Financial Statement Adjustments: Accruals, Prepayments, Depreciation

advertisement

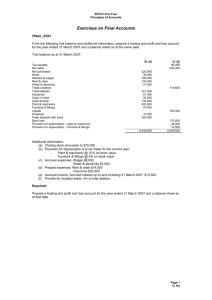

Financial statements The financial statements which have been covered so far have shown that total sales minus total expenses for the period will result in the net profit (or a net loss) for the period. Up to this level it is assumed that the expenses and income are incurred (recognised) exactly in the financial period under review. E.g. if statement of profit or loss is drafted up, all the expenses shown in the trial balance are exactly for that period only, there will be no accruals or prepayments. These types of financial statements are much easy to prepare. Adjustments When financial statements are prepared incorporating adjustments they become much comprehensive as calculations will have to be done to get the amounts which have to be posted to each set of financial statement. This will involve the following adjustments: 1. Accruals; 2. Prepayments; 3. Depreciation, and 4. Provision for bad debts. Accruals Accruals mean expense or income incurred but has not yet been paid. This can be applicable to income and expenses, let us see how it will be applied. Accrued expenses This will be defined as: amount of expenses that have been used by the organisation but have not yet been paid until the end of the financial period. (Example) Water &Electricity: Let us assume the total amount for water and electricity for the whole year is N$ 10 000, total amount paid for is only N$ 8000. In this case it means that there is a difference; as the amount paid for that expenses is only N$ 8000. The result will mean that: Total amount paid Total amount incurred Difference = Accrued expenses N$8 000 N$10 000 N$2 000 In other word the business paid less than what they were supposed to have paid for water & electricity. The effect of accrual on the financial statements The effect will be that the accrued amount of N$2 000 will be added to the amount of water and electricity in the statement of profit or loss and the same amount will be recoded as a liability in the statement of financial position, this is because the amount have not yet been paid. Statements of profit or loss and other comprehensive income for the year ended........ Less: operating expenses Water & electricity (8000 + 2000) N$ 10 000 Statements of financial position as at................ Current liabilities Accrued expenses N$ 2000 The double entry for accrued expense The reason why the accrued amount is added to the amount already paid in the statement of profit or loss is not a formula, but is an entry that is done by DR one account and CR another account. The entry will be as follow: DR. Water & Electricity expenses CR. Accrued expenses account Accrued income This will be defined as: Income that the business is entitled to but have not yet received the money until end of the financial year. (Example) Interest received: Let’s assume that the total amount which the business supposed to get for interest received on an investment for the whole year is N$3 500. What was received for that period is only N$2 000. In this case this means that there is a difference as the amount received for the income is only N$2 000. The result will mean: Total amount received Total amount incurred Difference = Accrued income N$2 000 N$3 500 N$1 500 In other word, this is basically saying that the organisation received less than what it was supposed to have received. The effect on the financial statements The effect will be that, the accrued amount of N$1 500 will be added to the amount of interest received in the statement of profit or loss and classified as an asset in the statement of financial position. Statements of profit or loss for the year ended........ Add: other income Interest received (2000 + 1500) N$3 500 Statements of financial position as at................ Currents assets Accrued income N$ 1500 The double entry for accrued income The reason why the accrued amount is added to the amount already paid in the statement of profit or loss is not a formula, but is an entry that is done by DR one account and CR another account. The entry is as follow: DR. Accrued income CR. Interest received account Prepayments Prepayment means is expenses or income that is paid in advance. This can be applicable to both income and expenses, let us see how it will be applied. Prepaid expenses This will be defined as: amount of an expense that have been paid in advance by the organisation, but has not yet been incurred during the financial period under review. (Example) Rent expenses: Let us assume the total amount for rent for the whole year is N$6 500. The total amount paid for that is N$7 000. In this case it means that there is a difference as the amount paid for the expense is N$7 000. The result will mean: Total amount paid Total amount incurred Difference = Prepaid expenses N$7 000 N$6 500 N$500 In other word this is basically saying that the organisation paid more than what it was supposed to have paid. Effect on the financial statements The effect will be that the prepaid amount of N$500 will be deducted from the amount of rent paid in the statement of profit or loss and classified as an asset in the statement of financial position as follows: Statements of profit or loss for the year ended........ Less: operating expenses Rent expenses (7000 - 500) N$ 6500 Statements of financial position as at................ Current Assets Prepaid expenses N$ 500 The double entry for prepaid expense The reason why the prepaid amount is deducted to the amount already paid in the statement of profit or loss is not a formula, but is an entry that is done by DR one account and CR another account. The entry will be as follow: DR. Prepaid expenses CR. Rent expenses account Prepaid income This is defined as: an amount of income that has been received in advance by the organisation, but has not yet been incurred until year end. (Example) Commission received: Let us assume that the total amount for commission for the whole year is N$1 200. The total amount received up-to-date is N$1 400. In this case it means that there is a difference as the amount received for that income is only N$ 1400. The result will mean: Total amount received Total amount incurred Difference = Prepaid income N$1 400 N$1 200 N$200 In other word, this is basically saying that the organisation received more than what it was supposed to have received. The effects on the financial statements The effects will be: the prepaid amount of N$200 will be deducted from the amount of commission received in the statement of comprehensive income and will be classified as a liability in the statement of financial position as follow: Statements of profit or loss for the year ended........ Add: Other income Commission received (1400 - 200) N$ 1200 Statements of financial position as at................ Current liabilities Prepaid income N$ 200 The double entry for prepaid income The reason why the prepaid amount is deducted to the amount already paid in the statement of comprehensive income is not a formula, but is an entry that is done by DR one account and CR another account. The entry will be as follow: DR. Commission received CR. Prepaid income Depreciation Depreciation is part of year end adjustment, is defined as follows: Decrease in value of assets due to wear and tear, decay and decline in price. Depreciation affects non -current assets to the extent that some non- current assets own by business need to be depreciated. E.G Motor van, equipment, computers and so on. Depreciation is regarded as an expense in the accounting records of an organisation. Method of calculating depreciation There are two common methods that can be used to calculate depreciation, they are: Straight line method and Reducing balance method (Diminishing balance method). Straight line method Sometimes also called the fixed instalment method, the number of years used is estimated. The cost, less the estimated disposal value, is then divided by the number of years to give the depreciation charge each year. This means that depreciation charged will be constant each year. Formula Cost – Residual value Number of years = Depreciation or Cost price X Rate% = Depreciation Reducing balance method By this method a fixed percentage of depreciation is deducted from the cost price in the first year. In the second or later years the same percentage is taken of the reduced balance (cost less total depreciation already charged). Depreciation charged each year decrease from one year to another. Formula Cost – Accumulated depreciation = NBV X Rate% The double entry Whether the straight line method or reducing balance method is used the double entry for recording depreciation is the same, this will be shown as follow: DR. Depreciation CR. Accumulated depreciation Provision for bad debts/ doubtful debts Provision for bad debts is an estimate that is made for the value of debtors who are unlikely not be able to pay. This is not the same as bad debts because a bad debt is the actual amount that is known that is not going to be paid. Provision for bad debts is calculated every year to determine the amount of debtors that are probably not going to pay using a fixed percentage on the outstanding debtors. This will then be compared between last year provision and this year provision and then the difference will either be increase or decrease in provision for bad debts. An increase in provision for bad debts is an expense while a decrease in provision for bad debts is an income. Prudence concept apply to provision for bad debts. The Double entry The double entry for provision for bad debts will be as follows: Increase in provision for bad debts DR. Bad debts CR. Provision for bad debts Decrease in provision for bad debts DR. Provision for bad debts CR. Bad debts Effect on financial statements An increase in provision for bad debts is recorded in operating expenses and the amount calculated will be shown in the statement of financial position being deducted from accounts receivable. Example: Increase in provision Debtors balance as at year end N$10 000 Provision for bad debts for previous year N$800 Policy: Provision for bad debts is calculated on the outstanding debtor’s amount at 10%. Answer: 10% X 10 000 = N$1 000 provision for this year. Provision for last year minus provision for this year. N$1 000 –N$800= N$200 increase in provision Statement of profit or loss for the year ended................ Less: Operating expenses Increase in provision for bad debts N$ 200 Statement of financial position as at ....................... Current assets Accounts receivable N$ 10 000 Less: Provision for bad debts (N 1 000) N$9 000 Example: Decrease in provision Debtors balance as at year end N$8 000 Provision for bad debts for previous year N$900 Policy: Provision for bad debts is calculated on the outstanding debtor’s amount at 10%. Answer: 10% X 8 000 = N$800 provision for this year Provision for last year minus provision for this year. N$900 –N$800 = N$100 decrease in provision Statement of profit or loss for the year ended................ Add: Other income Decrease in provision for bad debts N$ 100 Statement of financial position as at ....................... Current assets Accounts receivable N$8 000 Less: Provision for bad debts (N$800) N$7 200 The accounting concept The underlying accounting concept which apply to year-end adjustment is Accruals basis (matching rule). Which state that revenue and costs should be recognised in the period in which they are incurred regardless of whether cash or cash equivalent is received or paid. Source: Wood, F and Sangster, A. 2005. Business Accounting (10th e.d). China: Pearson Education Limited. END