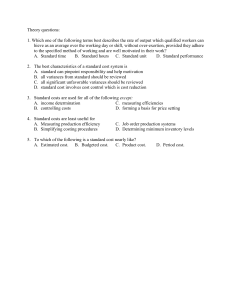

ACCOUNTING L1 STANDARD COSTING 1 RAGHAV WADHWA ❏ MCOM, MBA, B.ED, UGC NET ❏ PRODUCED NUMEROUS AIRs ❏ PLUS VERIFIED EDUCATOR ❏ Awarded a certificate from IIT, Bombay (under NPTEL) 2 Join with us in Telegram For Homework and class Notes click on: Telegram Channel ● https://t.me/raghavwadhwa 3 Study Planner Personal Guidance Customized study plan with bi-weekly reviews Get one on one guidance from top exam experts Live Classes ICONIC Weekly Tests PLUS Structured Courses Unlimited Access Test Analysis Study Material Get one on one guidance from top exam experts Specialised Notes & Practice Sets Experts' Guidelines Study booster workshops by exam experts 4 RAGHAVJRF RAGHAVJRF 5 6 ACCOUNTING STANDARD COSTING 7 MATERIAL VARIANCES SR × SQ SR × SM MYV SR × AQ MMV AR × AQ MPV MUV MCV SR = Standard Rate SQ = Standard Quantity (for Actual Production) SM = Standard Mix (Total of AQ but in the ratio of SQ) AQ = Actual Quantity Consumed (for Actual Production) AR = Actual Rate NOTE: SR, AQ, and AR are always given. These can be need to compute SQ and SM. SQ is computed only when actual output is given. 8 MATERIAL VARIANCES The standard material required for production is 5,200 kg. A price of ₹ 2 per kg has been xed for the materials. The actual quantity of materials used for the product is 5,600 kg. A sum of ₹ 14,000 has been paid for the materials. Calculate: (a) MCV; (b) MPV; (c) MUV. 9 fi Q1 MATERIAL VARIANCES Sol The standard material required for production is 5,200 kg. A price of ₹ 2 per kg has been xed for the materials. The actual quantity of materials used for the product is 5,600 kg. A sum of ₹ 14,000 has been paid for the materials. Calculate: (a) MCV; (b) MPV; (c) MUV. AR = 14,000/5000 = ₹ 2.50 per kg. SR × SQ 2 × 5,200 10,400 SR × SM INACTIVE FIELD SR × AQ 2 × 5,600 11,200 AR × AQ 2.5 × 5,600 14,000 MUV = (SR × SQ) - (SR × AQ) = 10,400 - 11,200 = 800 (A) MPV = (SR × AQ) - (AR × AQ) = 11,200 - 14,000 = 2,800 (A) MCV = (SR × SQ) - (AR × AQ) = 10,400 - 14,000 = 3,600 (A) 10 fi Q1 MATERIAL VARIANCES Q2 A manufacturer requires 10 kg standard material to manufacture one unit of product ‘X’. The standard price per kg of material is ₹ 5. The accounting records, however, reveal that 25,000 kg of material costing ₹ 1,50,000 were used for manufacturing 2,000 units. Calculate the material variances. 11 MATERIAL VARIANCES Q2 Sol A manufacturer requires 10 kg standard material to manufacture one unit of product ‘X’. The standard price per kg of material is ₹ 5. The accounting records, however, reveal that 25,000 kg of material costing ₹ 1,50,000 were used for manufacturing 2,000 units. Calculate the material variances. Standard Quantity (SQ) for 2,000 units = 2,000 units × 10 kg = 20,000 kg AR = 1,50,000/25,000 = ₹ 6 per kg SR × SQ 