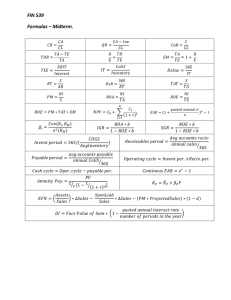

Chapter 9 – NPV Notes If NPV is positive, accept project. If NPV is negative, reject project Payback Period Issues o Ignores time value of money o Fails to consider risk differences o No economic rationale for looking at payback o Requires cutoff point o Biased against long-term projects Payback Period Advantages o Less cost from mistakes o Biased towards liquidity o Cash flows uncertain for future so payback ignores future CFs Discounted Payback Issues o May reject positive NPV o Requires cutoff point o Ignores cash flows beyond cutoff o Biased towards long-term projects Discounted Payback Advantages o Easy to understand o Includes time value of money o Does not accept negative NPV investments o Biased towards liquidity Average Accounting Return Disadvantages o Not true rate of return as time value ignored o Benchmark cutoff rate o Based on accounting values and not cash flow/market values AAR Advantages o Easy to calculate o Needed information usually available IRR Issues o Nonconventional cash flows o Mutually exclusive investments IRR Advantages o Closely related to NPV o Easy to understand o In percentages Modified Internal Rate of Return o Discounting Brings all negative cash flows to start and add cost o Reinvestment Compound all cash flows except first to end of project life o Combination Use both discounting and reinvestment Profitability Index Issues o May lead to incorrect decisions in comparisons of mutually exclusive investments PI Advantages o Closely related to NPV o Easy to understand o Maybe useful when investment funds limited Formulas Net Present Value 𝑁𝑃𝑉 = 𝑃𝑉 − 𝐶𝑜𝑠𝑡 Present Value 𝑃𝑉 = 𝐹𝑉 (1 + 𝑖)𝑛 Payback Period 𝑃𝑃 = 𝑌𝑒𝑎𝑟 + ( 𝐶𝐹𝑙𝑎𝑠𝑡 𝑛𝑒𝑔𝑎𝑡𝑖𝑣𝑒 𝐶𝐹 ) 𝐶𝐹𝑓𝑖𝑟𝑠𝑡 𝑝𝑜𝑠𝑖𝑡𝑖𝑣𝑒 𝐶𝐹 Average Accounting Return 𝐴𝐴𝑅 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐵𝑜𝑜𝑘 𝑉𝑎𝑙𝑢𝑒 𝐴𝐵𝑉 = 𝐵𝑒𝑔𝑖𝑛𝑛𝑖𝑛𝑔 − 𝐸𝑛𝑑𝑖𝑛𝑔 2 Average Book Value MIRR Discounting 𝐷𝑖𝑠𝑐𝑜𝑢𝑛𝑡𝑖𝑛𝑔 = 𝑌𝑒𝑎𝑟 𝑁 (1 + 𝑖)𝑛 MIRR Reinvestment 𝑅𝑒𝑖𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 = 𝑌𝑒𝑎𝑟 𝑁 + (𝑌𝑒𝑎𝑟1 × 𝑖) Profitability Index 𝑃𝐼 = 𝑃𝑉 𝐶𝑜𝑠𝑡 Chapter 10 – Capital Investment Decisions Notes Decisions based on incremental (relevant cost to project) cash flows and not net income Opportunity costs Cost of capital reflected in real required rate of return Cash flow analyzed on after-tax cash flows Standalone principle (mini-firms) who are not related to parent company Sunk costs are already incurred and cannot be removed, must not be considered Formulas Initial Investment (Expansion) 𝐼𝐼𝑒 = 𝐹𝐶 + 𝑁𝑊𝐶 Operating Cash Flows (Expansion) 𝑂𝐶𝐹𝑒 = (𝑆 − 𝐶 − 𝐷) × (1 − 𝑇) + 𝐷 Terminal Cash Flows (Expansion) 𝑇𝐶𝐹𝑒 = 𝑆𝑉 + 𝑁𝑊𝐶 − 𝑇 × (𝑆𝑉 − 𝐵𝑉) Initial Investment (Replacement) 𝐼𝐼𝑟 = 𝐹𝐶 + 𝑁𝑊𝐶 − 𝑆𝑉𝑜𝑙𝑑 + 𝑇 × (𝑆𝑉𝑜𝑙𝑑 − 𝐵𝑉𝑜𝑙𝑑 ) Operating Cash Flows (Replacement) 𝑂𝐶𝐹𝑟 = (∆𝑆 − ∆𝐶) × (1 − 𝑇) + 𝑇 × ∆𝐷 Terminal Cash Flows (Replacement) 𝑇𝐶𝐹𝑟 = ∆𝑆𝑉 + 𝑁𝑊𝐶 − 𝑇 × (∆𝑆𝑉 − ∆𝐵𝑉) Chapter 11 – Project Analysis & Evaluation Notes Operating Part starts from Sales until Operating Profit Financial Part starts from Operating Profit till EPS Marginal/Incremental Cost o Every unit increase in production leads to % change in total costs Payback & Breakeven o Project that does better than breakeven has shorter payback than project life and positive ROR. Project that breakeven on accounting basis have negative NPV and zero ROR. Lower the operating leverage, lower the fixed cost. Higher the OL, higher the risk DOL, DFL, DTL are all % changes in sensitivity respective to income statement. If I and D is 0, EPS/EBIT is 1, for every 1% change in EBIT, EPS change is 1% Capital Rationing o If firm has positive NPV but can’t find financing Soft Rationing o Units in business allocated for financing (within existing budget) Hard Rationing o Can’t raise financing under any circumstances (financial distress) Formulas Variable Costs 𝑇𝑉𝐶 = 𝑄 × 𝑣 Total Costs 𝑇𝐶 = 𝑇𝑉𝐶 + 𝐹𝐶 Average Cost 𝐴𝐶 = 𝑇𝐶 𝑄 General Break-Even 𝑄= 𝐹𝐶 + 𝑂𝐶𝐹 𝑃−𝑣 Accounting Break-Even 𝑄= 𝐹𝐶 + 𝐷 𝑃−𝑣 Cash Break-Even 𝑄= 𝐹𝐶 𝑃−𝑣 Financial Break-Even 𝑄= 𝐹𝐶 + 𝑂𝐶𝐹0 𝑃−𝑣 Degree of Operating Leverage 𝑆𝑎𝑙𝑒𝑠 − 𝑇𝑉𝐶 𝑆𝑎𝑙𝑒𝑠 − 𝑇𝑉𝐶 − 𝐹𝐶 %∆ 𝐸𝐵𝐼𝑇 𝐷𝑂𝐿 = %∆ 𝑆𝑎𝑙𝑒𝑠 𝐷𝑂𝐿 = 𝐷𝑂𝐿 = 1 + 𝐹𝐶 𝑂𝐶𝐹 Degree of Financial Leverage 𝐷𝐹𝐿 = 𝑆𝑎𝑙𝑒𝑠 − 𝑇𝑉𝐶 − 𝐹𝐶 1 𝑆𝑎𝑙𝑒𝑠 − 𝑇𝑉𝐶 − 𝐹𝐶 − 𝐼 − (𝐷𝑖𝑣𝑝 × (1 − 𝑇)) 𝐷𝐹𝐿 = %∆ 𝐸𝑃𝑆 %∆ 𝐸𝐵𝐼𝑇 Degree of Total Leverage 𝐷𝑇𝐿 = 𝑆𝑎𝑙𝑒𝑠 − 𝑇𝑉𝐶 1 𝑆𝑎𝑙𝑒𝑠 − 𝑇𝑉𝐶 − 𝐹𝐶 − 𝐼 − (𝐷𝑖𝑣𝑝 × (1 − 𝑇)) 𝐷𝑇𝐿 = %∆ 𝐸𝑃𝑆 %∆ 𝑆𝑎𝑙𝑒𝑠 Relationship between DOL, DFL, DTL 