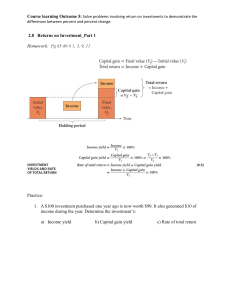

Unit 5: Money Markets Lecture 2: Money Markets – Worked Examples Yield Instruments Money Markets Yield Instruments Yield (or Interest Add-On) Instruments: • Fixed Deposits • Negotiable Certificates of Deposit (NCD) • Repurchase agreements 3 Money Markets Yield Instruments Example 1: Fixed Deposit Calculate the interest earned on a fixed deposit from 29/01/10 to 12/04/10 at a rate of 11.25% and an amount of R10 million d i Interest earned = PV × × 100 B 11.25 73 = 10,000,000 × × 100 365 = R 225,000 4 Money Markets Yield Instruments Example 1: NCD (Primary Market) What amount of money is repaid to an investor who purchased an NCD with a face value of R10 million at a coupon rate of 12.18% for a period of 181 days? c d im × MV = N × 1 + 100 B 12.18 181 = 10,000,000 × 1 + × 100 365 = R10,603,994.52 5 Money Markets Yield Instruments Example 2: NCD (Secondary Market) You invest in a secondary market NCD with a face value of R5,000,000. The NCD was issued at a coupon of 12.25% for 270 days and is currently trading at a yield of 11.85%, with 92 days left to maturity. What amount of money did you invest? c d im MV = N × 1 + × 100 B 12.25 270 = 5,000,000 × 1 + × 100 365 = R5,453,082.19 MV P = i y d sm 1 + × 100 B 5,453,082.19 = 11.85 92 × 1 + 100 365 = R5,294,930.59 6 Money Markets Yield Instruments Example 3: NCD (Primary and Secondary Market) Bank A issues a NCD, with a face value of R10m, issued for a period of 91 days at a rate of 11.5% p.a. This is a PRIMARY MARKET calculation Bank B now purchases the NCD at 10.95%. There are 30 days left to maturity • What did Bank B invest? (secondary trade) This part is the SECONDARY MARKET calculation 7 Money Markets Yield Instruments Example 3: NCD (Primary and Secondary Market) Bank A issues a NCD, with a face value of R10m, issued for a period of 91 days at a rate of 11.5% p.a. This is a PRIMARY MARKET calculation How did we calculate the MV of this instrument (in primary market)? 91 𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀 𝑉𝑉𝑉𝑉𝑉𝑉𝑉𝑉𝑉𝑉 = 10000000 1 + 0.115 x 365 Using your financial calculator: = 𝑅𝑅𝑅𝑅 286 712.33 N=1; PV = -10,000,000’; I% = 91/365 x 11.5; PMT = 0 FV = 10 286 712.33 = MV (Maturity Value) 8 Money Markets Yield Instruments Example 3: NCD (Primary and Secondary Market) How do we calculate what BANK B invested? Calculation: 𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃 = 10000000 1 + 0.115x 1 + (0.1095x 91 365 30 ) 365 RECOGNISE THIS? 𝑅𝑅10 286 712.33 = 𝑅𝑅𝑅𝑅 194 957.71 Step 1: N=1; I%=91/365x11.5; PV = -10000000; PMT = 0 FV = 10 286 712.33 Step 2: I% = 30/365 x 10.95 PV = 10 194 957.71 9 Money Markets Yield Instruments Example 4: NCD (Primary Market) All NCDs have interest payable at maturity and are traded on a yield basis Amount invested / Face Value = R 1 000 000 Issue date = 1 April 2008 Maturity date = 31 July 2008 d = 121 days 𝒄𝒄𝒚𝒚 = 12% 10 Money Markets Yield Instruments Example 4: NCD (Primary Market) 121 𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀𝑀 𝑉𝑉𝑉𝑉𝑉𝑉𝑉𝑉𝑉𝑉 = 1000000 1 + 0.12 x 365 = 𝑅𝑅𝑅 039 780.82 Using your financial calculator: N=1; PV = -1000000’; I% = 121/365 x 12; PMT = 0 FV = 1 039 780.82 = MV (Maturity Value) 11 Money Markets Money Market Instruments Example 4 (cont.): NCD (Secondary Market) MV = R 1 039 780.22 Contract date = 29 June 2008 Maturity date = 31 July 2008 d = 32 days 𝒊𝒊𝒚𝒚 = 12% 12 Money Markets Yield Instruments Example 4 (cont.): NCD (Secondary Market) 1039780.82 𝑆𝑆𝑆𝑆𝑆𝑆𝑆𝑆 𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃 = 32 1 + 0.12 x 365 = 𝑅𝑅𝑅 028 955.64 Using your financial calculator: N=1; I% = 32/365 x 12; PMT = 0; FV=1039780.82 