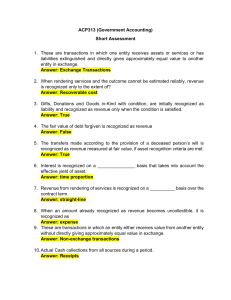

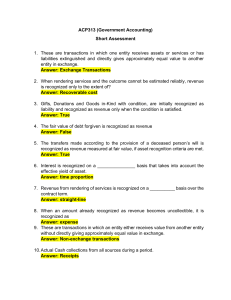

Lexine Dara Comia BSA – 1A ACCOUNTING • • It is an information system that reports the condition of a business to the intended users. It provides financial information and makes General Purpose Financial Reports that helps in decision making. Basic Accounting Activities IDENTIFYING RECORDING COMMUNICATING Identifying transactions in an entity. Recording events which includes classifying and summarizing of information. It can be done by analyzing and interpreting the reported information. Functions of Accounting People Make decisions Communicate through financial statements Company Activities measured Accountant Branches of Accounting FINANCIAL MANAGERIAL NON-PROFIT Reporting business activities to the external users. Assists internal users in making wellinformed business decision. Accounting made for humanitarian purposes. Classical Notion of Stewardship • • Managers are accountable to the stakeholders for the safe keeping of the company’s resources. Stewards must think about what is best for the business. Users of Accounting Information External User Internal User People like investors and lenders who use financial statements for their personal gain. Managers and people who run the company. They aim to use their knowledge to improve the efficiency of the company. Basic Accounting Concepts and Principles • Financial transactions must have equal and opposite effects in at least two different accounts. • Integrity • • • • Objectivity Professional Competence and Due Care Confidentiality Professional Behaviour Forms of Business Organization as Nature of Operations Service Business Offers services to people Merchandising Business Buying and selling of goods Manufacturing Business Manufacturing goods out of raw materials Agricultural Business Planting and selling of goods Hybrid Business More than one type of activity Forms of Business Organization PROPRIETORSHIP • • One owner Unlimited liability for unpaid debts PARTNERSHIP CORPORATION • • • • Two or more owners Unlimited liability for unpaid debts Unlimited owners Limited liability for corporate debts COOPERATIVE • • One man vote Operates like corporation Operating Cycle CASH SUPPLIES, STAFF PAYROLL (RENDER SERVICE) ACCOUNTS RECEIVABLE CASH ACCOUNTS RECEIVABLE INVENTORY CASH ACCOUNTS RECEIVABLE RAW MATERIALS, DIRECT LABOR FINISHED GOODS INVENTORY CASH ACCOUNTS RECEIVABLE RAW MATERIALS, DIRECT LABOR BIOLOGICAL ASSETS INVENTORY Fundamental Business Activities (inter-related) FINANCING ACTIVITIES INVESTING ACTIVITIES OPERATING ACTIVITIES More on investing or gathering of capital Purchase of long-term assets Activities of a company resulting in the sales of products or services Underlying Assumptions in Accounting Accrual Basis Records transactions as it happens, not as when cash is received. Going Concern Assumes the entity will continue until the next period. Economic Entity Personal expense should be separated from the business activities. Monetary Unit Measure the items in the financial statements in peso. Periodicity Life of an entity is divided into periods. Qualitative Characteristics of Financial Statements • • • Has predictive or confirmatory value Capable of making a difference to the user’s decision making Information is consistent and uniform • Independent observers could reach consensus. • It must be complete, neutral, and free from error. Faithfully represent the substance of what it purports to represent. Having information Can be easily available on time. understood by anyone. The benefit must excess the cost