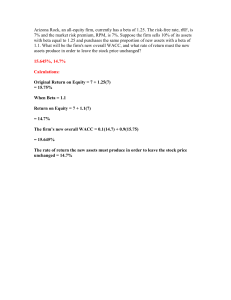

1. Describe the tasks and priorities of a modern corporate finance service Every single decision made in a business has financial implications, and any decision that involves the use of money is a corporate financial decision. t is the discipline of finance that deals with financing, capital structuring, and investment decisions. It is primarily concerned with maximising shareholder value through long and short-term financial planning and the implementation of various strategies. Corporate finance is split into three sub-sections: capital budgeting, capital structure working capital management. 2. What does the Beta coefficient measure? Beta (β) is a measure of the volatility or systematic risk of a security or portfolio compared to the market as a whole (usually the S&P 500). Stocks with betas higher than 1.0 can be interpreted as more volatile than the S&P 500. 3. What are the constituents of capital invested and capital employed and what is the economic meaning of these concepts? Capital employed is the total amount of capital used for the acquisition of profits by a firm or project. Capital employed can also refer to the value of all the assets used by a company to generate earnings. Capital employed is calculated by taking total assets from the balance sheet and subtracting current liabilities, which are short-term financial obligations. Invested capital is the investment made by both shareholders and debtholders in a company. When a company needs capital to expand, it can obtain it either by selling stock shares or by issuing bonds. For a company, invested capital is a source of funding that enables them to take on new opportunities such as expansion. It has two functions within a company. First, it is used to purchase fixed assets such as land, building, or equipment. Secondly, it is used to cover dayto-day operating expenses such as paying for inventory or paying employee salaries. Invested Capital= Net Working Capital+ PPE+ Goodwill and intangibles Where Net working capital = current operating assets = Non-interest bearing current labilities Goodwill and intangibles are items such as brand reputation, copyrights, and proprietary technology computer software 4. Should you discount even if there is no inflation and no risk? Why? Yes, because discounting is used to factor in an interest rate which remunerates the forgoing of immediate spending. Discounting is thus unrelated to inflation or risk. 5. What is the difference between EBITDA and EBIT in terms of creating value for owners of a company? The EBITDA indicator is used to determine the company's ability to service debt, that is, this indicator, combined with the net profit indicator, served as a source of information about how much interest payments the company can provide in the near future. EBIT measures the profit a company generates from its operations making it synonymous with operating profit. By ignoring taxes and interest expense, EBIT focuses solely on a company's ability to generate earnings from operations, ignoring variables such as the tax burden and capital structure. EBIT is an especially useful metric because it helps to identify a company's ability to generate enough earnings to be profitable, pay down debt, and fund ongoing operations. 6. Why does the financial expense (interests and principal debt)/EBITDA ratio play such a fundamental role in financial analysis? If there is a debt, we will repay it at the expense of EBITDA. EBITDA = both principal debt and interest due. EBITDA is the money that the company has. EBITDA means a resource for closing interest and principal. That is why the amount of interest and principal is compared with EBITDA. And this plays a key role in many financial analyses. That is, we have enough money that the company generates to pay the principal and interest. 7. Indicate the components of the cash flow, indicate its differences from the company's net profit, explain the features of cash flow and net profit from the point of view of the interests of owners of a company. The three main components of a cash flow statement are cash flow from operations, cash flow from investing, and cash flow from financing. The key difference between cash flow and profit is while profit indicates the amount of money left over after all expenses have been paid, cash flow indicates the net flow of cash into and out of a business. Features of CF: Analyzing a company's cash-flow provides critical information about its financial health, business activities, and reported earnings. Based on the analysis, future money flows are projected. Consequently, financial analysts plan short-term goals, long-term goals, working capital, and the optimum cash level required for business operations. Features of Net Profit: Net profit reveals the success of a business and its ability to repay debt and reinvest. 8. What difference is there between sales in a financial year and operating receipts over the same period? Sales are the exchange of products or services for money, either paid for now or in the future. When your business provides a product or service to a customer in exchange for financial consideration, the business has made a sale and can report that sale on its financial statements. Receipts are the amount of cash a business takes in during any one accounting period, regardless of whether the money came from a sale or other source, according to IRS rules. Receipts are cash sales, as well as money received in a customer's account. Receipts also include any cash received in the business from any source, including investment interest, royalties, leases, a loan or credit line proceeds or funding from investors. Cash receipts are shown on the cash flow statement, which helps show how much money is available for the business to pay its financial obligations. 