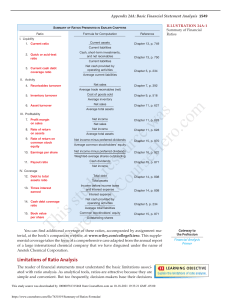

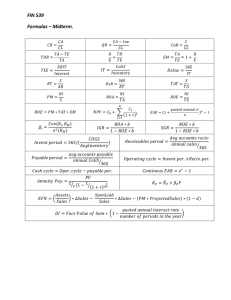

Financial Reporting and Analysis Formula Sheet www.365careers.com Financial Reporting and Analysis BASICS OF ACCOUNTING Basic Accounting Equation Assets = Liabilities + Equity Net income Net income = Revenue – Expenses Gross profit (income) Gross profit (income) = Revenue – Cost of goods sold Operating profit (income) Operating profit (income) = = Profit before interest and tax (PBIT) = Gross profit – Operating expenses Profit Before Tax (PBT) Profit before tax (PBT) = PBIT – Interest expense Net profit (income) Net profit (income) = = PBT – Tax expense = = Operating profit – Interest Expense – Tax expense Financial Reporting and Analysis UNDERSTANDING INCOME STATEMENTS Basic EPS = Basic Earnings per Share (EPS) Diluted Earnings per Share (DEPS) Net Income - Preferred Dividends Weighted average number of common shares outstanding Diluted EPS = Adjusted income available for common shares Weighted average common and potential common shares outstanding ][ [ Net - Preferred income dividends Diluted EPS = ( )( Weighted average shares + + )( Shares from conversion of conv. pfd. shares Gross profit margin Gross profit margin = Net profit margin Net profit margin = ][ Convertible preferred dividends Gross profit Revenue Net profit Revenue + ] Convertible (1 - t) debt interest Shares from )( Shares ) + conversion of + issuable from conv. debt stock options Financial Reporting and Analysis UNDERSTANDING BALANCE SHEETS LIQUIDITY RATIOS Current assets Current ratio Current ratio = Quick ratio Quick ratio = Cash + Short-term marketable securities + Receivables Current liabilities Cash ratio Cash ratio = Cash + Short-term marketable securities Current liabilities Current liabilities SOLVENCY RATIOS Long-term debt-to-equity Long-term debt-to-equity = Total debt-to-equity Total debt-to-equity = Debt ratio Debt ratio = Financial leverage Financial leverage = Long-term debt Total equity Total debt Total equity Total debt Total assets Total assets Total equity Financial Reporting and Analysis UNDERSTANDING CASH FLOW STATEMENTS FREE CASH FLOW MEASURES FCFF = CFO + [Int × (1 – tax rate)] – FCInv CFO = Cash flow from operations Int = Cash interest paid FCInv = Fixed capital investment (net capital expenditures) FCFF = NI + NCC + [Int × (1 – tax rate)] – FCInv - WCInv NI = Net income NCC = Non-cash charges (depreciation and amortization) Int = Cash interest paid FCInv = Fixed capital investment (net capital expenditures) WCInv = Working capital investment FCFE = CFO – FCInv + Net borrowing CFO = Cash flow from operations FCInv = Fixed capital investment (net capital expenditures) Net borrowing = Debt issued – debt repaid CASH FLOW RATIOS PERFORMANCE RATIOS Cash flow from operations Revenue Cash flow-to-revenue Cash flow-to-revenue = Cash-to-income Cash-to-income = Cash return-on-assets Cash return-on-assets = Cash flow from operations Average total assets Cash return-on-equity Cash return-on-equity = Cash flow from operations Average total equity Cash flow per share Cash flow per share = Cash flow from operations Operating income CFO - Preferred dividends Weighted average number of common shares Financial Reporting and Analysis UNDERSTANDING CASH FLOW STATEMENTS CASH FLOW RATIOS COVERAGE RATIOS Cash fow from operations Total debt Debt coverage Debt coverage = Interest coverage Interest coverage = Reinvestment ratio Reinvestment ratio = Debt payment Debt payment = Dividend payment Dividend payment = Investing and financing ratio Investing and financing ratio = CFO + Interest paid + Taxes paid Interest paid Cash flow from operations Cash paid to acquire long-term assets Cash flow from operations Cash paid to repay long-term debt Cash flow from operations Dividends paid Cash flow from operations Cash outflows from investing and financing activities Financial Reporting and Analysis RATIO ANALYSIS ACTIVITY RATIOS Meaning Receivables turnover = Annual sales Average receivables Days of sales outstanding = Cost of goods sold Average inventory Inventory turnover = Days of inventory on hand = Payables turnover = 365 Receivables turnover 365 Inventory turnover Purchases Average trade payables Number of days of payables = Fixed assets turnover = Revenue Average net fixed assets Working capital turnover = Total assets turnover = 365 Payables turnover ratio Revenue Average working capital Revenue Average total assets Cash conversion cycle = Days of sales outstanding + Days of inventory on hand - Number of days of payables Equity turnover = Revenue Average total equity The efficiency of a company in collecting its trade receivables The average number of days a company takes to collect its receivables from clients The efficiency of a company in terms of inventory management The average inventory processing period The efficiency of a company in allowing trade credit to suppliers The average number of days a company takes to pay its suppliers The efficiency of a firm in utilizing its fixed assets The efficiency of a firm in managing its working capital (current assets - current liabilities) The efficiency of a firm in using its total assets to create revenue The number of days a company takes to convert its investments in inventory and other resources into cash flows from sales The efficiency of a firm in utilizing equity to create revenue Financial Reporting and Analysis RATIO ANALYSIS LIQUIDITY RATIOS Meaning Current