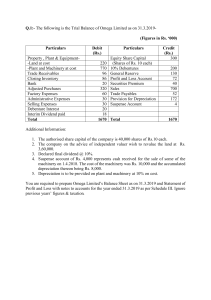

NEW NATION SCHOOL DEPARTMENT OF ACCOUNTING FUNDAMENTALS OF ACCOUNTING METHODS 2021/2022 ACADEMIC YEAR WORKSHEET 4 (DEPRECIATION) Q1. The data below was extracted from the books of Karana Enterprise: Non-Current Assets Machine No. 1 Machine No. 2 Machine No. 3 Machine No. 4 Cost GH₵ 200,000 350,000 400,000 540,000 Date of purchase 01/01/13 30/06/13 01/01/14 01/12/14 Date of disposal 01/10/15 30/06/15 Additional information: i. ii. iii. iv. It is the policy of the company to charge a full year’s depreciation on all machinery assets in use by the end of the financial year. Machine 1 and 3 are depreciated at 20% on reducing balance while machine 2 and 4 are 10% on straight line basis. Accounts are prepared to December 31st each year. Machine 1 and 2 were sold for GH₵150,000 and GH₵250,000 respectively. You are required to: i. Show the relevant entries to record these transactions for the relevant years. Q2. The following information relates to Kpakpakpa Ltd: a) On 1st January, 2015 balances brought forward in respect of non-current assets were: GH₵ Plant and machinery at cost 900,000 Motor vehicles at cost 780,000 Provision for depreciation: Plant and machinery 50,000 Motor vehicles 30,000 b) During the six months period ending 30th June 2015, the following additional non-current assets were acquired by cheque: BEKOE, ASARE, DONKOR & APPIAGYEI 1 OF 2 i. ii. On 31st March 2015 two cargo GH₵20,000 each and a plant for GH₵50,000 On 1st April 2015, one saloon car at GH₵10,000 and four machines GH₵12,000 each. On 30th June, 2015 two machines purchased on 1st January, 2012 at GH₵9,000 were sold for GH₵4,500 and GH₵5,500. On the same date, one saloon car purchased on 1st July, 2012 for GH₵15,000 was auctioned for GH₵11,000. It is the policy of the business to depreciate motor vehicles and plant and machinery at 10% and 5% per annum respectively on straight line method and on one month ownership basis. You are required to write up the following accounts to 30th June, 2015: i. ii. iii. Plant and machinery and Motor vehicles. Provision for depreciation of plant and machinery and motor vehicles Disposal of plant and machinery and motor vehicles. Q3. An extract from the statement of financial position of Nana Yaw Ltd. as at 31st December 2014 is given below: Asset Plant and Machinery Cost GH₵’000 200,000 Net Book Value GH₵’000 125,583 Additional information: It is the policy of the business to provide for depreciation at the rate of 10% per annum on reducing balance basis. Annual depreciation is calculated on asset in use at the end of the year. The following transactions took place in 2015: i. ii. Plant which cost GH₵35,000,000 and had been used for four years was sold for GH₵24,000,000. A new plant costing GH₵40,000,000 was acquired on 1st January, 2015. You are required to prepare: a) Plant and machinery account. b) Provision for depreciation account for the year ended 31st December, 2014 and 2015 c) Plant and machinery disposal account. BEKOE, ASARE, DONKOR & APPIAGYEI 2 OF 2