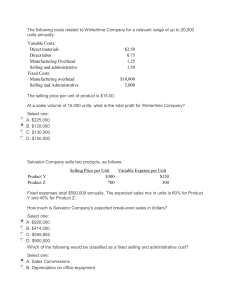

Costing Break-even Analysis Objectives • Analyze the concepts under break-even • Compute the break-even point in unit sales and sales dollars • Determine the level of sales needed to achieve a desired target profit. • Prepare and interpret a cost-volume-profit (CVP) graph. • Compute the margin of safety and explain its significance • Analyze the ‘make or buy’ decisions of the firm Break-even Analysis • This is the assessment of the interrelationship that exists among costs, volume and profits at different levels of output. • It is an important tool for management • It assists in planning and making important decisions Break-even Assumptions • Costs are classified as either variable or fixed • Selling price remains constant • Volume is the only factor that affects costs and revenue • The factors of production are constant • The focus is on a particular product or product mix. Uses of BEA • Determine the profit and loss at different levels of production and sales • Make predictions on the effects of price changes on sales • Determine the break-even point • Determine the margin of safety • Examine the relationship between fixed and variable costs • Determine how changes in costs and efficiency will affect profits Review the Advantages and Disadvantages of BEA BE Point • The level of output that enables a firm to cover its costs (both fixed and variable) exactly. It is the point where neither a profit or loss is being made. • The break-even point is either the point where total sales revenue equals total expenses, variable and fixed • It is the point where total contribution margin equals total fixed expenses. • Once the break-even point has been reached, net income will increase by the unit contribution margin for each additional unit sold. Calculation of BE Point • There are three methods which can be used to determine the BE point of a firm. These are: • The Equation Method • The Contribution Margin Method • The Graphical Method We will focus specifically on the CM and Graphical Methods Contribution Margin Method BE Point, Target Profit, Margin of Safety BE Point •𝐵𝐸 𝑖𝑛 •𝐵𝐸 𝑖𝑛 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠 𝑢𝑛𝑖𝑡𝑠 = 𝐶𝑀 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠 𝑠𝑎𝑙𝑒𝑠 $ = 𝐶𝑀 𝑅𝑎𝑡𝑖𝑜 * 𝐶𝑀 𝑅𝑎𝑡𝑖𝑜 = 𝐶𝑀 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 𝑆𝑒𝑙𝑙𝑖𝑛𝑔 𝑃𝑟𝑖𝑐𝑒 × 100 Target Profit • 𝑇𝑃 𝑖𝑛 𝑢𝑛𝑖𝑡𝑠 = 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠+𝑇𝑎𝑟𝑔𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡 𝐶𝑀 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 • TP 𝑖𝑛 𝑠𝑎𝑙𝑒𝑠 $ = 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠+𝑇𝑎𝑟𝑔𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡 𝐶𝑀 𝑅𝑎𝑡𝑖𝑜 Margin of Safety The margin of safety is defined as the excess of budgeted (or actual) sales over the breakeven volume of sales. It is the amount by which sales can decrease before the firm begins to incur losses. $𝑀𝑆 = 𝑇𝑜𝑡𝑎𝑙 𝑆𝑎𝑙𝑒𝑠 − 𝐵𝑟𝑒𝑎𝑘 𝑒𝑣𝑒𝑛 𝑠𝑎𝑙𝑒𝑠 %𝑀𝑆 = 𝑇𝑆 − 𝐵𝐸𝑆 × 100 𝑇𝑆 The margin of safety percentage indicates the percentage by which total sales may decline, other things being constant, before the firm begins to incur losses. Example 1 Racing developed contribution margin income statement at 300 units. We will use this information to calculate the BE Point in units and sales dollars. Income 300 units Sales $ 150,000 Less: variable expenses 90,000 Contribution margin $ 60,000 Less: fixed expenses 80,000 Net operating income $ (20,000) Calculating the BE Point • BE in Units 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠 𝐵𝐸 𝑖𝑛 𝑢𝑛𝑖𝑡𝑠 = 𝐶𝑀 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 FC- $80,000 CM/UNIT=$60,000/300 =$200 80,000 𝐵𝐸 𝑖𝑛 𝑢𝑛𝑖𝑡𝑠 = 200 =400 Units BE in Sales Dollars 