𝐷𝑇𝐿 = 𝐷𝑂𝐿 + 𝐷𝐹𝐿 %∆ 𝐸𝑃𝑆 %∆ 𝐸𝐵𝐼𝑇 %∆ 𝐸𝑃𝑆 = × %∆ 𝑆𝑎𝑙𝑒𝑠 %∆ 𝑆𝑎𝑙𝑒𝑠 %∆ 𝐸𝐵𝐼𝑇 Percentage Change % 𝐶ℎ𝑎𝑛𝑔𝑒 = 𝑁𝑒𝑤 − 𝑂𝑙𝑑 𝑂𝑙𝑑 Chapter 14 – Cost of Capital Notes External Financing o Common & Preferred Stocks, Bonds, Loans Internal Financing o Retained Earnings Cost Degree o Common Stock (Highest cost) o Retained Earnings o Preferred Stock o Loans o Bonds (Lowest cost) Dividend Growth Model Issues o Only for firms that pay dividends and assuming they are constant. Estimated cost of equity very sensitive to estimated growth rate, and does not explicitly consider risk CAPM Advantages o Adjusting for risk o Applicable to companies without constant dividend growth CAPM Issues o Market & Beta coefficient that need to be accurate otherwise provide poor results o Uses the past to predict the future Cost of Debt Advantage o Tax advantage on interest, which reduces overall after-tax rate. We tax interest expense first, so loan payment is lower. Pure-Play approach o When taking WACC based on companies in same field, with similar beta and capital structures in market Floatation Costs o Extra costs such as administrative or fees incurred when beginning project, such as marketing or commissions Formulas Cost of Equity (Dividend Growth Model) 𝐶𝑜𝑠𝑡𝐸 = 𝐷0 × (1 + 𝑔) 𝐷1 => 𝑖−𝑔 𝑖−𝑔 𝑅𝑒𝑞𝑢𝑖𝑟𝑒𝑑 𝑅𝑒𝑡𝑢𝑟𝑛(𝑖) = 𝐷1 +𝑔 𝑃𝑐 Cost of Equity (CAPM / SML) 𝐶𝐴𝑃𝑀 = 𝑅𝑓 + 𝛽(𝑅𝑚 − 𝑅𝑓 ) Cost of Preferred Equity 𝐶𝑜𝑠𝑡𝑃 = 𝐷 𝑃 Cost of Debt 𝐶𝑜𝑠𝑡𝐷 = 𝐶𝐹 𝐹𝑉 + 𝑛 (1 + 𝑖) (1 + 𝑖)𝑛 𝐶𝑜𝑠𝑡𝐷 = $1,000 − 𝑃 𝑛 $1,000 + 𝑃 2 𝐶+ After-tax Cost of Debt 𝐴𝑓𝑡𝑒𝑟𝑡𝑎𝑥 𝐶𝑜𝑠𝑡𝐷 = 𝑌𝑇𝑀 × (1 − 𝑇) Weighted Average Cost of Capital 𝑊𝐴𝐶𝐶 = (𝑤𝐷 × 𝑖𝐷 × (1 − 𝑇)) + (𝑤𝑃 × 𝑖𝑃 ) + (𝑤𝐸 × 𝑖𝐸 ) Chapter 16 – Financial Leverage & Capital Structure Policy Notes M&M Proposition I (Pie Model) o Value of firm is independent of firm’s capital structure. Consider pie chart where stocks are 40% and bonds are 60%. It is same if stocks are 60% and bonds are 40%. Changing capital structure does not change total value of firm M&M Proposition II (Linear Model) o Firm’s cost of equity capital is positive linear function of firm’s capital structure. As debt-equity ratio increases, increase in leverage raises risk of equity, increasing cost of equity. Business Risk o Equity risk from operating activities. Depends on assets & operations, unaffected by capital structure. Greater business risk, greater required return on assets, greater cost of equity Financial Risk o Equity risk from financial policy (capital structure) Interest Tax Shield o Interest paid on EBIT gives EBT which is then taxed, giving more net income than regular tax on EBIT M&M I (No Tax) o Value of levered firm equal to value of unlevered firm. o Implications are that capital structure is irrelevant, WACC is same no matter mixture of debt and equity used M&M I (Tax) o Value of levered firm equal to value of unlevered firm plus present value of interest tax shield o Implications are that debt financing is highly advantageous, and most optimal capital structure is 100% debt, as WACC decreases with increase in debt M&M II (No Tax) o Cost of equity rises as debt financing increases. o Risk of equity depends on business and financial risk M&M II (Tax) o Same implications regardless of tax or no tax Direct Bankruptcy Costs o Associated with bankruptcy such as legal & administrative expenses. Bondholders don’t get all what they are owed. Direct costs are disincentive to debt financing Indirect Bankruptcy Costs o Costs of avoiding bankruptcy filing incurred by financially distressed firm Financial Distress Costs o Direct & Indirect costs associated with going bankrupt Static Theory of Capital Structure o Firm borrows up to point where tax benefit from extra dollar in debt equals cost from increased probability of financial distress Static Theory Taxes o Tax benefit from leverage only to companies with tax-paying position. o Companies with high tax shields from other sources (depreciation) have less benefit from leverage o Higher the effective tax rate, greater the incentive to borrow Static Theory Financial Distress o Firms borrow less than firms with lower risk of financial distress. More costly for some firms depending on assets Market & Nonmarket Claims o Market claims can be bought & sold in financial markets o Nonmarket claims cannot be bought & sold in financial markets o Value of firm relates to market claims only and not nonmarket claims o Value of market claims