5 × 20,000 1,00,000 MUV = (SR × SQ) - (SR × AQ) = 1,00,000 - 1,50,000 = 50,000 (A) MPV = (SR × AQ) - (AR × AQ) = 1,25,000 - 1,50,000 = 25,000 (A) MCV = (SR × SQ) - (AR × AQ) = 1,00,000 - 1,50,000 = 25,000 (A) SR × SM INACTIVE FIELD SR × AQ 5 × 25,000 1,25,000 AR × AQ 6 × 25,000 1,50,000 12 MATERIAL VARIANCES Q3 Material A B C Standard Quantity (kg) 10 15 25 50 Standard Price (₹) 5 2 3 Actual Quantity (kg) 10 10 30 50 Actual Price (₹) 6 2 5 Find out Material Mix Variances. Sol Materials A B C SR × SQ 5 × 10 = 50 2 × 15 = 30 3 × 25 = 75 SR × SM 5 × 10 = 50 2 × 15 = 30 3 × 25 = 75 SR × AQ 5 × 10 = 50 2 × 10 = 20 3 × 30 = 90 AR × AQ 6 × 10 = 60 2 × 10 = 20 5 × 30 = 150 Total 155 155 160 230 MYV = (SR × SQ) - (SR × SM) = MMV = (SR × SM) - (SR × AQ) = 155 - 160 = 5(A) MUV = (SR × SQ) - (SR × AQ) = MPV = (SR × AQ) - (AR × AQ) = MCV = (SR × SQ) - (AR × AQ) = 13 MATERIAL VARIANCES Q4 Standard Material X Y Quantity 200 100 300 Actual Price (₹) 2 5 Amount (₹) 400 500 900 Quantity 240 120 360 Price (₹) 2.20 4.50 Amount (₹) 528 540 1,068 Find out Material Variances. Sol Materials Y SR × SQ 2 × 200 = 400 5 × 100 = 500 SR × SM 2 × 240 = 480 5 × 120 = 600 SR × AQ 2 × 240 = 480 5 × 120 = 600 AR × AQ 2.20 × 240 = 528 4.50 × 120 = 540 Total 900 1,080 1,080 1,068 X MYV = (SR × SQ) - (SR × SM) = 900 - 1,080 = 180(A) MMV = (SR × SM) - (SR × AQ) = 1,080 - 1,080 = NIL MUV = (SR × SQ) - (SR × AQ) = 900 - 1,080 = 180(A) MPV = (SR × AQ) - (AR × AQ) = 1,080 - 1,068 = 12(F) MCV = (SR × SQ) - (AR × AQ) = 900 - 1,068 = 168(A) 14 MATERIAL VARIANCES Q5 Sol Material A B C Standard Quantity (kg) Standard Price (₹) Total Amount (₹) 60 6 360 40 5 200 20 7 140 120 700 Due to shortage of material A it was decided to reduced consumption of A by 10% and to increase that of B by 10%. The actual quantities used were - A = 40 kg; B = 50 kg and C = 24 kg. Materials A B C SR × SQ 6 × 54 = 324 5 × 44 = 220 7 × 20 = 140 SR × SM 6 × 52.2 = 313.20 5 × 42.5 = 212.50 7 × 19.3 = 135.10 SR × AQ 6 × 40 = 240 5 × 50 = 250 7 × 24 = 168 AR × AQ 6 × 40 = 240 5 × 50 = 250 7 × 24 = 168 Total 684 660.80 658 658 MYV = (SR × SQ) - (SR × SM) = 684 - 660.80 = 23.20(F) MMV = (SR × SM) - (SR × AQ) = 660.80 - 658 = 2.80(A) MUV = (SR × SQ) - (SR × AQ) = 684 - 658 = 26(F) MPV = (SR × AQ) - (AR × AQ) = 658 - 658 = NIL MCV = (SR × SQ) - (AR × AQ) = 684 - 658 = 26(F) 15 MATERIAL VARIANCES Q6 The standard cost of a company shows: Standard Mix: 40% of Material A at ₹ 10 per ton. 60% of Material B at ₹ 20 per ton. The normal loss in production is 10% of input. During the month of February 2022, the cost and production records reveal the following: 90 tons Material A at the cost of ₹ 9 per ton. 110 tons of Material B at the cost of ₹ 24 per ton. The yield produced 190 tons of good production. Calculate Material Variances. Sol Materials