing traditional budgeting processes to

eventually improve management control over an organization. By abandoning

traditional budgeting processes, a company aims to establish a highly

decentralized organizational system and adaptive set of management

processes

Pros

Faster response

Innovative strategies

Lower costs

More loyal customers

Cons

Major shift in how a company is managed.

Time Required.

Gaming the System.

Blame for Outcomes.

Expense Allocations.

Spend It or Lose It.

Only Considers Financial Outcomes.

Strategic Rigidity.

Related Courses.

8. Financial performance indicator

Profitability

Liquidity

Asset turnover ratios

9. Performance evaluation in service industry