may be affected by changes in capital structure o Increase in market claims has identical decrease in nonmarket claims Pecking Order (Internal Financing) o Companies issuing stocks is bad news for investors as it is expensive and shows stock is overvalued o Company issues bond shows that stock is undervalued Pecking Order Issues o No target capital structure No optimal debt-equity ratio. Capital structure determined by external financing and not internal financing o Profitable firms use less debt Profitable firms have greater internal financing, they need less external financing and less debt o Financial Slack To avoid selling new equity, companies stockpile on retained earnings Business Failure o Business terminated with loss to creditors Legal Bankruptcy o Firms and creditors bring petitions to federal court for bankruptcy to liquidate or reorganize firm Technical Insolvency o Firm is unable to meet its financial obligations Accounting Insolvency o Firms with negative net worth are insolvent on books. Liabilities exceed assets. Formulas M&M I 𝐷 𝑅𝐸 = 𝑅𝐴 + (𝑅𝐴 − 𝑅𝐷 ) × ( ) 𝐸 𝑇𝐶 × 𝐷 = 𝑇𝐶 × 𝐷 × 𝑅𝐷 𝑅𝐷 𝑉𝐴 = 𝑉𝐵 + 𝑇𝐶 × 𝐷 M&M II 𝐷 𝑅𝐸 = 𝑅𝐵 + (𝑅𝐵 − 𝑅𝐷 ) × ( ) × (1 − 𝑇𝐶 ) 𝐸 Bankruptcy Claims 𝐶𝐹 = 𝑃𝑠𝑡𝑜𝑐𝑘ℎ𝑜𝑙𝑑𝑒𝑟𝑠 + 𝑃𝑐𝑟𝑒𝑑𝑖𝑡𝑜𝑟𝑠 + 𝑃𝑔𝑜𝑣𝑒𝑟𝑛𝑚𝑒𝑛𝑡 + 𝑃𝑏𝑎𝑛𝑘𝑟𝑢𝑝𝑡𝑐𝑦 𝑐𝑜𝑢𝑟𝑡𝑠 + 𝑃𝑜𝑡ℎ𝑒𝑟 Value of Firm relative to market and nonmarket claims 𝑉𝑇𝑜𝑡𝑎𝑙 = 𝐸 + 𝐷 + 𝐺 + 𝐵 + ⋯ => 𝑉𝑀 + 𝑉𝑁 Chapter 17 – Dividends & Payout Policy Notes Dividends o Payments made out of firm earnings to owners (in cash or stock) Distribution o Payments made by firm to owners from sources other than retained earnings Types of Dividends o Regular Cash Dividends Payments made by firm to owners in normal business time o Extra Cash Dividends Extra dividends paid out, may not be repeated o Special Dividends One-time events that will not be repeated o Liquidating Dividends Paid off when business has been liquidated Dividend Payment Process o Declaration Date Date on which board of directors pass resolution to pay dividends o Cumulative Dividend Date One day before ex-dividend date Buyer gets dividend but sellers do not o Ex-Dividend Date One day before date of record where individuals entitled to dividends Sellers receive dividends but buyers do not o Date of Record Date which holder must be on record to receive dividends Sellers receive dividends but buyers do not o Date of Payments Dividends are mailed Dividend Policy and Value of Company Theories o Irrelevant Theory (M&M) Regardless of dividend distribution, company value remains same o Homemade Dividends (M&M) Investor has ability to change dividend policy of company to suit their needs, however dividends paid still result in value being same. o Taxes Company should pay less dividends Income tax is higher than capital gains tax, meaning profit is low if dividends are paid Negative Relationship o Desire for Current Income Prefer to pay dividends now to avoid future risks Positive Relationship o Information Content Effect Market’s reaction to change in corporate dividend payouts. If company pays high dividends, investors think company has good profits and share price will increase o Clientele Effect High payouts attract one group, and low payouts attract another Company must not change their dividend policy otherwise client biases might make older clients sell stocks Negative Relationship Stock Repurchase o Open Market Purchases Firm purchases own stock on stock exchange as a buyer, keeping identity anonymous o Tender Offers Firm announces to stockholders that it wants to buy fixed number of shares at specific price o Targeted Repurchase Repurchasing shares from specific individual stockholders Formulas Dividend Payout Ratio 𝐷𝑃 = 𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑 𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒 Dividend Yield 𝐷𝑌 = 𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑 𝑃𝑟𝑖𝑐𝑒 Dividend Per Share 𝐷𝑃𝑆 = 𝑇𝑜𝑡𝑎𝑙 𝐷𝑖𝑣𝑖𝑑𝑒𝑛𝑑𝑠 𝑆ℎ𝑎𝑟𝑒𝑠 𝑂𝑢𝑡𝑠𝑡𝑎𝑛𝑑𝑖𝑛𝑔 Chapter 18 – Short-term Finance & Planning Notes Activities that increase cash or sources of cash o Increasing long-term debt o Increasing equity o Increasing current liabilities o Decreasing current assets other than cash o Decreasing fixed assets Activities that decrease cash or uses of cash o Decreasing long-term debt o Decreasing equity o Decreasing current liabilities o Increasing current assets other than cash o Increasing fixed assets