SR × SQ SR × SM SR × AQ AR × AQ A 10 × 84.4 = 844.44 10 × 80 = 800 10 × 90 = 900 9 × 90 = 810 B 20 × 126.6 = 2,533.33 20 × 120 = 2,400 20 × 110 = 2,200 24 × 110 = 2,640 Total 3,377.77 3,200 3,100 3,450 16 MATERIAL VARIANCES Sol Materials SR × SQ SR × SM SR × AQ AR × AQ A 10 × 84.4 = 844.44 10 × 80 = 800 10 × 90 = 900 9 × 90 = 810 B 20 × 126.6 = 2,533.33 20 × 120 = 2,400 20 × 110 = 2,200 24 × 110 = 2,640 Total 3,377.77 3,200 3,100 3,450 MYV = (SR × SQ) - (SR × SM) = 3,377.77 - 3,200 = 177.77(F) MMV = (SR × SM) - (SR × AQ) = 3,200- 3,100 = 100(F) MUV = (SR × SQ) - (SR × AQ) = 3,377.77 - 3,100 = 277.77(F) MPV = (SR × AQ) - (AR × AQ) = 3,100 - 3,450 = 350(A) MCV = (SR × SQ) - (AR × AQ) = 3,377.77 - 3,450 = 72.27(A) 17 LABOUR VARIANCES SR × ST SR × SM LYV SR × AT(W) LMV SR × AT(P) LITV AR × AT(P) LPV LEV TLEV LCV SR = Standard Rate (Always given) ST = Standard Time (for Actual Production) SM = Standard Mix [Total of AT(P) but in the ratio of ST] AT(W) = Actual Time Worked AT(P) = Actual Time Paid (Always given) AR = Actual Rate Note: 1. AT(W) = AT(P) - Idle Time 2. Calculation of Standard Time: A worker can produce 200 units in a day of 8 hours (standard) Actual output during the period is 50,000 units Therefore, Standard Time = 8 hours/200 units × 50,000 units = 2,000 hours 18 LABOUR VARIANCES Q7 From the following information, compute Labour Variances. Standard Workers A B Hours 10 15 Rate per hour (₹) 3.00 4.00 Total Amount (₹) 30.00 60.00 Rate per hour (₹) 3.00 4.50 Total Amount (₹) 60.00 22.50 Actual Workers A B Sol Hours 20 5 Workers SR × ST A B Total SR × SM SR × AT(W) SR × AT(P) AR × AT(P) 3 × 10 = 30 3 × 20 = 60 3 × 20 = 60 3 × 20 = 60 4 × 15 = 60 90 4 × 5 = 20 80 4 × 5 = 20 80 4.5 × 5 = 22.50 82.50 LEV = (SR × ST) - (SR × ATW) = 90 - 80 = 10(F) LPV = (SR × ATP) - (AR × ATP) = 80 - 82.50 = 2.50(A) LCV = (SR × ST) - (AR × ATP) = 90 - 82.50 = 7.50(F) 19 LABOUR VARIANCES Q8 Calculate Labour Variances from the following information: Labour Rate = Re 1 per hour Hours as Standard per unit = 12 Hours Actual Data: Units produced = 1,000 Actual Labour Cost = ₹ 10,000 Hours worked actually = 12,500 Hours Sol. ST = 12 Hours × 1,000 units = 12,000 Hours AR = ₹ 10,000/ 12,500 Hours = ₹ 0.80 per Hour SR × ST SR × SM SR × AT(W) SR × AT(P) AR × AT(P) 1 × 12,000 —— 1 × 12,500 1 × 12,500 0.8 × 12,500 12,500 12,500 10,000 12,000 LEV = (SR × ST) - (SR × ATW) = 12,000 - 12,500 = 500(A) LPV = (SR × ATP) - (AR × ATP) = 12,500 - 10,000 = 2,500(F) LCV = (SR × ST) - (AR × ATP) = 12,000 - 10,000 = 2,000(F) 20 LABOUR VARIANCES Q9 The following information relates to a manufacturing company: Number of employees 150 Weekly hours worked 30 Hours Standard Wage rate ₹ 0.50 per hour Standard Output 200 units per hour During the rst week of February 2022, 8 employees were paid at ₹ 