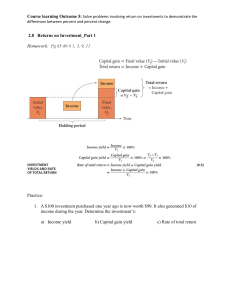

FIN 261 Lecture Notes Ch. 1, 2 1 Investments Nature of Investment Reduce current consumption for greater future consumption Investors’ perspective Maximizing expected welfare Return is good Risk is bad Ex ante risk-return trade-off Portfolios Asset classes Securities Decision Process Top down Bottom up 2 Real versus Financial Assets Real Assets Used to produce good and services Property, plants, equipment, human capital, etc Financial Assets Claims on real assets or claims on real asset income Debt securities, equity, derivatives, mutual fund shares, insurance, etc 3 Financial Markets and Economy Information role of financial markets Are market prices fair? Consumption timing Consumption smoothing over time Risk allocation Risk-return trade off Separation of ownership and management Agency problem Performance based compensation Threat of takeovers Board of directors 4 The Players Businesses Net borrowers Households Net savers Governments Financial intermediaries Commercial banks, investment companies, insurance companies, pension funds, hedge funds, etc Investment bankers specialize in primary market transactions Primary market – newly issued securities offered to public Secondary market – pre-existing securities traded among investors 5 Financial Assets Direct investment Nonmarketable financial assets Money market Treasury bills, Commercial bills Fixed income securities Bonds Equity securities Common stock, Preferred stock Derivatives Options, Futures Indirect investment Mutual funds Closed-end funds / ETFs 6 Money Market A market for the purchase and sale of short term debt instruments highly liquid, relatively low risk Maturities generally less than 12 months Dominated by financial institutions Treasury bill Sold by the US Treasury at a discount from face value Proxy for “risk-free” rate Key role in liquidity management NZ Short term low risk Govt debt issued by Crown Maturities 3, 6, 12 months Traded in parcels of $1m Redeemable at par on maturity 7 Treasury Bill Quotes NZ T-bill US T-bill (wsj.com) 8 T-Bill Yield Investment yield Actual annualized yield face value - market val ue 365 market val ue # of days Discount yield (US) Quoted yield face value - market val ue 360 face value # of days Prices move inversely to yields 9 T-bill Yield Example 90 day $1000 par value US T-bill issued at $990 What is the investment yield? Investment Yield 1000 - 990 365 4.096% p.a. 90 990 This is an annual percentage rate. What is the effective annual rate including interest-on-interest? Effective Yield 1 1000 - 990 990 365 90 1 4.16% p.a. What is the quoted yield? 1000 - 990 360 Discount Yield 4.0% 1000 90 10 A 6-day T-bill is quoted r = 0.04% p.a. How much will it cost you to buy now? # of days Market Value Face Value 1 Discount Yield 360 6 1000 1 0.0004 $999.99 360 A NZ 182-day bill’s investment yield is r = 5.48% p.a. How much will it cost you to buy now? Market Value Face Value 1 Investment Yield 1000 182 1 0.0548 365 # of days 365 $973.40 11 Assume you bought the 182 day bill at a yield of 5.48% p.a. You then sell it after 122 days at a yield of 4% p.a. What was your realised return p.a? Selling price Future Value 1000 $993.47 60 d 1.04 1 r 365 365 Psell 365 Realised Yield (%) 1 100 P 122 buy 993.47 365 1 100 6.17% p.a 973 . 40 122 12 Commercial Bill (NZ) / Paper (US) Document comprising a promise by the borrower to repay the lender Sold at discount from face value A source of short term borrowing and lending for companies, financial institutions, local bodies Maturities: usually 90 days, may range from 30-270 days Example: You wish to borrow so that you repay $500,000 in 90 days You issue (sell) a 90 day bill at $489,593, and promise to repay face value ($500,000) on maturity The buyer of the bill lends $489,593 to you The holder (buyer) usually re-sells (re-discounts) the bill in the market before maturity NZ: If repayment of the bill is “accepted” (guaranteed) by a registered bank it is called a bank bill 13 How they work: If the borrower defaults holders 1 and 2 are contingently liable to repay the face value of the bill. 14 https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-90-day-rate If $1,000 par 90 day bank bills are priced to yield 2.77% p.a. What is the market value of the bill? 1000 / (1+0.0277×90/365) = 993.2162 If market interest rates increased to 4% p.a. how does this affect 90 day bill prices? 