Operating Cycle o Period between acquiring inventory and collection of cash from receivables Inventory Period o Time taken to acquire and sell inventory Accounts Receivables Period o Time taken between sale of inventory and cash collected from receivables Accounts Payables Period o Time taken between receipt of inventory and payment for it Cash Cycle o Time between cash disbursement and cash collection Timeline of Operating Cycle o Inventory Purchased which starts Inventory Period and Payables Period o Cash paid for inventory which ends Payables Period and begins Cash Cycle o Inventory Sold which ends Inventory Period and begins Receivables Period o Cash Received which ends Receivables Period and Cash Cycle Operating Cycle and Firm’s Organizational Chart o Cash Manager Deals with cash, marketable securities, and short-term loans Collection, Concentration, Disbursement, Short-term investments, Shortterm borrowing, Banking relations o Credit Manager Deals with accounts receivables Monitoring & control of accounts receivables, and credit policy decisions o Marketing Manager Deals with accounts receivables Credit Policy Decisions o Purchasing Manager Deals with inventory and accounts payables Decisions about purchases and suppliers. May negotiate payment terms o Production Manager Deals with inventory and accounts payables Setting of production schedules and materials requirements o Payables Manager Deals with accounts payables Decisions about payment policies and whether to take discounts o Controller Deals with receivables and payables Accounting information about cash flows, reconciliation of payables, application of payments to receivables Cash cycle depends on inventory, receivables, and payables Cash cycle increases as inventory and receivables period get longer Cash cycle decreases as payables period get longer The longer the cash cycle, the more financing required Shorter the cash cycle, the lower firm’s investment in inventories and receivables, meaning lower assets and higher asset turnover Short-Term Financial Policy o Size of firm’s investment in current assets Flexible or accommodative policy would maintain high ratio of current assets to sales Keeping large balances of cash and marketable securities Making large investments in inventory Granting liberal credit turns resulting in higher receivables Restrictive policy would entail a low ratio of current assets to sales Keeping low cash balances and little investment in marketable securities Small investments in inventory Allowing few or no credit sales reducing receivables Carrying Costs Costs that rise with increases in level of investment in current assets Shortage Costs Costs that fall with increase in level of investments o Trading/Order Costs are costs of placing an order for more cash (brokerage costs) or more inventory (production setup costs) o Costs related to safety reserves for lost sales, lost customer goodwill, and disruption of production schedules Optimal current asset holdings are highest under flexible policy, where carrying costs are perceived to be low relative to shortage costs o Financing of current assets Flexible policy means less short-term debt and more long-term debt Restrictive policy means high proportion of short-term debt to long-term debt Total assets requirements may change over time General growth trend Seasonal Variation around trend Unpredictable day-to-day fluctuations With flexible policies, firm maintains higher overall level of liquidity Analysis of Financial Policy o Cash Reserves Surplus cash and little short-term borrowing Reduces probability that firm will experience financial distress o Maturity Hedging Matching maturities of assets and liabilities Financing inventories with short-term bank loans and fixed assets with long-term financing Risky because short-term interest rates are more volatile than long-term interest rates o Relative Interest Rates Short-term interest rates usually lower than long-term rates. More costly to rely on long-term borrowing as compared to short-term Cash Budget o Forecast of cash receipts and disbursements for next planning period Cash Payments o Payments of Payables for goods or services rendered by suppliers such as raw materials o Wages, taxes, and other expenses includes all regular costs of doing business o Capital expenditures are payments of cash for long-life assets o