9. Among the following different flows, which will be appropriated by both shareholders and lenders: operating receipts, operating cash flow, free cash flows? Who has priority in each case, shareholders or lenders? Why? Free cash flows, since all operating or investment outlays have been paid. The lenders because of contractual agreement. 10. Does sale of goods on credit affect the company’s net income and the company’s cash position? Why? Selling on credit may boost revenue and income, but it offers no actual cash inflow. In the short term, it is acceptable, but in the long term, it can cause the company to run short on cash and have to take on other liabilities to fund operations. 11. What does the Capital Asset Pricing Model (CAPM) mean? The Capital Asset Pricing Model (CAPM) describes the relationship between systematic risk, or the general perils of investing, and expected return for assets, particularly stocks. It is a finance model that establishes a linear relationship between the required return on an investment and risk. The model is based on the relationship between an asset's beta, the risk-free rate (typically the Treasury bill rate), and the equity risk premium, or the expected return on the market minus the risk-free rate. 12. Do equipment valuation methods influence on the company’s net income and the company’s cash position? Equipment valuation methods influence the company’s net income. Equipment valuation methods don’t influence the company’s cash position. 13. What Is the Weighted Average Cost of Capital (WACC)? The weighted average cost of capital (WACC) is the average rate that a business pays to finance its assets. It is calculated by averaging the rate of all of the company's sources of capital (both debt and equity), weighted by the proportion of each component. 14. What is the difference between liabilities and sources of funds? Sources of funds include shareholders’equity (which does not have to be repaid and is consequently not a liability) and liabilities (which sooner or later have to be repaid). 15. In what calculations is the Weighted Average Cost of Capital (WACC) used, and why? Why is WACC compared to ROA, and what do the results of such comparisons say if WACC is greater or less than ROA? The WACC is used to calculate the discounted present value of cash flows when they are valued without funding. When WACC exceeds ROA, this indicates a decrease in economic value added and an overall loss in company value, and if WACC is less than ROA, this indicates that assets are being used efficiently and the company's value is growing. 16. How to calculate capital employed and capital invested? Capital employed=Total assets−Current liabilities=Equity + Non current liabilities Capital Invested=Net Working Capital + Net Fixed Assets + Net Intangible Assets 17. What are the advantages and disadvantages of increasing the stock options granted to CEOs? Advantages: Ties the employee's financial reward to the success of the business, aligning the employee's self-interest with the company founder's self-interest Does not generally involve company cash and is therefore an attractive compensation technique Allows the Company to better attract and retain key employees Disadvantages: Dilution can be very costly to shareholder over the long run. It might be difficult to evaluate stock options. Stock options can result in high levels of compensation of executives for mediocre business results. An individual employee must rely on the collective output their co-workers and management in order to receive a bonus. 18. How to calculate working capital of a company? Working capital=Current assets-Current liabilities 19. What differences are there between cash flow from operating activities and operating cash flow? Unlike operating cash flow, cash flow from operating activities encompasses not only operations but also financial expense, tax and some exceptional items. 20. Will repayment of a loan (principal and interests) always be recorded on the income statement? Will it always be recorded under a cash item? Only the interest portion of a loan payment will appear in income statement as an Interest Expense. The principal payment of loan will not be included in business' income statement. Yes it always be recorded under a cash item, because debts are repaid in cash. 21. What is a breakeven point? What are the types of breakeven points? What can breakeven analysis be used for? The break-even point is the point at which total cost and total revenue are equal. Three different breakeven points may be calculated: operating breakeven, which is a function of the company’s fixed and variable production costs. It determines the stability of operating activities, but may lead to financing costs being overlooked; financial breakeven, which takes into account the interest expense incurred by the company, but not its cost of equity; total breakeven, which takes into account both interest expense and the net profit required by shareholders. As a result, it takes into account all the returns required by all the company’s providers of funds. Break-even analysis is a way to find out the minimum sales volume so that a business does not suffer losses. 22. Does the inflation-related increase in the nominal value of an asset appear on the income statement? No, because of the principle of prudence, which mentions that income and assets are not overstated in financial statements. 