CHAPTER 1: INTRODUCTION AND OVERVIEW

Research in accounting – solving problems,

investigating relationships and building a body

of knowledge.

Bennet (1991) four basic levels of research

o Description – collection and reporting

of data related to what is, or was, the

case. Include standard deviations of

individual variables, correlations

between pairs of variables.

o Classification – still descriptive but

easing the reporting process, and

highlighting similarities and clustering

through grouping and classifying.

o Explanation – an attempt to make

sense of behaviors by explaining the

relationships observed and attributing

causality based on some appropriate

theory.

o Prediction – going beyond the

understanding and explaining of the

prior stage, to model observations in a

way that allows testable predictions to

be made of unknown events.

Two major processes of reasoning:

o Deductive (theory to observation) –

starts with theory and proceeds to

generate specific predictions which

follow from its application. Predictions

can be verified.

o Inductive (observation to theory) –

starts with specific observations (data)

from which theories can be generated;

a generalizable pattern may emerge

from further observations and repeated

testing for compliance. Hawking (1998)

notes that generalizations made can

never be regarded as ‘certain’ since just

one contrary instance can cause them

to be overturned.

Strict division of reasoning processes is not

always helpful because interdependencies

always exist

o Induction will usually imply some

knowledge of theory in order to select

the data to be observe.

o Deduction will be dependent on the

selection of the initial hypotheses for

testing.

New approach

1. Interpretive perspective – human

actions are the result of external

influences. Active participation rather

than detached observation.

2. Critical perspective – focusing on the

ownership of knowledge and the

associated social, economic and

political implications.

Popper (1959) – genuine test of a theory is an

attempt to falsify it or refute it.

Three fundamental criteria exist to judge

whether theory fits observation

1. Co-variation – even where no causality

exists we would expect the two

variables to move together so that a

high degree of correlation exists

between the two variables. Where

there is no co-variation it will be

difficult to establish a causal link.

2. Cause prior to effect – if a causal link is

to be established then the ‘causal

event’ should occur before the ‘effect

event’. The sequence of events can

therefore help to establish an

explanatory direction.

3. Absence of plausible rival hypotheses –

seeks to eliminate alternative

explanations of the events as being

implausible.

Critique published articles

1. Why is this article

interesting/important?

2. Are the outcomes important?

3. What motivates the authors to write

this article now?

4. What is the research

problem/question?

5. What theory or theoretical framework

underpins the research?

6. What are the key motivating literatures

on which the study depends?

7. Which research method has been

chosen?

8. How does the sample been selected?

9. How have questions of validity been

addressed?

10. How have the results been analyzed?

11. Are the conclusions and

recommendations consisted with the

findings?

CHAPTER 2: DEVELOPING THE RESEARCH IDEA

Research sequence

1. Identify broad area

2. Select topic

3. Decide approach

4. Formulate plan

5. Collect information

6. Analyze data

7. Present findings

The positivist approach

1. Problem

2. Literature review

3. Hypothesis development

4. Method

5. Results

Alternative research methods

Archival research Hypothesis testing using

Laboratory

standard

experiments

instruments/method/controls

Survey method

Quantitative data

Deductive positivism

Action research

Quasi-research methods

Field-based

surveys/interviews

Field research

Subjective accounts ‘inside’

situations

No a priori hypotheses

Qualitative data

Ethnographic

method

Research proposal elements

o Title

o Abstract

o Issues

o Objectives

o Literature

o Method

o Benefits

Basic conceptual scheme – provides a powerful

tool for the examination of causal relationship

in a positivist environment.

Dependent variables – one or more outcome

variables whose value may be influenced by a

number (independent) explanatory factors.

CHAPTER 3: THEORY, LITERATURE AND HYPOTHESES

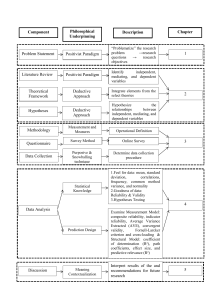

Three characteristics of accounting research

o Theory

o Reliability

o Validity

Expanded

o Good theory

o Reliability

o Construct validity

o Internal validity

o External validity

Theory – network of hypotheses or an allembracing notion that underpins one or more

hypotheses

Hypotheses – supposed relationships, possibly

causal links, between two or more concepts or

variables. A hypothesis should be testable, but

it may not be directly so if it comprises a

number of abstract concepts.

Concepts – abstract ideas, not directly

observable or measurable which must first be

operationalized in some way to provide

measurable indicators. Either by identifying a

variable that is an adequate substitute for the

concept or by developing a construct to provide

a new measure of the concept.

Constructs – indirect measures of concepts

usually generated in the form of multi-item

questions. The sum of a set of valid and reliable

responses to the construct provides a measure

of the concept.

Variables – observable items which can assume

different values. Values can be measured either

directly or indirectly through the use of proxy

(substitute) variables.

o Independent – explanatory

o Dependent – are explained by the

independent variables

o Moderating – have a conditional

influence

o Intervening – with an influence,

potentially spurious, that needs to be

controlled

Reliability – establishes the consistency of a

research instrument in that the results it

achieves should be similar in similar

circumstances.

Validity – measures the degree to which our

research achieves what it sets out to do.

With internal validity – able to eliminate rival

hypotheses with confidence because we can

specify causal relationships; we know what is

causing what because we are controlling for all

other influential factors.

No external validity – they cannot be

generalized to the ‘real world’ because they

only apply in the laboratory.

Fundamental trade-off: we may have to

compromise loss of internal validity (loosening

the confidence we have in the relationships) in

order to increase external validity (and realism).

Fundamental distinction underpinning

accounting theory

o Normative theory – of what ought to be

o Positive theory – of what is or will be

Economics

Early researchers:

0

0