Long-term financing expenses includes interest payments on long-term debt outstanding and dividend payments Unsecured Loans o Line of Credit Committed lines include formal legal arrangements that usually involve commitment fee paid by firm to bank Non-committed lines include informal arrangements that allow firms to borrow up to previously specified limit without going through paperwork o Revolver Revolving credit arrangement similar to line of credit but usually open for more two or more years o Compensating Balance Money kept by firm with a bank in low-interest or non-interest bearing accounts as part of loan agreement Usually computed as monthly average of daily balances o Letter of Credit Bank issuing letter promises to make a loan if certain conditions are met Letter guarantees payment on shipment of goods May be subject to cancellation or not Secured Loans o Receivables Financing Secured short-term loan that involves either assignment or factoring of receivables o o o o o Under assignment, lender has receivables as security, but borrower still responsible if receivables can’t be collected Under conventional factoring, receivable is discounted and sold to lender (factor), and once sold, collection is factor’s problem and assumes full risk of default Under maturity factoring, factor forwards money on agreed-upon future date Credit Card Receivable Funding / Business Cash Advances Company goes to factor and receives cash up front, after which portion of each credit card sale routed directly to factor by credit card processor until loan paid off Purchase Order Financing Factor pays supplier who manufactures product, and when sale is completed, seller is paid and factor is repaid Inventory Loans Short-term loan to purchase inventory Blanket Inventory Lien gives lender lien against all borrower’s inventories (blanket covers everything on default) Trust receipt is device by which borrower holds specific inventory in trust for the lender Field Warehouse Financing involves public warehouse company acting as control agent to supervise inventory for lender Commercial Paper Short-term notes issued by large and highly rated firms Short maturities, ranging up to 270 days Issued directly and backs issue with special bank line of credit, and interest rate obtained is usually lower than rate bank would charge Trade Credit Increasing payables period May end up paying much higher price for purchases, making it expensive Formulas Cash 𝐶𝑎𝑠ℎ = 𝐿𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠𝑙𝑜𝑛𝑔 + 𝐸𝑞𝑢𝑖𝑡𝑦 + 𝐿𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠𝑐𝑢𝑟𝑟𝑒𝑛𝑡 − 𝐴𝑠𝑠𝑒𝑡𝑠𝑐𝑢𝑟𝑟𝑒𝑛𝑡−𝑐𝑎𝑠ℎ − 𝐴𝑠𝑠𝑒𝑡𝑠𝑙𝑜𝑛𝑔 Operating Cycle 𝑂𝐶 = 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑃𝑒𝑟𝑖𝑜𝑑 + 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑 Cash Cycle 𝐶𝐶 = 𝑂𝐶 − 𝑃𝑎𝑦𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑 Inventory Turnover 𝐼𝑇 = 𝐶𝑂𝐺𝑆 𝐴𝑣𝑔 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 Inventory Period 𝐼𝑃 = 𝐷𝑎𝑦𝑠 𝐼𝑇 Receivables Turnover 𝑅𝑇 = 𝐶𝑟𝑒𝑑𝑖𝑡 𝑆𝑎𝑙𝑒𝑠 𝐴𝑣𝑔 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 Receivables Period 𝑅𝑃 = 𝐷𝑎𝑦𝑠 𝑅𝑇 Payables Turnover 𝑃𝑇 = 𝐶𝑂𝐺𝑆 𝐴𝑣𝑔 𝑃𝑎𝑦𝑎𝑏𝑙𝑒𝑠 Payables Period 𝑃𝑃 = 𝐷𝑎𝑦𝑠 𝑃𝑇 Cash Collections 𝐶𝐶 = 𝐵𝑒𝑔𝑖𝑛𝑛𝑖𝑛𝑔 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 + 1 × 𝑆𝑎𝑙𝑒𝑠 2 Effective Interest Rate 𝐸𝐼𝑅 = 𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑃𝑎𝑖𝑑 𝐴𝑚𝑜𝑢𝑛𝑡 𝐴𝑣𝑎𝑖𝑙𝑎𝑏𝑙𝑒 Problems (Chapter 10) Question 1 Cost of Building = $24,000 Equipment Cost = $16,000 Initial Investment = $12,000 Economic Life = 4 Years Building MV = $15,000 Building BV = $21,816 Equipment MV = $4,000 Equipment BV = $2,720 Sales = $80,000 Costs = $58,000 Tax = 40% Cost of Capital = 12% Depreciation Year 1 = $3,512 Depreciation Year 2 = $5,744 Depreciation Year 3 = $3,664 Depreciation Year 4 = $2,544 Find the NPV 𝐼𝐼 = ($24,000 + $16,000) + $12,000 => −$52,000 𝑂𝐶𝐹1 = ($80,000 − $58,000 − $3,512) × (1 − 0.4) + $3,512 => $14,604.80 𝑂𝐶𝐹2 = ($80,000 − $58,000 − $5,744) × (1 − 0.4) + $5,744 => $15,497.60 𝑂𝐶𝐹3 = ($80,000 − $58,000 − $3,664) × (1 − 0.4) + $3,664 => $14,665.60 𝑂𝐶𝐹4 = ($80,000 − $58,000 − $2,544) × (1 − 0.4) + $2,544 => $14,217,60 𝑇𝐶𝐹𝑏𝑢𝑖𝑙𝑑𝑖𝑛𝑔 = $15,000 − 0.4 × ($15,000 − $21,816) => $17,726.40 𝑇𝐶𝐹𝑒𝑞𝑢𝑖𝑝𝑚𝑒𝑛𝑡 = $4,000 − 0.4 × ($4,000 − $2,720) => $3,488 𝑇𝐶𝐹 = $17,726.40 + $3,488 + $12,000 => $33,214.40 YEAR 0 1 2 3 4 ENDING PV Question 2 Cost of Old Printer = $15,000 Old Printer Life = 