23. What are the types of breakeven points? What does each of them mean? Three different breakeven points may be calculated: operating breakeven, which is a function of the company’s fixed and variable production costs. It determines the stability of operating activities, but may lead to financing costs being overlooked; financial breakeven, which takes into account the interest expense incurred by the company, but not its cost of equity; total breakeven, which takes into account both interest expense and the net profit required by shareholders. As a result, it takes into account all the returns required by all the company’s providers of funds. 24. What are the accounting items corresponding to additions to wealth for shareholders, lenders and the State? Financial expense - for lenders. Net income - shareholders Corporate income tax - for State 25. What is a contribution margin? What does increase and decrease of it mean? The contribution margin shows how much additional revenue is generated by making each additional unit product after the company has reached the breakeven point. If the product's contribution margin is negative, the company is losing money with each unit produced and should either abandon the product or raise prices. If a product has a positive contribution margin, then that product is worth keeping. 26. Define a company’s book value Book value is the net value of a firm's assets found on its balance sheet, and it is roughly equal to the total amount all shareholders would get if they liquidated the company. 27. What is economic value added? How can this indicator be calculated? What does this indicator mean? Economic value added (EVA) is a measure of a company's financial performance based on the residual wealth calculated by deducting its cost of capital from its operating profit, adjusted for taxes on a cash basis. Economic Value Added=Net Operating Profit After Tax - (Capital Invested × WACC) It is used to measure the value a company generates from funds invested in it. If a company's EVA is negative, it means the company is not generating value from the funds invested into the business. Conversely, a positive EVA shows a company is producing value from the funds invested in it. 28. In your view, should short-term debt be separated out from medium- to long-term debt on the cash flow statement? Why? Definitely not, short-term debt should not be separated from medium-term and long-term debt in the cash flow statement, it helps you keep an idea of the future state of your business. 29. What indicators characterizing the activity of the company indicate the creation of value in terms of its economy, market and accounting? Why? The tools used for measuring creation of value can be classified under three headings: Economic tools, which yield the best results since they factor in returns required by investors (the weighted average cost of capital) and do not depend directly on the sometimes erratic price movements of markets. NPV is the most important of these.EVA, the popular term for economic profit, measures how much the shareholder has increased his wealth over and above standard remuneration. However, EVA has the drawback of being restricted to the financial period in question; EVA can thus be manipulated to yield maximum results in one period at the expense of subsequent periods. Market tools, which measure MVA (Market Value Added), or the difference between the company’s enterprise value, its book value,and TSR (Total Shareholder Returns). TSR is the rate of shareholder returns given the increase in the value of the share and the dividends paid out. These market tools are only useful over the medium term, because to be meaningful they should avoid the market fluctuations that can distort economic reality. Accounting indicators, which have the main drawback of being designed for accounting purposes; i.e., they do not factor in risk or return on equity. They include Earnings Per Share (EPS) linked to the value of the share by the Price/ Earnings ratio (P/E), shareholders’ equity linked to the value of the share by the Price/Book Ratio (PBR), accounting profitability indicators (shareholders’ equity, Return On Equity – ROE, Return On Capital Employed – ROCE) to be compared with the cost of equity (or the Weighted Average Cost of Capital, WACC). 30. On what should you base a choice between two equal discounted values? If the present values are equal, it makes no difference. 31. What is the beta coefficient of a company and what does its value depend on? Beta coefficient can measure the volatility of an individual stock compared to the systematic risk of the entire market. The beta coefficient depends on two main parameters that work together: - the correlation of asset price changes (together with market changes). - the relative volatility of the selected instrument in relation to the market where it rotates. 32. Why can the internal rate of return not be used for choosing between two investments? Because it does not measure the value created. 33. What is enterprise value? Why does it matter? Enterprise value (EV) is the total value of a company, defined in terms of its financing. It includes both the current share price (market capitalization) and the cost to pay off debt (net debt, or debt minus cash). Combining these two figures helps establish the company’s enterprise value, indicating the neighborhood you need to be in to buy the company. Enterprise Value = Market Cap + Debt – Cash or Enterprise value = Value of net debt + Equity value Businesses use enterprise value to gauge the cost of acquiring a company, particularly when they have different capital structures. Because EV accounts for more than just its outstanding by adding debt and subtracting cash from the cost, it allows for companies to determine how much a company is worth. 