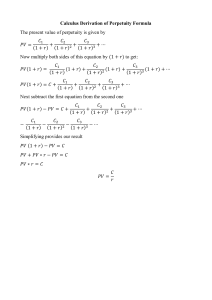

NPV and Time Value of Money: Finance Essentials

advertisement