15 Years OCF -$52,000 $14,604.80 $15,497.60 $14,665.60 $14,217.60 TCF $33,214.40 $40,200 Old Printer Salvage = $0 Old Printer BV = $5,000 Cost of New Printer = $24,000 Change in Costs = $6,000 New Printer MV = $4,000 Old Printer MV = $2,000 Tax = 40% NWC = $3,000 Cost of Capital = 11.5% Depreciation Year 1 = $7,920 Depreciation Year 2 = $10,800 Depreciation Year 3 = $3,600 Depreciation Year 4 = $1,680 Depreciation Year 5 = $0 Find NPV 𝐼𝐼 = $24,000 + $3,000 − $2,000 + 40% × ($2,000 − $5,000) 𝑂𝐶𝐹1 = (0 − (−$6,000)) × (1 − 0.4) + 0.4 × ($7,920 − $1,000) => $6,368 𝑂𝐶𝐹2 = (0 − (−$6,000)) × (1 − 0.4) + 0.4 × ($10,800 − $1,000) => $7,520 𝑂𝐶𝐹3 = (0 − (−$6,000)) × (1 − 0.4) + 0.4 × ($3,600 − $1,000) => $4,640 𝑂𝐶𝐹4 = (0 − (−$6,000)) × (1 − 0.4) + 0.4 × ($1,680 − $1,000) => $3,872 𝑂𝐶𝐹5 = (0 − (−$6,000)) × (1 − 0.4) + 0.4 × ($0 − $1,000) => $3,200 𝑇𝐶𝐹 = ($4,000 − 0) + $3,000 − 0.4(($4,000 − 0) − ($0 − $0)) => $5,400 YEAR 0 1 2 3 4 5 ENDING PV OCF -$23,800 $6,368 $7,520 $4,640 $3,872 $3,200 TCF $5,400 $7,200 $6,368 $7,520 $4,640 $3,872 $8,600 + + + + = 1 2 3 4 (1 + 0.115) (1 + 0.115) (1 + 0.115) (1 + 0.115) (1 + 0.115)5 > −$1,197.28 𝑁𝑃𝑉 = $23,800 + Problems (Chapter 11) Question 1 Cost of Disk = $3 Selling Price = $5 Fixed Cost = $600 Depreciation = $300 Find breakeven $5 − $3 => $2 $600 + $300 => $900 𝐵𝑟𝑒𝑎𝑘𝑒𝑣𝑒𝑛 = $900 => 450 𝑑𝑖𝑠𝑘𝑠 $2 Question 2 Selling Price = $1.20 Variable Cost = $0.80 Fixed Cost = $360,000 Depreciation = $60,000 Find accounting breakeven Find DOL if quantity sold increases 10% above breakeven 𝑄= $360,000 + $60,000 => 1,050,000 $1.20 − $0.80 𝐷𝑂𝐿 = 1 + $360,000 => 7 $60,000 Question 3 Sales = $4,000,000 Firm A VC = $2 Firm A FC = $1 Firm B VC = $2.60 Firm B FC = $1.30 Firm C VC = $2.40 Firm C FC = $1.40 Find highest DOL 𝐷𝑂𝐿𝐴 = $4 − $2 => 2 $4 − $2 − $1 𝐷𝑂𝐿𝐵 = $4 − $2.60 => 14 $4 − $2.60 − $1.30 𝐷𝑂𝐿𝐶 = $4 − $2.40 => 8 $4 − $2.40 − $1.40 Question 4 Units Produced = 200,000 Selling Price = $3 VC = $2 FC = $75,000 Interest = $25,000 Find DOL and DTL 𝐷𝑂𝐿 = (200,000 × $3) − (200,000 × $2) => 1.6 (200,000 × $3) − (200,000 × $2) − $75,000 𝐷𝑇𝐿 = 200,000 × ($3 − $2) => 2 200,000 × ($3 − $2) − $75,000 − $25,000 Question 5 Liabilities = $200,000 Equity = $250,000 ROE = 15.60% Find DFL EBIT Interest Expense EBT Taxes Net Income Expected EBIT $80,000 ($15,000) $65,000 ($26,000) $39,000 𝐸𝑃𝑆1 = 𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒 $39,000 = = 0.156 𝑆ℎ𝑎𝑟𝑒𝑠 $250,000 𝐸𝑃𝑆2 = 𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒 $43,800 = = 0.175 𝑆ℎ𝑎𝑟𝑒𝑠 $250,000 0.175 − 0.156 = 0.122 0.156 %∆𝐸𝑃𝑆 = %∆𝐸𝐵𝐼𝑇 = 𝐷𝐹𝐿 = $88,000 − $80,000 = 0.1 $80,000 %∆𝐸𝑃𝑆 0.122 = = 1.22 %∆𝐸𝐵𝐼𝑇 0.1 Question 6 EBIT + 10% $88,000 ($15,000) $73,000 ($29,200) $43,800 10% increase in sales Increase in EPS from $1 to $1.50 No debt or preferred stock Find DOL No debt so DFL is removed from equation $1.50 − $1 50% $1 𝐷𝑂𝐿 = => => 5 10% 10% Question 7 Units Sold = 10,000 Selling Price = $5 FC = $8,000 Interest = $2,000 VC = $3 EBIT = $12,000 Find DFL and DTL 𝐷𝑂𝐿 = 𝐷𝑇𝐿 = (10,000 × $5) − (10,000 × $3) => 1.67 (10,000 × $5) − (10,000 × $3) − $8,000 (10,000 × $5) − (10,000 × $3) => 2 (10,000 × $5) − (10,000 × $3) − $8,000 − $2,000 − $0 Problems (Chapter 14) Question 1 Dividends Paid = $4 Stock Price = $60 Growth = 6% Find Cost of Equity 𝐷1 = $4 × (1 + 6%) => $4.24 𝐶𝑜𝑠𝑡𝐸 = $4.24 + 6% => 13.07% $60 Question 2 Beta = 1.2 Market Risk Premium = 7% Risk-free Rate = 6% Previous Dividend = $2 Growth = 8% Stock Price = $30 Find Cost of Equity 𝐶𝑜𝑠𝑡𝐸 = 6% + (1.2 × 7%) => 14.4% 𝐷1 = $2 × (1 + 8%) => $2.16 𝐶𝑜𝑠𝑡𝐸 = $2.16 + 8% => 15.2% $30 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐶𝑜𝑠𝑡𝐸 = 14.4% + 15.2% => 14.8% 2 Question 3 Preferred Stock Price = $100 First Stock Dividend = $4.52 Stock Sold at = $102.50 Second Stock Dividend = $4.92 Stock Sold at = $104.70 Find Cost of Preferred Stock 𝐶𝑜𝑠𝑡𝑃1 = $4.52 => 4.41% $102.50 𝐶𝑜𝑠𝑡𝑃2 = $4.92 => 4.70% $104.70 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐶𝑜𝑠𝑡𝑃 = 4.41% + 4.70% => 4.55% 2 Question 4 Stocks Outstanding = 1,400,000 Stock Price = $20 Debt traded of face value = 93% Total Face Value = $5,000,000 Debt Yield = 11% Risk-free rate = 8% Market Risk Premium = 7% Beta = 0.74 Tax = 21% Find WACC 𝐶𝑜𝑠𝑡𝐸 = 8% + (0.74 × 7%) => 13.18% 𝑉𝑎𝑙𝑢𝑒 𝑜𝑓 𝐸𝑞𝑢𝑖𝑡𝑦 = 1,400,000 × $20 => $28,000,000 𝑉𝑎𝑙𝑢𝑒 𝑜𝑓 𝐷𝑒𝑏𝑡 = 93% × $5,000,000 => $32,650,000 𝑊𝑒𝑞𝑢𝑖𝑡𝑦 = $28,000,000 => 85.76% $32,650,000 𝑊𝑑𝑒𝑏𝑡 = 1 − 85.76% => 