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠 𝐵𝐸 𝑖𝑛 𝑠𝑎𝑙𝑒𝑠 $ = 𝐶𝑀 𝑅𝑎𝑡𝑖𝑜 FC= $80,000 CM/UNIT = $200 SP/UNIT= $150,000/300 =$500 CM RATIO=200/500*100 =40% 80000 𝐵𝐸 𝑖𝑛 𝑠𝑎𝑙𝑒𝑠 $ = 40%𝑂𝑅 0.4 =$200,000 Target Profit (Assume the firms has a target profit of $50,000) • 𝑇𝑃 𝑖𝑛 𝑢𝑛𝑖𝑡𝑠 = 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠+𝑇𝑎𝑟𝑔𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡 𝐶𝑀 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠+𝑇𝑎𝑟𝑔𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡 𝐶𝑀 𝑅𝑎𝑡𝑖𝑜 TP 𝑖𝑛 𝑠𝑎𝑙𝑒𝑠 $ = FC = $80,000 FC= $80, 000 TP = $50,000 TP= $50,000 CM/UNIT= $200 CM RATIO = 40% OR 0.4 (80,000 + 50,000) ∴ 𝑇𝑃 𝑖𝑛 𝑢𝑛𝑖𝑡𝑠 = 200 = 650 units ∴TP 𝑖𝑛 𝑠𝑎𝑙𝑒𝑠 $ = (80,000+50000) 40% = $325,000 Margin of Safety • $𝑀𝑆 = 𝑇𝑜𝑡𝑎𝑙 𝑆𝑎𝑙𝑒𝑠 − 𝐵𝑟𝑒𝑎𝑘 𝑒𝑣𝑒𝑛 𝑠𝑎𝑙𝑒𝑠 TS = $150,000 BES= $200,000 $𝑀𝑆 = 150,000 −200,000 =($50,000) • %𝑀𝑆 = 𝑇𝑆−𝐵𝐸𝑆 𝑇𝑆 TS=$150,000 BES= $200,000 × 100 150,000 − 200,000 %𝑀𝑆 = × 100 150,000 = -33.33% Activity 1 • Using Chapter from Pitterson pg 221 • Complete exercise “Black’s Block Factory” Graphical Method The relationship among revenue, cost, profit and volume can be expressed graphically by preparing a CVP graph. The graphical method gives us a concise picture of the cost-volume profit relationship of the business. User-friendly information on sales, fixed costs, variable costs, total costs and the profits at various levels of sales can be obtained. BE Chart • From the chart the following information can be derived: 1) Total revenue/ sales vary directly with the number of units sold 2) Fixed costs are constant within the relevant range 3) Variable costs are represented by the area above the FC and below the total cost. They vary with output. BE Chart 4) Break-even occurs at the point of intersection between the TR line and the TC line. Any particular level of activity to the right of the break-even point would result in a profit which represents the vertical distance between the TR line and the TC line. Any particular activity to the left of the break-even point would result in a loss which is represented by the vertical distance between the TC line and the TR line. 5) At break-even point. TR equals TC and profit is zero. Note In a CVP graph, • unit volume is usually represented on the horizontal (X) axis • dollars on the vertical (Y) axis. BE Graph 450,000 400,000 350,000 300,000 250,000 200,000 150,000 100,000 50,000 - 100 200 300 Units 400 500 600 700 800 BE Chart • Racing developed contribution margin income statements at 300, 400, and 500 units sold. We will use this information to prepare the BE graph. Income 300 units Sales $ 150,000 Less: variable expenses 90,000 Contribution margin $ 60,000 Less: fixed expenses 80,000 Net operating income $ (20,000) Income 400 units $ 200,000 120,000 $ 80,000 80,000 $ - Income 500 units $ 250,000 150,000 $ 100,000 80,000 $ 20,000 BE Chart 450,000 400,000 350,000 In a CVP graph, unit volume is usually represented on the horizontal (X) axis and dollars on the vertical (Y) axis. 300,000 250,000 200,000 150,000 100,000 50,000 - 100 200 300 400 Units 500 600 700 800 BE Graph 450,000 400,000 350,000 300,000 250,000 200,000 Fixed Expenses 150,000 100,000 50,000 - 100 200 300 Units 400 500 600 700 800 BE Graph 450,000 400,000 350,000 300,000 250,000 Total Expenses (F+V) 200,000 Fixed Expenses 150,000 100,000 50,000 - 100 200 300 Units 400 500 600 700 800 BE Graph 450,000 400,000 Total Sales 350,000 300,000 Total Expenses 250,000 200,000 Fixed Expenses 150,000 100,000 50,000 - 100 200 300 Units 400 500 600 700 800 BE Graph 450,000 Break-even point (400 units or $200,000 in sales) 400,000 350,000 300,000 250,000 200,000 150,000 100,000 50,000 - 100 200 300 Units 400 500 600 700 800 Activity 2 Firm A makes and sells pillows. Each pair of pillows is sold for $500. The variable cost per unit of pillow is $200 and it has total fixed costs of $45 000. The total units sold were 200. 