0.45 per hour and 2 employees ar ₹ 0.55 per hour, the rest employees were paid at standard rates. Idle time is one hour per employee. Actual output was 6,250 units. Calculate Labour Variances. Sol. Standard Time = 150 employees × 30 Hours = 4,500 Hours Standard Production = 200 units per hour × 30 hours = 6,000 units Standard Time for Actual Production = 4,500 Hours/ 6,000 units × 6,250 units = 4,688 Hours SR × ST SR × SM SR × AT(W) SR × AT(P) AR × AT(P) 0.5 × 4,688 = 2,344 —— 0.5 × 4,350 = 2,175 0.5 × 4,500 = 2,250 0.45 × (8 × 30) = 108 0.55 × (2 × 30) = 33 0.50 × (140 × 30) = 2,100 2,344 2,175 2,250 2,241 fi 21 LABOUR VARIANCES Sol. Standard Time = 150 employees × 30 Hours = 4,500 Hours Standard Production = 200 units per hour × 30 hours = 6,000 units Standard Time for Actual Production = 4,500 Hours/ 6,000 units × 6,260 units = 4,688 Hours SR × ST SR × SM SR × AT(W) SR × AT(P) AR × AT(P) 0.5 × 4,688 = 2,344 —— 0.5 × 4,350 = 2,175 0.5 × 4,500 = 2,250 0.45 × (8 × 30) = 108 0.55 × (2 × 30) = 33 0.50 × (140 × 30) = 2,100 2,344 2,175 Idle Time: For 8 Employees = 1 Hour × 8 Employees = 8 Hours For 2 Employees = 1 Hour × 2 Employees = 2 Hours For 140 Employees = 1 Hour × 140 Employees = 140 Hours 2,241 LEV = (SR × ST) - (SR × ATW) = 2,344 - 2,175 = 169(F) LITV = (SR × ATW) - (SR × ATP) = 2,175 - 2,250 =75(A) TLEV = (SR × ST) - (SR × ATP) = 2,344 - 2,250 = 94(F) LPV = (SR × ATP) - (AR × ATP) = 2,250 - 2,241 = 9(F) LCV = (SR × ST) - (AR × ATP) = 2,344 - 2,241 = 103(F) AT(W) For 8 Employees = (8 × 30) - 8 Hours = 232 Hours For 2 Employees = (2 × 30) - 2 Hours = 58 Hours For 140 Employees = (140 × 30) - 140 Hours = 4,060 Hours Total of AT(W) 2,250 4,350 Hours 22 VARIABLE OVERHEAD VARIANCES SR × ST SR × AT AR × AT VO Expenditure Var VO E ciency Var VO Cost Var SR = Standard Rate (Always given) ST = Standard Time (for Actual Production) AT = Actual Time Paid (Always given) AR = Actual Rate ffi 23 VARIABLE OVERHEAD VARIANCES Q9 From the following information of G Ltd., Calculate Variable Overhead Variances. Budgeted Production = 6,000 units Budgeted Variable Overhead = ₹ 1,20,000 Standard time for one unit of output = 2 hours Actual Production = 5,900 units Variable Overhead Incurred = ₹ 1,22,000 Actual hours worked = 11,600 hours Sol. SR = ₹ 1,20,000/12,000 Hours = ₹ 10 per hour ST = 5,900 units × 2 Hours = 11,800 hours AR = ₹ 1,22,000/11,600 Hours = ₹ 10.517 per hour SR × ST SR × AT AR × AT 10 × 11,800 10 × 11600 10.517 × 11,600 1,18,000 1,16,000 1,22,000 VO Ef ciency Var = (SR × ST) - (SR × AT) = 1,18,000 - 1,16,000 = 2,000(F) VO Expenditure Var = (SR × AT) - (AR × AT) = 1,16,000 - 1,22,000 = 6,000(A) VO Cost Var = (SR × ST) - (AR × AT) = 1,18,000 - 1,22,000 = 4,000(A) fi 24 VARIABLE OVERHEAD VARIANCES Q 10 From the following information, Calculate Variable Overhead