14.24% 𝑊𝐴𝐶𝐶 = (85.76% × 13.18%) + (14.24% × 11% × (1 − 21%)) => 12.54% Question 5 Coupon Rate = 12% YTM = 14% Tax = 31% Find after-tax cost of debt 𝐴𝑓𝑡𝑒𝑟𝑡𝑎𝑥 𝐶𝑜𝑠𝑡𝐷 = 14% × (1 − 31%) => 9.66% Question 6 Coupon Rate = 6% Coupon Time = 7 Years Coupon Price = $940.54 Tax = 30% Find after-tax cost of debt 𝐶𝑜𝑠𝑡𝐷 = $1,000 − $940,54 7 => 7.06% $1,000 + $940.54 2 (6% × $1,000) + 𝐴𝑓𝑡𝑒𝑟𝑡𝑎𝑥 𝐶𝑜𝑠𝑡𝐷 = 7.06% × (1 − 30%) => 4.94% Question 7 Debt = 45% Preferred Stock = 10% Equity = 45% Current Stock Price = $20 Last Dividend = $1.50 Growth = 8% Preferred Stock Price = $50 Preferred Stock Yield = 6% Cost of Debt = 9% Tax = 46% Find Cost of Debt, Preferred Stock, Equity Find WACC 𝐶𝑜𝑠𝑡𝐷 = 9% 𝐶𝑜𝑠𝑡𝑃 = 6% × $50 = 6% $50 𝐷1 = $1.50 × (1 + 8%) = $1.62 𝐶𝑜𝑠𝑡𝐸 = $1.62 + 8% => 16.1% $20 𝑊𝐴𝐶𝐶 = (45% × 9% × (1 − 46%)) + (10% × 6%) + (45% × 16.1%) => 10.032% Question 8 Bonds (Debt) = 40% Preferred Stock = 5% Common Stock = 55% Bonds Cost = 7.5% Preferred Stock Cost = 11% Common Stock Cost = 15% Tax = 40% Find WACC 𝑊𝐴𝐶𝐶 = (40% × 7.5% × (1 − 40%)) + (5% × 11%) + (55% × 15%) => 10.6% Question 9 Debt = 30% Preferred Stock = 20% Common Stock = 50% Debt Cost = 10% Preferred Stock Cost = 11% Common Stock Cost = 18% Tax = 40% Find WACC 𝑊𝐴𝐶𝐶 = (30% × 10% × (1 − 40%)) + (20% × 11%) + (50% × 18%) => 13% Question 10 Earnings Paid in Dividends = 40% Growth = 9% Previous Earnings = $5 Current Stock Price = $42 Coupon Rate = 8% Coupon Yield = 7.5% Tax = 30% Find Cost of Equity Find After-tax Cost of Debt 𝐷0 = 40% × $5 = $2 𝐷1 = $2 × (1 + 9%) = $2.18 𝐶𝑜𝑠𝑡𝐸 = $2.18 + 9% => 14.19% $42 𝐴𝑓𝑡𝑒𝑟𝑡𝑎𝑥 𝐶𝑜𝑠𝑡𝐷 = 7.5% × (1 − 30%) => 5.25% Question 11 Debt = 40% Equity = 60% Bond Par = $1,000 Coupon Rate = 10% Maturity = 20 Years Coupon Selling price = $849.54 Beta = 1.2 Risk-free Rate = 10% Market Risk Premium = 5% Tax = 40% Find WACC 𝐶𝑜𝑠𝑡𝐸 = 10% + (1.2 × 5%) => 16% 𝐶𝑜𝑠𝑡𝐷 = $1,000 − $849.54 20 => 11.63% $1,000 + $849.54 2 (10% × $1,000) + 𝑊𝐴𝐶𝐶 = (40% × 11.63% × (1 − 40%)) + (60% × 16%) => 12.39% Question 12 Expansion = $50,000,000 Debt = $20,000,000 Equity = $30,000,000 Before-tax return on debt = 9% Return on equity = 14% Tax = 40% Find WACC 𝑊𝐷 = $20,000,000 => 40% $50,000,000 𝑊𝐸 = $30,000,000 => 60% $50,000,000 𝑊𝐴𝐶𝐶 = (40% × 9% × (1 − 40%)) + (60% × 14%) => 10.56% Question 13 Equity = $100 Debt = $300 Bonds Issued at = 9% Beta = 1.125 Risk-free rate = 6% Expected return in market = 14% Tax = 40% Find WACC 𝐶𝑜𝑠𝑡𝐸 = 6% + 1.125 × (14% − 6%) => 15% 𝐶𝑜𝑠𝑡𝐷 = 9% 𝑊𝐸 = $100 => 25% $400 𝑊𝐷 = $300 => 75% $400 𝑊𝐴𝐶𝐶 = (75% × 9% × (1 − 40%)) + (25% × 15%) => 7.8% Question 14 Debt = 40% Equity = 50% Preferred Stock = 10% YTM = 7% Preferred Stock Selling Price = $40 Preferred Stock Dividend = $4 Common Stock Selling Price = $25 Common Stock Dividend = $2 Growth = 7% Tax = 40% Find WACC 𝐶𝑜𝑠𝑡𝐷 = 7% 𝐶𝑜𝑠𝑡𝑃 = 𝐶𝑜𝑠𝑡𝐸 = $4 = 10% $40 $2 + 7% => 15% $25 𝑊𝐴𝐶𝐶 = (40% × 7% × (1 − 40%)) + (10% × 10%) + (50% × 15%) => 10.18% Question 15 Debt = 50% Equity = 50% Bond Yield = 10% Price of Stock = $31.50 Dividend = $3 Growth = 5% Tax = 40% Find WACC 𝐶𝑜𝑠𝑡𝐷 = 10% 𝐷1 = $3 × (1 − 5%) => $3.15 𝐶𝑜𝑠𝑡𝐸 = $3.15 + 5% => 15% $31.50 𝑊𝐴𝐶𝐶 = (50% × 10% × (1 − 40%)) + (50% × 15%) => 10.5% Problems (Chapter 18) Question 1 Beginning Inventory = $5,000 Ending Inventory = $7,000 Beginning Receivables = $1,600 Ending Receivables = $2,400 Beginning Payables = $2,700 Ending Payables = $4,800 Credit Sales Ended = $50,000 Cost of Goods Sold = $30,000 Calculate turnovers Calculate periods Calculate cycles $30,000 => 5 𝑡𝑖𝑚𝑒𝑠 $6,000 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑇𝑢𝑟𝑛𝑜𝑣𝑒𝑟 = 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 𝑇𝑢𝑟𝑛𝑜𝑣𝑒𝑟 = 𝑃𝑎𝑦𝑎𝑏𝑙𝑒𝑠 𝑇𝑢𝑟𝑛𝑜𝑣𝑒𝑟 = $30,000 => 8 𝑡𝑖𝑚𝑒𝑠 $3,750 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑃𝑒𝑟𝑖𝑜𝑑 = 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑 = 𝑃𝑎𝑦𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑 = $50,000 => 25 𝑡𝑖𝑚𝑒𝑠 $2,000 365 => 73 𝑑𝑎𝑦𝑠 5 365 => 14.6 𝑑𝑎𝑦𝑠 25 365 => 45.6 𝑑𝑎𝑦𝑠 8 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐶𝑦𝑐𝑙𝑒 = 73 + 14.6 => 87.6 𝑑𝑎𝑦𝑠 𝐶𝑎𝑠ℎ 𝐶𝑦𝑐𝑙𝑒 = 87.6 − 45.6 => 42 𝑑𝑎𝑦𝑠 Question 2 Inventory Period = 90 days Receivables Period = 60 days Payables Period = 30 days Operating Cycle Investments = $30,000,000 Working Days = 360 days Find Operating Cycle Find Cash Conversion Cycle Find amount of resources needed to support firm’s cash conversion cycle 𝑂𝐶 = 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑃𝑒𝑟𝑖𝑜𝑑 + 