15 Other Money Market Securities (Marketable) CD Certificate of deposit from a bank Repurchase agreement Borrower agrees to sell and repurchase government securities Maturity tends to be very short, typically up to 14 days Banker’s acceptance A time draft drawn on a bank by a customer Normally used in international trade. Eurodollars Dollar-denominated deposits held outside U.S. 16 Other Money Market Securities Federal funds Depository institutions must maintain deposits with FRB Federal funds – trading in reserves held on deposit at Federal Reserve Key interest rate LIBOR (London Interbank Offer Rate) Rate at which large banks in London lend to each other Base rate for many loans and derivatives Broker’s calls Call money rate applies for investors buying stock on margin Loan may be “called in” by broker 17 Fixed Income Securities Debt securities which provide a fixed interest (coupon) rate plus repayment of principal at maturity Maturities > 1 year Sold by companies/Govt to raise money Listed debt traded on NZX Debt Market: http://www.nzx.com/markets/nzdx Quoted on a yield to maturity basis The return expected from holding a bond to maturity and re-investing all cash flows Since this return is determined by market prices it also measures investors’ required rate of return 18 Notes and Bonds Quotes directbroking.co.nz wsj.com 19 Bond Price Example Assume a bond has a 10% p.a. coupon, a nominal (par or face) value of $1,000. Interest paid annually on 4/3. Issued on 5/3/08, expires on 4/3/15. At what price should the bond sell today (assume 5/3/12) assuming investors' required rates of return are 6%? PV2012 Cash Flow1 ( 2013) (1 r )1 CF2 ( 2014) (1 r ) 2 CF3 ( 2015) (1 r ) 3 100 100 1100 (1 .06)1 (1 .06) 2 (1 0.06) 3 $1,106. 92 110.69% of face value Now assume a year goes by. It is now 5/3/13 and required rates of return have increased to 7%. 20 Value at 5/3/13 is: PV 100 1100 $1054.24 1.07 (1.07) 2 Total return over the year is: P P interest 1054.24 1106.92 100 t t 1 R 4.27% t P 1106.92 t 1 To calculate the holding period returns we use MARKET PRICES to measure the CHANGE in the VALUE OF THE INVESTMENT (capital gains) and add INTEREST INCOME The investor made the investment EXPECTING a return of 6%. The ACTUAL return was 4.27%! What caused this difference? As interest rates change the realised (actual) return will differ from the expected return. 21 Bond Characteristics Discounts / Premiums Related to coupon rate and yield Zero coupon bond always sells at a discount STRIPS Call / Put provision Gives issuer (buyer) to buy (sell) back Can be thought of as a combination of a plain bond and option Security 22 Types of Bonds Treasuries Notes and bonds TIPS (Treasury Inflation-Protected Securities) Federal Agency Securities Mortgage-backed securities Municipal bonds (‘munis’) Political entities other than the federal government Exempt from federal taxes Taxable equivalent yield = munis yield / (1 – marginal tax rate) 23 Corporate Bonds Default risk Credit ratings Security Debentures have no collateral Options can be attached Callable bond Convertible bond International bonds Eurobond Denominated in a foreign currency – e.g., Euro-dollar, Euro-yen Yankee bond, Samurai bond denominated in local currencies 24 Equity Securities Common stock Ownership interest (residual claim) of corporation Limited liability Voting rights Distribution Dividends – cash, stock (splits) Repurchase 25 Equity Securities Preferred stock Known (fixed or variable-rate) dividend Seniority between bonds and common stock Must be paid before common stock Often nonvoting Depository Receipts ADR (American Depository Receipts) Certificates traded in the U.S. representing ownership in foreign security 26 Stock and Bond Market Indexes Stock market index is a portfolio of shares used to measure the market’s performance, especially over time as a benchmark to assess portfolio performance to develop index investment funds Different ways of constructing indices Price weighted index Value weighted index Equal weighted index 27 Constructing an Index - Example Company A Company B No. of Shares 100m 10m Price at start $2 $1 Price at end $2.20 $1.50 Return 10% 50% Assume we have an index comprised of two companies no dividends are paid by either company the (arbitrary) starting index is 100 Price Weighted Index Assumes you hold an equal number of shares of each company in the index Starting dollar value