1. Use the above information to plot a well-labelled breakeven chart 2. Determine the margin of safety and illustrate this on your chart. Make or Buy Decisions Make or Buy • A very important decision a firm must make is whether to make a product or buy it. Whether the firm makes the product or buys it depends on the firm’s cost-benefit analysis. Benefits must be greater than cost. Making Products • The following are some reasons why a firm will want to make its own products: • To maintain its quality. The reputation of the firm is at stake • Costs will be lower. Outsourcing can be more costly • The firm has spare capacity. If plant equipment are being underutilised then the firm can benefit from capacity utilisation. • There are no suitable suppliers. In this situation the firm must produce the product itself • The size of the order. It may not be cost-effective for another firm to accept this order Making Products Cont’d • Delivery times. The outside supplier may not be able to deliver the supplies on time • To maintain secrecy. In a highly competitive market it is vital that the firm keeps its operations secret • To ensure a ready supply of output. This is necessary to ensure customer loyalty and maintain market share. • To give workers employment. This is vital if workers have been with the firm for long periods and it will be a cost factor to lay off workers and then have to retrain new staff when needed. Outsourcing • The following are the factors that will lead a firm to outsource supplies: • The lack of spare capacity: if the firm is operating at full capacity. • The cost factor: it is more cost-effective to buy the product than make it. • The lack of technical skill to make the product: it would not be cost-effective to hire the technical skills. • To increase specialisation: if the product needed is not in keeping with the firm’s line of operation, it is prudent to outsource the product. This allows the firm to specialise in its line of output • The credibility of the outside firm: if the firm can depend on the efficiency as well as the quality of the output of the outside firm. Example AG’s Ltd manufactures stereos to be used in the production of cars. The costs associated with its current production of 30,000 stereos are outlined below: • DM $515,000 • DL $685,000 • DE $200,000 • VOH $100,000 • FOH $1,000,000 The firm can purchase the stereos from Stereo Plus at $75 per stereo. Should the company make or buy the stereos? Notes • The variable costs of production should be considered when making this decision. • Fixed costs are incurred whether the firm continues production or chooses to purchase the stereos. (This therefore can not impact on the decision to be made.) 1st Calculate the total cost of making the products. 2nd Calculate the total cost of purchasing the products. 3rd Compare the costs to determine which course of action should be taken by the firm. A manufacturing company is deciding whether to buy in a component from an outside supplier or to produce the part itself. Buying it from an outside supplier will cost $90 per unit. The company accountant has produced a list of costs. Total Cost Cost Per Unit Direct costs Materials 20,000 40 Labour 12,000 24 Variable 3,000 6 Fixed 8,000 16 General Overheads 6,000 12 Total cost 49,000 98 Overheads Exercise Only 50% of the fixed manufacturing overhead cost is related to this specific component. The general overheads will be incurred regardless of the decision made. Calculate the relevant cost of making the component. What decision should the company make based on these cost calculations: should it make or buy?