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑 𝑂𝐶 = 90 𝑑𝑎𝑦𝑠 + 60 𝑑𝑎𝑦𝑠 => 150 𝑑𝑎𝑦𝑠 𝐶𝐶 = 𝑂𝐶 − 𝑃𝑎𝑦𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑 𝐶𝐶 = 150 𝑑𝑎𝑦𝑠 − 30 𝑑𝑎𝑦𝑠 => 120 𝑑𝑎𝑦𝑠 𝑆𝑎𝑙𝑒𝑠 𝐴𝑚𝑜𝑢𝑛𝑡 𝑁𝑒𝑒𝑑𝑒𝑑 = ( ) × 𝐶𝐶 360 $30,000,000 𝐴𝑚𝑜𝑢𝑛𝑡 𝑁𝑒𝑒𝑑𝑒𝑑 = ( ) × 120 => $10,000,000 360 Three ways to decrease cash conversion cycle Collect receivables quicker by offering discounts to debtors to repay early Decrease number of days inventory is on hand by having sales and discount on stock Extend payables period by having good relationship with suppliers Question 3 Inventory Turnover = 6 times Average Collection Period = 45 days Average Payment Period = 30 days Operating Cycle Investment = $3,000,000 Working Days = 360 days Calculate CC cycle, daily cash operating expenditure, and amount of resources needed to support CC cycle Find CC cycle and resource investment if average age of inventory is shortened by 5 days, receivables speed up by 10 days, and payment extended by 10 days Find increase or decrease in profit of CC cycle if firm pays 13% for its resource investment 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑃𝑒𝑟𝑖𝑜𝑑 = 365 => 60.83 𝑑𝑎𝑦𝑠 6 𝐶𝐶 = 60.83 + 45 − 30 => 75.83 𝑑𝑎𝑦𝑠 𝐴𝑚𝑜𝑢𝑛𝑡 𝑁𝑒𝑒𝑑𝑒𝑑 = ( $3,000,000 ) × 75.83 => $631,916.67 360 𝐷𝑎𝑖𝑙𝑦 𝐶𝑎𝑠ℎ 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐸𝑥𝑝𝑒𝑛𝑑𝑖𝑡𝑢𝑟𝑒 = $631,916.67 => $8,333.33 75.83 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑃𝑒𝑟𝑖𝑜𝑑𝑛𝑒𝑤 => 60.83 − 5 => 55.83 𝑑𝑎𝑦𝑠 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑𝑛𝑒𝑤 => 45 − 10 => 35 𝑑𝑎𝑦𝑠 𝑃𝑎𝑦𝑎𝑏𝑙𝑒𝑠 𝑃𝑒𝑟𝑖𝑜𝑑𝑛𝑒𝑤 => 30 + 10 => 40 𝑑𝑎𝑦𝑠 𝐶𝐶𝑛𝑒𝑤 = 55.83 + 35 − 40 => 50.83 𝑑𝑎𝑦𝑠 𝐴𝑚𝑜𝑢𝑛𝑡 𝑁𝑒𝑒𝑑𝑒𝑑𝑛𝑒𝑤 = ( $3,000,000 ) × 50.83 𝑑𝑎𝑦𝑠 => $423,583.33 360 𝐷𝑎𝑖𝑙𝑦 𝐶𝑎𝑠ℎ 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐸𝑥𝑝𝑒𝑛𝑑𝑖𝑡𝑢𝑟𝑒𝑛𝑒𝑤 = $423,583.33 => $8,333.33 50.83 𝑅𝑒𝑑𝑢𝑐𝑡𝑖𝑜𝑛 𝑖𝑛 𝐶𝐶 = 75.83 − 50.83 => 25 𝑑𝑎𝑦𝑠 𝐴𝑑𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡 = 𝑅𝑒𝑑𝑢𝑐𝑡𝑖𝑜𝑛 𝑖𝑛 𝐶𝐶 × 𝐷𝑎𝑖𝑙𝑦 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐶𝑎𝑠ℎ 𝐸𝑥𝑝𝑒𝑛𝑑𝑖𝑡𝑢𝑟𝑒 × 𝑅𝑒𝑠𝑜𝑢𝑟𝑐𝑒 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 𝐴𝑑𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙 𝑃𝑟𝑜𝑓𝑖𝑡 = 25 × $8,333.33 × 13% => $27,083.32 As additional profit is less than $35,000, the proposed effort should be rejected Question 4 Month Jan Feb Mar Apr May Jun Amount $2,000,000 $2,000,000 $2,000,000 $4,000,000 $6,000,000 $9,000,000 Month Jul Aug Sep Oct Nov Dec Amount $12,000,000 $14,000,000 $9,000,000 $5,000,000 $4,000,000 $3,000,000 Dividend firm’s monthly funds requirement into permanent and season component Find monthly average for permanent and seasonal component Describe amount of long-term and short-term financing used to meet total funds requirement under aggressive and conservative funding strategy Assume short-term funds cost 12% annually and long-term funds cost 17%. Use averages to calculate total cost of each strategies Discuss profitability-risk tradeoffs associated with aggressive and conservative strategy MONTH TOTAL FUND REQUIREMENTS JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC $2,000,000 $2,000,000 $2,000,000 $4,000,000 $6,000,000 $9,000,000 $12,000,000 $14,000,000 $9,000,000 $5,000,000 $4,000,000 $3,000,000 PERMANENT REQUIREMENTS $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000 SEASONAL REQUIREMENTS $0 $0 $0 $2,000,000 $4,000,000 $7,000,000 $10,000,000 $12,000,000 $7,000,000 $3,000,000 $2,000,000 $1,000,000 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑃𝑒𝑟𝑚𝑎𝑛𝑒𝑛𝑡 𝑅𝑒𝑞𝑢𝑖𝑟𝑒𝑚𝑒𝑛𝑡𝑠 = $2,000,000 𝑇𝑜𝑡𝑎𝑙 𝑆𝑒𝑎𝑠𝑜𝑛𝑎𝑙 𝑅𝑒𝑞𝑢𝑖𝑟𝑒𝑚𝑒𝑛𝑡𝑠 = $48,000,000 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑆𝑒𝑎𝑠𝑜𝑛𝑎𝑙 𝑅𝑒𝑞𝑢𝑖𝑟𝑒𝑚𝑒𝑛𝑡𝑠 = $48,000,000 => $4,000,000 12 Aggressive Strategy o Firm borrows between $1,000,000 to $12,000,000 according to seasonal requirement shown in table at prevailing short-term rate. Firm will borrow $2,000,000 as permanent portion at prevailing long-term rate o 𝐴𝑔𝑔𝑟𝑒𝑠𝑠𝑖𝑣𝑒 = ($2,000,000 × 17%) + ($4,000,000 × 12%) => $820,000 Conservative Strategy o Firm would borrow at peak need level of $14,000,000 at prevailing long-term rate o 𝐶𝑜𝑛𝑠𝑒𝑟𝑣𝑎𝑡𝑖𝑣𝑒 = ($14,000,000 × 17%) => $1,960,000 Looking at the strategies, the financing cost difference shows that aggressive strategy is more attractive. The higher returns have higher risks. The conservative strategy requires firm to pay interest on un-needed funds so the cost is higher. Thus, aggressive strategy more profitable but also more risky.