Variances. Standard hours per unit : 3 Variable overhead per hour : ₹ 5 Actual variable overhead incurred : ₹ 4,20,000 Actual output : 30,000 units Actual hours worked : 1,00,000 hours Sol. ST = 30,000 units × 3 Hours = 90,000 hours AR = ₹ 4,20,000/1,00,000 Hours = ₹ 4,20 per hour SR × ST SR × AT AR × AT 5 × 90,000 5 × 1,00,000 4.20 × 1,00,000 4,50,000 5,00,000 4,20,000 VO Ef ciency Var = (SR × ST) - (SR × AT) = 4,50,000 - 5,00,000 = 50,000(A) VO Expenditure Var = (SR × AT) - (AR × AT) = 5,00,000 - 4,20,000 = 80,000(F) VO Cost Var = (SR × ST) - (AR × AT) = 4,50,000 - 4,20,000 = 30,000(F) fi 25 FIXED OVERHEAD VARIANCES SR × SH SR × AH FO EFFICIENCY VAR SR × RBH FO CAPACITY VAR SR × BH FO CALENDER VAR AR × AH FO EXPENDITURE VAR FO VOLUME VAR FO COST VAR SR = Standard Rate of FO per hour [Budgeted FO/ Budgeted Hours] AR = Actual Rate SH = Standard Hours for Actual Production [Budgeted Hours/Budgeted Production × Actual Production] AH = Actual Hours (Always Given) BH = Budgeted Hours (Normally Given; If not then BH = BFO/BFO Rate Per hour) RBH = Revised Budgeted Hours 26 FIXED OVERHEAD VARIANCES Q 10 In Department ‘P’ of a plant, the following Standard Output for 40 hours per week Budgeted Fixed Overheads Actual Output Actual Hours Worked Actual Fixed Overheads Calculate Fixed Overhead Variances. Sol. SR = ₹ 2,800/40 Hours = ₹ 70 per hour SH = 40 Hours/2,800 Units × 2,400 Units = 34.28 hours SR × SH 70 × 34.28 Hrs = 2,400 2,400 data are submitted for the week ended 31st March, 2022: 2,800 units ₹ 2,800 2,400 units 35 Hours ₹ 3,000 SR × AH SR × RBH SR × BH AR × AH 70 × 35 Hrs = 2,450 70 × 40 Hrs = 2,800 70 × 40 Hrs = 2,800 85.71 × 35 Hrs = 3,000 2,450 2,800 2,800 3,000 FO Ef ciency Var = (SR × SH) - (SR × AH) = 2,400 - 2,450 = 50(A) FO Capacity Var = (SR × AH) - (SR × RBH) = 2,450 - 2,800 = 350(A) FO Calendar Var = (SR × RBH) - (SR × BH) = 2,800 - 2,800 = NIL FO Volume Var = (SR × SH) - (SR × BH) = 2,400 - 2,800 = 400(A) FO Expenditure Var = (SR × BH) - (AR × AH) = 2,800 - 3,000 = 200(A) fi FO Cost Var = (SR × SH) - (AR × AH) = 2,400 - 3,000 = 600(A) 27 FIXED OVERHEAD VARIANCES Q 10 Raghav Company Ltd. is having standard costing system in operation for quite some time. The following relating to the month of June, 2022 is available from the cost records: Output Operating Hours Fixed Overheads Working Days Sol. Budgeted 30,000 Units 25,000 Hours ₹ 50,000 25 Actual 32,500 Units 28,000 Hours ₹ 55,000 26 SR = ₹50,000/25,000 Hours = ₹2 per hour SH = 25,000 Hours/30,000 Units × 32,500 Units = 27,083 hours RBH = 25,000 Hours/25 Days × 26 Days = 26,000 Hours SR × SH SR × AH SR × RBH 2 × 27,083 Hrs = 54,167 54,167 2 × 28,000 Hrs 2 × 26,000 Hrs = 52,000 = 56,000 56,000 SR × BH AR × AH 2 × 25,000 Hrs = 50,000 1.96 × 28,000 Hrs = 55,000 50,000 55,000 52,000 FO Ef ciency Var = (SR × SH) - (SR × AH) = 54,167 - 56,000 = 1,833(A) FO Capacity Var = (SR × AH) - (SR × RBH) = 56,000 - 52,000 = 4,000(F) FO Calendar Var = (SR × RBH) - (SR × BH) = 52,000 - 50,000 = 2,000 (F) FO Volume Var = (SR × SH) - (SR × BH) = 54,167 - 50,000 = 4,167(F) FO Expenditure Var = (SR × BH) - (AR × AH) = 50,000 - 55,000 = 5,000(A) fi FO Cost Var = (SR × SH) - (AR × AH) = 54,167 - 56,000 = 833(A) 28 FIXED OVERHEAD VARIANCES Q 11 Mehak Ltd. has furnished you the following data: Budgeted Actual Number of Working Days 25 27 Production (in units) 20,000 22,000 Fixed Overheads ₹ 30,000 ₹ 31,000 Budgeted Fixed Overhead Rate is ₹ 1.00 per hour. In July, 2022, the actual hours worked were 31,500. Calculate Fixed Overhead Variances Sol. SH = 30,000 Hours/20,000 Units × 22,000 Units = 33,000 hours RBH = 30,000 Hours/25 Days × 27 Days = 32,400 Hours SR × SH SR × AH SR × RBH 1 × 33,000 Hrs = 33,000 1 × 31,500 Hrs = 1 × 32,400 Hrs = 32,400 31,500 33,000 31,500 32,400 SR × BH AR × AH 1 × 30,000 Hrs = 30,000 0.98 × 31,500 Hrs = 31,000 30,000 31,000 FO Ef ciency Var = (SR × SH) - (SR × AH) = 33,000 - 31,500 = 1,500(F) FO Capacity Var = (SR × AH) - (SR × RBH) = 31,500 - 32,400 = 900(A) FO Calendar Var = (SR × RBH) - (SR × BH) = 32,400 - 30,000 = 2,400 (F) FO Volume Var = (SR × SH) - (SR × BH) = 33,000 - 30,000 = 3,000(F) FO Expenditure Var = (SR × BH) - (AR × AH) = 30,000 - 31,000 = 1,000(A) fi FO Cost Var = (SR × SH) - (AR × AH) = 33,000 - 31,000 = 2,000(F) 29 SALES VARIANCES SR × SQ SR × SM Sales Quantity Variance (SQV) SR × AQ Sales Mix Variance (SMV) AR × AQ Sales Price Variance (SPV) Sales Volume Variance (SVV) Sales Value Variance SR = Standard Selling Price SQ = Standard Quantity of Sales SM = Standard Mix (Total of AQ but in the ratio of SQ) AQ = Actual Quantity Sold AR = Actual Selling Price NOTE: Arrows are in OPPOSITE direction. 30 SALES VARIANCES Q 12 The budgeted sales for one month and the actual results achieved are as under: Budget Material Quantity (Units) M N O P Total 2,500 Actual Amount (₹) 10,000 Quantity (Units) 1,000 Price (₹) 10.00 700 20.00 500 300 1,200 Price (₹) 12.50 Amount (₹) 15,000 14,000 800 15.00 12,000 30.00 15,000 600 30.00 18,000 50.00 15,000 400 60.00 24,000 54,000 3,000 69,000 You are required to calculate in respect of each product the Sales Variance. Sol Materials SR × SQ SR × SM SR × AQ AR × AQ M 10 × 1000 = 10,000 10 × 1200 = 12,000 10 × 1200 = 12,000 12.50 × 1200 = 15,000 N 20 × 700 = 14,000 20 × 840 = 16,800 20 × 800 = 16,000 15 × 800 = 12,000 O 30 × 500 = 15,000 30 × 600 = 18,000 30 × 600 = 18,000 30 × 600 = 18,000 P 50 × 300 = 15,000 50 × 360 = 18,000 50 × 400 = 20,000 60 × 400 = 24,000 Total 54,000 64,800 66,000 69,000 31 SALES VARIANCES Sol Materials SR × SQ SR × SM SR × AQ AR × AQ M 10 × 1000 = 10,000 10 × 1200 = 12,000 10 × 