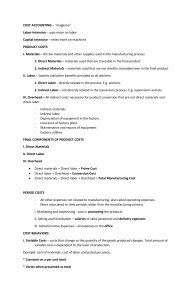

Classification of Cost Measuring costs requires judgment. That is why there are alternative ways in which costs can be defined and classified Different companies or sometimes even different departments within the same company may define and classify costs differently. 1. Costs in Relation to the Product a. Manufacturing costs (Production costs) or Product costs al. Under Normal Costs System: 1. Direct Materials 2. Direct Labor 3. Factory Overhead Applied (predetermined or estimated) Under normal costs system, the actual incurrence of indirect materials, indirect labor and other production costs (or factory costs) are recorded to Factory Overhead- Control. Product costs are classified into two: 1. Prime Cost = Direct Materials + Direct Labor 2. Conversion Cost = Direct Labor + Factory Overhead a2 Under Actual Cost System 1. Materials 2. Labor 3. Factory Overhead (other production costs) b. Non-manufacturing costs or Period costs 1. Administrative or General expenses 2. Selling or Marketing expenses II. Cost in Relation to Volume of Production a. Variable costs b. Fixed costs c. Semi-variable or Semi-fixed costs III. Cost in Relation to Types of Inventory a. Materials Inventory b. Work-in-process Inventory c. Finished Goods Inventory IV. Cost in Relation to Traceability to Cost Objective a. Direct costs b. Indirect costs V. Cost in Relation to their nature as common or joint a. Common costs b. Joint costs VI. Cost in Relation to the Nature of Expenditures a. Capital expenditures b. Revenue expenditures VII Cost in Relation to Period of Incurrence a. Historical costs b. Future costs VIII. Cost in Relation to Managerial Influence a. Controllable costs b. Non-controllable costs