of the portfolio $2 + $1 = $3 Set an arbitrary index level, say 100 for $3 Ending value of the portfolio $2.20 + $1.50 = $3.70 Return is $3.70/$3 -1 = 23.3%. Closing index is 100×($3.70/$3) = 123.3 Or the return on index = 10%×2/3 + 50%×1/3 = 23.3% Influence of a stock return on the index return is determined by its price 1% return on high priced stocks more influential $1 change in any stock has the same influence on the index level Index must be adjusted for any capital changes made during the period which affect share price share splits, bonus issues, rights issues For example, an index based on prices will drop after a share split, even though nothing economic happened As the index should reflect only changes in share price rather than capital structure, the index value must be adjusted so that it is not affected by the split Divisor an arbitrary number that is first defined when an index is first published. Initial use is to divide the total value of the index to produce an initial index value such as the number '100'. For example, the initial divisor for the price weighted index above is 0.03. Divisor is adjusted to ensure continuity Price-weighted index: stock splits, dividend payment, bonus issues, component change Dow Jones Industrial Average (DJIA) 30 stocks Divisor Adjustment Example Suppose that Company A splits its stock 2-for-1 right at the end of the period. Then the divisor adjusts to keep the value of index constant. Before the split, Index = (2.2 + 1.5) / 0.03 = 123.33 After the split, the divisor, d, would adjust to yield Index = 123.33 = (1.1 + 1.5) / d d = 0.0211 We keep 1 share each in our portfolio before and after the split Weights will change while keeping the same index level Value Weighted Index Prices are weighted by the value of shares on issue Value at start $2(100m) + $1(10m) = $210m Value at end $2.2(100m)+ $1.5(10m)=$235m Closing index is 100× ($235/$210) = 111.9 Or return = 10%×200/210 + 50%×10/210 = 11.9% Initial divisor = 2.1m Divisor adjusts for stock dividends, secondary offerings, and etc Influence of a company’s return on the index return is based on its relative total market value Gives more weight to large companies Many indices are now based on freely floating shares NZX, S&P Value Weighted Index Examples NZX, S&P, NASDAQ, Russell indices NZX 10 Equal Weighted Index Each share in the index is given equal weight an equal dollar amount (say $1,000) is invested in each share Thus we buy 500 shares of A @ $2 = $1,000 1000 shares of B @ $1 = $1,000 Value at end is $2.2(500)+ $1.5(1000)=$2600 Closing index is 100×($2600/$2000) = 130 Return is 2600/2000 - 1 = 30% Or Return = 10% × Needs rebalancing Value Line Index 1 2 1 2 + 50% × = 30% NZSX Indexes The main share price index is the NZSX 50 A gross index comprising the largest 50 companies based on market capitalisation using free float shares Other indices include: the top 10 domestic companies, medium sized companies, small companies, all listed companies science and technology companies https://www.nzx.com/markets/indices Bond Indexes Merryl Lynch, Barclays, and Salomon Smith Barney Thin trading Bonds trade infrequently Components that are thinly traded create lumpy movements in the index, distorting true index values Exclusion of infrequently traded components may result in an index that is less representative of the underlying market Some NZ stocks 37 Derivative Securities Options Call – right to buy at a pre-determined price Put – right to sell at a pre-determined price Can be used in variety of strategies Futures The holder has an obligation to buy/sell an asset in the future at a price specified now 38 Are the following assets real or financial? a. Patents b. Lease obligations c. Customer goodwill d. A college education e. A $5 bill 39 Table 1.1: Balance Sheet of US Households 40 Structure of a bond’s cash flows A typical bond’s cash flows $1,025 Coupon rate = ? Par value = ? Bond price = ? 0 $25 $25 1 2 $25 $25 $25 $25 $25 $25 $25 9 10 annual time periods $1,000 41 Example: Municipal Bond A municipal bond carries a yield to maturity of 6.75% and is trading at par. What would be the taxable equivalent yield of this bond to a taxpayer in a 35% tax bracket? Taxable equivalent yield = munis yield / (1 – marginal tax rate) Taxable equivalent yield = 6.75% 1−35% = 10.385% 42 NZ TOP 10 ETF (TNZ) https://smartshares.co.nz/types-of-funds/new-zealand-shares/tnz 43