1200 = 12,000 12.50 × 1200 = 15,000 N 20 × 700 = 14,000 20 × 840 = 16,800 20 × 800 = 16,000 15 × 800 = 12,000 O 30 × 500 = 15,000 30 × 600 = 18,000 30 × 600 = 18,000 30 × 600 = 18,000 P 50 × 300 = 15,000 50 × 360 = 18,000 50 × 400 = 20,000 60 × 400 = 24,000 Total 54,000 64,800 66,000 69,000 Sales Quantity Var (SQV) = (SR × SM) - (SR × SQ) = 64,800 - 54,000 = 10,800(F) Sales Mix Variance (SMV) = (SR × AQ) - (SR × SM) = 66,000 - 64,800 = 1,200(F) Sales Volume Variance (SVV) = (SR × AQ) - (SR × SQ) = 66,000 - 54,000 = 12,000(F) Sales Price Variance (SPV) = (AR × AQ) - (SR × AQ) = 69,000 - 66,000 = 3,000(F) Sales Value Variance = (AR × AQ) - (SR × SQ) = 69,000 - 54,000 = 15,000(F) 32 UGC NET COMMERCE The devia ons between actual and standard cost is known as: (a) Mul ple analysis (b) Variable cost analysis (c) Variance analysis (d) Linear trend analysis ti ti 33 UGC NET COMMERCE The devia ons between actual and standard cost is known as: (a) Mul ple analysis (b) Variable cost analysis (c) Variance analysis (d) Linear trend analysis ti ti 34 UGC NET COMMERCE Overhead cost variances is: (a) The di erence between overheads recovered on actual output - actual overhead incurred. (b) The di erence between budgeted overhead cost and actual overhead cost. (c) Obtained by mul plying standard overhead absorp on rate with the di erence between standard hours for actual output and actual hours worked. (d) None of the above ff ti ti ff ff 35 UGC NET COMMERCE Overhead cost variances is: (a) The di erence between overheads recovered on actual output - actual overhead incurred. (b) The di erence between budgeted overhead cost and actual overhead cost. (c) Obtained by mul plying standard overhead absorp on rate with the di erence between standard hours for actual output and actual hours worked. (d) None of the above ff ti ti ff ff 36 FIXED OVERHEAD VARIANCES SR × SH SR × AH FO EFFICIENCY VAR SR × RBH FO CAPACITY VAR SR × BH FO CALENDER VAR AR × AH FO EXPENDITURE VAR FO VOLUME VAR FO COST VAR SR = Standard Rate of FO per hour [Budgeted FO/ Budgeted Hours] AR = Actual Rate SH = Standard Hours for Actual Production [Budgeted Hours/Budgeted Production × Actual Production] AH = Actual Hours (Always Given) BH = Budgeted Hours (Normally Given; If not then BH = BFO/BFO Rate Per hour) RBH = Revised Budgeted Hours 37 UGC NET COMMERCE Which of the following variance arises when more than one material is used in the manufacture of a product: (a) Material price variance (b) Material usage variance (c) Material cost variance (d) Material mix variance 38 UGC NET COMMERCE Which of the following variance arises when more than one material is used in the manufacture of a product: (a) Material price variance (b) Material usage variance (c) Material cost variance (d) Material mix variance 39 MATERIAL VARIANCES SR × SQ SR × SM MYV SR × AQ MMV AR × AQ MPV MUV MCV SR = Standard Rate SQ = Standard Quantity (for Actual Production) SM = Standard Mix (Total of AQ but in the ratio of SQ) AQ = Actual Quantity Consumed (for Actual Production) AR = Actual Rate NOTE: SR, AQ, and AR are always given. These can be need to compute SQ and SM. SQ is computed only when actual output is given. 