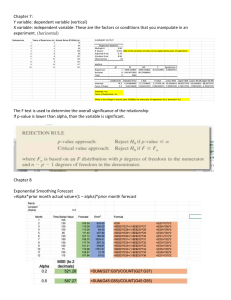

Formulas for Model-3 ( chapter 6) Time series decomposition and exponential smoothing Time series can be decomposed into four parts: 1. 2. 3. 4. Trend Seasonal component Cyclical Irregular Step1: Smoothing the time series with Moving average Moving average- 4 months =Average(Average(Q1:Q4), Average(Q2:Q5)) It removes the seasonality from the data Step -2 : Isolating the seasonality of a time series 1. Raw seasonal: ( it is used in the normalization for seasonality decomposition) Formula= Sales/ moving average 2. Create a small table with three columns Quarters 1 Raw factor =Averageif (quarters range, quarters number from this table, raw seasonal range) 2 3 4 3. Seasonal Index Vllokup ( qtr no, above table range, col-indx-no) 4. Isolating the Irregularities: =sales/ ( Moving average*seasonal index) 5. Reconstruction: = Moving average*seasonal index* irregulaties Normalisation = Raw factor / average of Raw factors Exponential smoothing: Exponential smoothing refers to a type of weighted average where largest weight is given to the most recent observation, and the weights on the prior observations decline exponentially over time. Steps: 1. Alpha = 0.25 ( initial value) 2. Exponential smoothing = Initial cell = sales Second cell= exponential smoothing previous +(alpha*(previous sales- previous exp smoothing)) 1. MSE = SUMXMY2(Sales series: Exponential smoothing series)/ count( sales series) 2. MAPE =Average(Abs(sales series-exp smoothing series)/sales series) Plot the line graph with three series Re-estimate the alpha by using solver 1. set MSE is equal to zero 2. By changing Alpha value 3. Constrains alpha value should be >= 0 and <= 1