ratio = Quick ratio = Cash ratio = Current assets Current liabilities Ability to meet current liabilities (with total current assets) Cash + Marketable securities + Receivables Current liabilities Cash + Marketable securities Current liabilities Defensive Cash + Marketable securities + Receivables interval = Average daily expenditure Ability to meet current liabilities (with total current assets, excluding inventory) Ability to meet current liabilities (with cash and marketable securities only) The number of days a company can cover its average daily expenses with the use of current liquid assets only SOLVENCY RATIOS Debt-to-equity = Total debt Total shareholder’s equity Debt as a percentage of total equity Debt-to-capital = Total debt Total debt + Total shareholder’s equity Debt as a percentage of total capital Debt-to-assets = Total debt Total assets Debt as a percentage of total assets Financial leverage = Interest coverage = Average total assets Average total equity Earnings before interest and taxes Interest payments Earnings before interest and taxes Fixed charge + Lease payments = coverage Interest payments + Lease payments An indicator of a company’s debt financing usage The ability to cover interest expenses The ability to cover interest and lease expenses Financial Reporting and Analysis RATIO ANALYSIS PROFITABILITY RATIOS Meaning Gross profit margin = Gross profit Revenue Operating profit margin = Pre-tax margin = Operating income (EBIT) Revenue EBT Revenue Net profit margin = Net income Average total assets Operating return Operating profit (EBIT) on assets (ROA) = Average total assets Return on total capital = Operating profitability (before interest and tax) as a percentage of total revenue Operating profitability (before tax) as a percentage of total revenue Net income Revenue Return on assets (ROA) = Gross profitability as a percentage of total revenue Operating profit (EBIT) Average total capital Net income Return on Equity (RoE) = Average equity Net profitability as a percentage of total revenue Net profitability (excluding interest and taxes) as a percentage of total invested funds Net profitability (including interest and taxes) as a percentage of total invested funds Operating profitability as a percentage of total capital Net profitability as a percentage of total equity Financial Reporting and Analysis RATIO ANALYSIS VALUATION RATIOS Meaning Earnings per Share (EPS) = Price earnings (P/E) ratio = P/E ratio (company wide) = Dividend yield = Net Income - Preferred dividends Outstanding number of common shares Share price Earnings per share (EPS) The price that investors are willing to pay per $1 of earnings Market capitalization Net income Total price that investors are willing to pay for a company's Net income Dividend per share Current share price Retention rate (RR) = Dividend payout = Income earned per 1 common share outstanding Net income - Dividends declared Net income Dividends declared Net income Sustainable growth rate (g) = RR x ROE The "portion "of a share price that is distributed as dividends The "portion" of Net income that is reinvested in the company The "portion" of Net income that is distributed as dividends Equity growth rate RR = Retention rate Financial Reporting and Analysis RATIO ANALYSIS DUPONT ANALYSIS Return on Equity (RoE) Net income Average equity Net profit margin X Net income Revenue Net profit margin Net income EBT X Interest burden EBT EBIT Revenue Average equity Asset turnover X Net income Revenue Tax burden Equity turnover X Operating profit margin EBIT Revenue Revenue Average assets X Asset turnover Revenue Average assets X X Financial leverage ratio Average assets Average equity Financial leverage ratio Average assets Average equity Financial Reporting and Analysis INVENTORIES Where: FIFO = First-in, First-out method LIFO = Last-in, First-out method Ending inventory = Beginning inventory + Purchases - Cost of goods sold (COGS) Cost of goods sold (COGS) = Beginning inventory + Purchases - Ending inventory FIFO inventory = LIFO inventory + LIFO reserve Δ Cash = LIFO reserve x Tax rate Δ Cash = Excess cash saved on the valuation method FIFO retained earnings = LIFO retained earnings + LIFO Reserve x (1 - Tax rate) FIFO COGS = LIFO COGS - (Ending LIFO reserve - Beginning LIFO reserve) Financial Reporting and Analysis LONG-LIVED ASSETS Straight-line depreciation expense = Cost-Salvage (residual) value Useful life Double-declining balance = 2 x (Cost - Accumulated depreciation) Useful life (DDB) depreciation expense Double-declining balance (DDB) depreciation expense = Double the straight-line depreciation rate Cost - Salvage value Units of production x Output units in the period = Life in output units depreciation expense Ending PPE net book value = (Original) Cost – Accumulated depreciation Average age = Accumulated depreciation Annual depreciation expense Total useful life = Historical cost Annual depreciation expense Remaining useful life = Ending PPE net book value Annual depreciation expense Financial Reporting and Analysis INCOME TAXES Income tax expense = Taxes Payable + Δ Deferred Tax Liabilities (DTL) – Δ Deferred Tax Assets (DTA) Effective tax rate = Income tax expense Pre-tax income NON-CURRENT LIABILITIES Interest expense = Market rate at Issuance × Balance sheet value of the liability at the beginning of the period Coupon interest payment = Coupon rate (as per contract) x Par Value www.365careers.com