34. What is discounting? Why should we discount? What is the discount factor equal to (formula)? Discounting is the process of determining the present value of a future payment or stream of payments. Discounted cash flow helps investors evaluate how much money goes into the investment, the timing of when that money is spent, how much money the investment generates, and when the investor can access the funds from the investment. Discount factor = 1/(1+Discount rate)^Period number 35. What is a market approach to business valuation and what multiples are used? What are the applicable assessment methods? What are the pros and cons of the market approach? The market approach is a method of determining the value of business based on the selling price of similar business. Within the market approach, there are two primary methods: the guideline public company method (based on valuation multiples derived from publicly traded companies in similar industries), and the guideline transactions method (based on valuation multiples derived primarily from merger & acquisition transactions involving companies similar to the subject company) Common valuation multiples include EV (enterprise value) to sales, EV to EBITDA (earnings before interest, taxes, depreciation, and amortization), and Price to Earnings (P/E) Advantages Based on real market data; Reflects existing sales and purchase practices; Takes into account the influence of industry factors on the company's share price Disadvantages Insufficiently clearly characterizes the features of organizational, technical, financial preparation of the enterprise Only retrospective information is taken into account; Does not take into account the future expectations of investors 36. On the same loan, is the total amount of interest payable more if the loan is repaid in fixed annual instalments, by constant amortisation or on maturity? On maturity, because the principal is lent in full over the whole period 37. What is an income approach to business valuation? What are the applicable assessment methods? What are the pros and cons of the income approach? The income approach measures the future economic benefits that the company can generate for a business owner or investor. There are two income-based approaches that are primarily used when valuing a business, the Capitalization of CF Method and the DCF Method. The Capitalization of Cash Flow Method is most often used when a company is expected to have a relatively stable level of margins and growth in the future. The DCF method is more flexible than the Capitalization CF Method and allows for variation in margins, growth rates, debt repayments and other items in future years that may not remain static. As a result, the Capitalization of Cash Flow Method is typically applied more often when valuing mature companies with modest future growth expectations. The Discounted Cash Flow Method is used when future growth rates or margins are expected to vary or when modeling the impact of debt repayments in future years. Advantages Takes into account future changes in income, expenses; Takes into account the level of risk (through the discount rate); Takes into account the interests of the investor Disadvantages There are difficulties in predicting future results and costs; There may be several rates of return, which makes it difficult to make a decision; Does not take into account the state of the market; 38. What Is Net Present Value (NPV)? NPV demonstrates the expected future revenue of the project minus its initial cost. NPV allows you to compare current money with future money, which will cost less due to inflation. 39. What is an asset approach to business valuation? What are the applicable assessment methods? What are the pros and cons of the asset approach? Asset-based valuation is a form of valuation in business that focuses on the value of a company’s assets or the fair market value of its total assets after deducting liabilities. Asset-based valuation is a form of valuation in business that focuses on the value of a company’s assets or the fair market value of its total assets after deducting liabilities. There are 2 approaches to calculate an asset-based valuation: Going Concern: Under this approach, the business needs to list out its net balance sheet value of its assets. The value of the company’s assets less liabilities is then subtracted. Liquidation Value: In case the business is in the process of liquidating, then it must quickly calculate its amount of net cash. This is the cash received as soon as the assets are sold and the liabilities are repaid. It tends to be less than market value. 40. What Is Enterprise Value (EV)? Enterprise Value is the entire value of a firm equal to its equity value, plus net debt, plus any minority interest 41. Advantages and disadvantages of different business valuation approaches Income approach Advantages Takes into account future changes in income, expenses; Takes into account the level of risk (through the discount rate); Takes into account the interests of the investor Disadvantages There are difficulties in predicting future results and costs; There may be several rates of return, which makes it difficult to make a decision; Does not take into account the state of the market; Market approach Advantages Based on real market data; Reflects existing sales and purchase practices; Takes into account the influence of industry factors on the company's share price Disadvantages Insufficiently clearly characterizes the features of organizational, technical, financial preparation of the enterprise Only retrospective information is taken into account; Does not take into account the future expectations of investors Cost approach Advantages Takes into account the influence of production and economic factors on the change in the value of assets; Gives an assessment of the level of technology development, taking into account the degree of