40 UGC NET COMMERCE If standard hours for 100 units of output are 400 @ ₹ 2 per hour and actual hours taken are 380 @ ₹ 2.25 per hour, then the labour rate/pay variance is: (a) ₹ 95 (adverse) (b) ₹ 100 (adverse) (c) ₹ 25 (favourable) (d) ₹ 55 (adverse) 41 UGC NET COMMERCE If standard hours for 100 units of output are 400 @ ₹ 2 per hour and actual hours taken are 380 @ ₹ 2.25 per hour, then the labour rate/pay variance is: (a) ₹ 95 (adverse) (b) ₹ 100 (adverse) (c) ₹ 25 (favourable) (d) ₹ 55 (adverse) 42 LABOUR VARIANCES SR × ST SR × SM LYV SR × AT(W) LMV SR × AT(P) LITV AR × AT(P) LPV LEV TLEV LCV SR = Standard Rate (Always given) ST = Standard Time (for Actual Production) SM = Standard Mix [Total of AT(P) but in the ratio of ST] AT(W) = Actual Time Worked AT(P) = Actual Time Paid (Always given) AR = Actual Rate Note: 1. AT(W) = AT(P) - Idle Time 2. Calculation of Standard Time: A worker can produce 200 units in a day of 8 hours (standard) Actual output during the period is 50,000 units Therefore, Standard Time = 8 hours/200 units × 50,000 units = 2,000 hours 43 UGC NET COMMERCE Idle me variance is obtained by mul plying: (a) The di erence between standard and actual hours by the actual rate of labour per hour (b) The di erence between actual labour hours paid and actual labour hours worked by the standard rate (c) The di erence between standard and actual hours by the standard rate of labour per hour (d) None of the above. ti ff ff ff ti 44 UGC NET COMMERCE Idle me variance is obtained by mul plying: (a) The di erence between standard and actual hours by the actual rate of labour per hour (b) The di erence between actual labour hours paid and actual labour hours worked by the standard rate (c) The di erence between standard and actual hours by the standard rate of labour per hour (d) None of the above. ti ff ff ff ti 45 LABOUR VARIANCES SR × ST SR × SM LYV SR × AT(W) LMV SR × AT(P) LITV AR × AT(P) LPV LEV TLEV LCV SR = Standard Rate (Always given) ST = Standard Time (for Actual Production) SM = Standard Mix [Total of AT(P) but in the ratio of ST] AT(W) = Actual Time Worked AT(P) = Actual Time Paid (Always given) AR = Actual Rate Note: 1. AT(W) = AT(P) - Idle Time 2. Calculation of Standard Time: A worker can produce 200 units in a day of 8 hours (standard) Actual output during the period is 50,000 units Therefore, Standard Time = 8 hours/200 units × 50,000 units = 2,000 hours 46