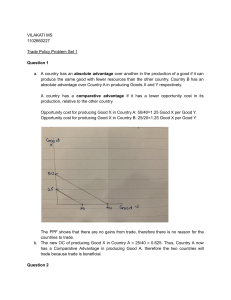

PRINCIPLES OF ECONOMICS DR/ SAMIA SAMY Basic Economic Concepts • This module introduces you to: • Economics main concepts. • Definition of economics. • The differences between microeconomics and macroeconomics. • Economic Problem. • The Economic Way of Thinking. • How People Make Decisions?(opportunity cost). • Production Possibility Frontier (PPF) Theory. Introduction. * the household must allocate its scarce resources among its various members, taking into account each member’s abilities, efforts and desires. • A society faces many decisions too: -A society must decide what jobs will be done and who will do them. -It needs some people to grow food, other people to make clothing. A society must also allocate the output of goods and services that it produces. • The management of society’s resources is important because resources are scarce. Scarcity means that the society has limited resources and therefore cannot produce all the goods and services people wish to have. Economics Is economics about money? How people make it and spend it? Is it about business, government, and jobs? Is economics about why some people and some nations are rich and others poor? Economics is about all these things, but its core is the study of choices and their consequences, in the presence of scarcity Your life will be shaped by the challenges you face and the opportunities that you create. But to face those challenges and maximize the opportunities, you must understand the economics as a guide to your decisions. Definition of Economics. Economics is driven by two certain realities. • First, the society has limited resources. • Second, our wants and desires are unlimited. We all want more. Economics is generally defined as the study of how our limited resources are allocated to satisfy our unlimited wants for goods and services. Economics is the social science that studies the choices that individuals, businesses, governments, and societies make as they cope with scarcity. Economics – the study of how society manages its scarce resources. ** SCARCITY • THE LIMITED NATURE OF SOCIETY’S RESOURCES. • SOCIETY HAS SHORTAGE OF RESOURCES AND THEREFORE CANNOT PRODUCE ALL THE GOODS AND SERVICES PEOPLE NEED. • THE COMBINATION OF LIMITED RESOURCES AND UNLIMITED WANTS IMPLIES A SHORTAGE, OR SCARCITY. • SCARCITY FORCES US TO MAKE CHOICES, AFTER TRADEOFFS. **TRADEOFFS • DECISIONS ABOUT WHAT TO DO, WHICH NECESSARILY INVOLVE DECISIONS ABOUT WHAT NOT TO DO. • WHEN WE SACRIFICE ONE THING TO OBTAIN ANOTHER, THAT'S CALLED A TRADE-OFF. opportunity cost . Only have enough cash to buy a car or an apartment, but not both? That's a trade-off. Trade-offs creates opportunity costs, one of the most important concepts in economics. Whenever you make a trade-off, the thing that you do not choose is your opportunity cost. Opportunity cost is the route not taken : You bought that car? Then the apartment was your opportunity cost. Efficiency and Equity Efficiency and Equity Efficiency is a measurable concept that can be determined by determining the ratio of useful output to total input. It minimizes the waste of resources while successfully achieving the desired output. means that society is getting the maximum it can from its scarce resources. Equity – means that the benefits of those resources are distributed equally among society’s members. • Policies such as taxes and welfare make incomes more equal but these policies reduce returns to hard work, and, therefore the economy doesn’t produce as much. Economics divides in two main parts: Microeconomics is the study of choices that individuals and businesses make, the way those choices interact in markets, and the influence of governments. An example of a microeconomic question is: Why are people buying more e-books and fewer hard copy books? Macroeconomics is the study of the performance of the national and global economies. An example of a macroeconomic question is: Why is the unemployment rate in the United States so high? Economic Problem. In order to solve the problem of scarcity all societies, must to answer three basic questions. What to produce? the best combination of goods and services to meet their needs How to produce? the best combination of factors to create the desired output of goods and services. For whom to produce? who will get the output from the country’s economic activity, and how much they will get. The Factors of Production Goods and services are produced by using productive resources that economists call factors of production. The factors of production are the inputs that are used in the production of goods or services in order to make an economic profit. (How to produce?) The factors of production include: Land: this is a short-hand expression for any natural resource in addition to land Labor: this includes labor defined in terms of quantity the number of workers and quality (the skills these workers possess) Capital: this includes the physical plants, machinery and equipment used to produce other goods and services entrepreneurship is The human resource that organizes land, labor, and capital. Each factor gets an income or return; Land earns rent. Labor earns wages. Capital earns interest. Entrepreneur earns profit Characteristics of Resources Quality of resources Productivity of resources Affected by technology, education and training of workforce. We achieve economic growth by increasing the quantity and/or quality of resources, or by technological development. Consumer Needs and Wants Needs: Are those things necessary to human survival e.g. food, shelter Wants: goods/services desired by the consumer e.g. travel, luxury cars Characteristics: Unlimited Recurrent Complementary Changeable The Economic Way of Thinking 1. Society’s wants are unlimited, but ALL resources are limited (scarcity). 2. Due to scarcity, choices must be made. Every choice has a cost (a trade-off). 3. Everyone’s goal is to make choices that maximize their satisfaction. Everyone acts in their own “self-interest.” 4. Everyone acts rationally by comparing the costs and benefits of every choice. 5. Real-life situations can be explained and analyzed through simplified models and graphs. The Economic Way of Thinking How do people choose rationally? The answers turn on benefits and costs. Benefit: What you Gain The benefit of something is the gain or pleasure that it brings and is determined by preferences. Preferences are what a person likes and dislikes and the intensity of those feelings. How People Make Decisions? 1. People face tradeoffs To get one thing that we like, we usually have to give up another thing that we like. Making decisions requires trading off one goal against another. Only have enough cash to buy a car or an apartment, but not both? That's a trade-off. 2. The Cost of Something Is What You Give Up to Get It Whenever you make a trade-off, the thing that you do not choose is your opportunity cost. Opportunity cost is the route not taken: You bought that car? Then the apartment was your opportunity cost. Production Possibility Frontier (PPF) Theory A simplified economic model which portrays scarcity, choice and opportunity cost. Production possibilities frontier (PPF) A curve showing the maximum attainable combinations of two products that may be produced with available resources and current technology. The static PPF The Static Production Possibility Frontier Analyses the economy at a fixed point in time Is based on the following assumptions: There is a fixed quantity of resources The economy only produces two products Resources can be used interchangeably All resources within the economy are used Resources are used at maximum efficiency (Economic efficiency assumes minimum cost for the production of a good or service, maximum output) An Example of the Static PPF Model The PPF Graph Maximum Output Levels The PPF shows the maximum output of the economy If the economy devotes all of its resources to the production of VCRs it is able to produce 800 (+ zero tractors)—Production Possibility A Alternatively, if the economy chooses Production Possibility C it is able to produce 200 tractors and 400 VCRs The PPF shows that to produce more of one product means producing less of another Opportunity costs of production can be measured e.g. if the economy moves from point C to D (along the PPF) it will produce an extra 100 tractors BUT 200 VCRs must be sacrificed Hence the opportunity cost is 200 VCRs Points Outside the Static PPF Points outside the PPF are not possible or unattainable using existing technology and resources Points Inside the Static PPF At point z, the economy is satisfying fewer needs and wants than is possible This is due to: Resources not being fully employed and/or Resources not being used in the most efficient way. So point z is attainable but not efficient. The Dynamic PPF Model This model differs from the static PPF in that it incorporates changes over time It demonstrates the effect of changes in the quantity and quality of productive resources e.g. new resource discoveries, improvements in technology. Changes in the quantity and/or quality of resources will SHIFT the PPF When the quality/quantity of resources increases (decreases), the economy can produce more (less) of both products and the entire curve will SHIFT outwards to right or (inwards to left), when the PPF shift up that mean achieving economic growth but when it shift down that mean an economic recession. The Dynamic PPF Model