depreciation of assets; Calculations are based on financial and accounting documents, so the results of the assessment are more justified Disadvantages Reflects past value; Does not take into account the market situation at the valuation date, Does not take into account the prospects for the development of the enterprise; Does not take into account risks; There are no links with the present and future results of the company's activities 42. Upon what is the Beta coefficient dependent? It depends on the structure of the company's operating costs, the financial structure, and the rate of profit growth. It depends on the information policy of the company, because depending on how fully we give information to the market, the market evaluates us that way. That is, Beta consists of the assessment of experts who have certain information, and this information includes the structures of operating costs, financial structure, profit growth rate and information policy (because this is the company's information about how it is going to develop). Beta evaluates both the past and the future, the past can be estimated from actual data, and the future only from information from the company. 43. What does the Beta coefficient measure? The Beta coefficient is a measure of sensitivity or correlation of a security or an investment portfolio to movements in the overall market. 44. What are systematic and non-systematic risks? How do they differ from each other? Systematic risk is the underlying risk that affects the entire market. Unsystematic risk is a risk specific to a company or industry, while systematic risk is the risk tied to the broader market. Unlike systematic risks, unsystematic risks can be controlled, minimized, and even avoided by an organization and systematic risks affect the financial market as a whole, whereas unsystematic risks are unique to a specific company or investment. 45. What is the terminal value? What are the methods of its calculation and application? Terminal value (TV) is the value of an asset, business, or project beyond the forecasted period when future cash flows can be estimated. Terminal value assumes a business will grow at a set growth rate forever after the forecast period. Terminal value often comprises a large percentage of the total assessed value. Analysts use the discounted cash flow model (DCF) to calculate the total value of a business. The forecast period and terminal value are both integral components of DCF. The two most common methods for calculating terminal value are perpetual growth (Gordon Growth Model) and exit multiple. The perpetual growth method assumes that a business will generate cash flows at a constant rate forever, while the exit multiple method assumes that a business will be sold. Most companies do not assume they will stop operations after a few years. They expect business will continue forever (or at least a very long time). Terminal value is an attempt to anticipate a company's future value and apply it to present prices through discounting. 46. It has been said that a solid financial structure was a guarantee of freedom and independence for a company. Is this true? Are there any exceptions? Yes, except when the share price is undervalued, in which case there is a risk of takeover 47. What are the Payback Methods? Explain the difference between them The payback method evaluates how long it will take to “pay back” or recover the initial investment. The main difference between the two methods is that the discounted payback period takes into account the time value of the factor while the regular payback ignores it. Under the regular payback period, the cash flows generated by a project are used at their face value. 48. Assess the liquidity of the following assets in order of decreasing liquidity: plant, unlisted securities, listed securities, head office building located in the centre of a large city, ships and aircraft, commercial papers, raw materials inventories, work-in-progress inventories? In order of decreasing liquidity: listed securities, commercial paper, raw materials inventories, head office, unlisted securities, ships and aircraft, work-in-progress inventories, plant. 49. How to reconcile the results of the three approaches to business valuation? The cost of a business in each of the approaches may be approximately the same, or it may differ. After evaluating the three approaches, we need to analyze the pros and cons of each approach for our company and give each approach a specific weight. For example, if a company has many expensive assets and average or poor performance, more weight could be given to the cost approach. If a company has a steadily growing income for several years, it is profitable. And if there are many similar companies on the market and data on them - comparative. 50. On what should you base a choice between two equal discounted values? If the present value are equal, it makes no difference 51. Why can the internal rate of return not be used for choosing between two investments? It ignores the actual dollar value of comparable investments. It does not compare the holding periods of like investments. It does not account for eliminating negative cash flows. It provides no consideration for the reinvestment of positive cash flows. 52. The Beta coefficient measures the specific risk of a security. True or false? Why? True, Beta coefficient measures the volatility of a security compared to the market as a whole. Beta (β), primarily used in the capital asset pricing model CAPM, is a measure of the volatility–or systematic risk–of a security or portfolio compared to the market as a whole.

![FORM 0-12 [See rule of Schedule III]](http://s2.studylib.net/store/data/016947431_1-7cec8d25909fd4c03ae79ab6cc412f8e-300x300.png)