PV = 1 028 955.64 = Price / Sale Proceeds 13 Money Markets Yield Instruments Example 5: NCD (Secondary Market – Dirty Price) ‘Dirty’ price of a £1,000,000 NCD with an original maturity of 182 days, a coupon of 7%, and remaining maturity of 60 days at a yield of 6.5% (Act/365) £1,000,000 x [1 + (7% x 182/365)] = £1,023,963.13 [1 + (6.5% x 60/365)] ‘Dirty price’ = ‘Clean price’ + accrued interest Acc int = £1,000,000 × (𝑐𝑐×𝑑𝑑𝑖𝑖𝑖𝑖 ) = £1,000,000 × (0.07×(182−60)) = £23,397.26 𝑦𝑦𝑦𝑦𝑦𝑦𝑦𝑦 365 ‘Clean’ = £1,023,963.13 - £23,397.26 = £1,000,565.87 14 Money Markets Yield Instruments Example 6: NCD Table ABSA NCD rate Bid Offer 5.15 4.90 3m (30 day) 4.95 4.70 6m (180 day) 4.85 4.60 12m (360 day) Given the quotes above, at what rate would you be able to buy a 6m NCD from the bank? You always buy at the offer rate 15 Money Markets Yield Instruments Example 6: NCD Table Three months later you need money urgently for bridging finance, and obtain the following rates from Standard Bank: SBSA NCD rate Bid Offer 5.25 5.10 3m (30 day) 5.15 5.00 6m (180 day) At what rate can you sell the NCD to Standard? You always sell at bid rate 16 Discount Instruments Money Markets Discount Instruments Discount Instruments: • Treasury Bills • Bankers’ Acceptances • Promissory Notes • Commercial Paper 18 Money Markets Discount Instruments Example 7: Treasury Bill (Primary Market) Calculate the amount to be invested in a 92-day Treasury bill at a rate of 10.25% and a face value of R10m. 𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃 = 10000000 x 1 − 0.1025 92 365 = R9 741 643.84 19 Money Markets Discount Instruments Example 8: Treasury Bill (Primary Market) A tenderer (buyer) decides the discount rate that he/she would like to earn is 15.80%. 1. The discount price/tender price will be: Price = 100 – 100x(15.80% x 91/365) = R96.061 He/she will submit a price of R96.06 2. The discount rate will then be: Discount rate = (100 – 96.06) x 365/91 = 15.80% 20 Money Markets Discount Instruments Example 9: Treasury Bill (Primary and Secondary Market) Bank A buys a 92-day Treasury bill that is issued at a rate of 10.25% with a face value of R5 million (Remember this is the primary market transaction) After 33 days the bank sells this T-Bill at 9.90% (This is the secondary market transaction) • What did the bank pay for the Treasury bill in the primary market? • What did the bank receive when they sold the bill? (secondary market) 21 Money Markets Discount Instruments Example 9 (cont.): Treasury Bill (Primary Market) What did Bank A pay for the TB? 92 = 5,000,000 − (5,000,000 × 0.1025 × ) 365 = 4,870,821.92 22 Money Markets Discount Instruments Example 9 (cont.): Treasury Bill (Secondary Market) What did Bank A receive when they sold the TB after 33 days at a rate of 9.90%? 59 = 5,000,000 − (5,000,000 × 0.0990 × ) 365 = 4,919,986.30 23 Money Markets Discount Instruments Example 10: Banker’s Acceptance (Primary Market) Issue mathematics: Proceeds payable to the drawer (the company) issued at discount) Nominal Value R 1 000 000 All in discount rate 10.70% days 90 Proceeds =R1 000 000 – (1 000 000 x (0.1070 x 90/365)) =R973 616.44 24 Money Markets Discount Instruments Example 11: Banker’s Acceptance (Primary Market) A bankers acceptance with a nominal value of R50 000 000 is issued at a discount of 9.95% for a period of 91 days. An acceptance commission of 1.5% of the nominal value is payable. Calculate the proceeds if you include the acceptance commission 9.95 + 1.5 91 P = 50m × 1 − × 365 100 = R 48 572 671.23 25 Money Markets Discount Instruments Example 11 (cont.): Banker’s Acceptance (Primary Market) A bankers acceptance with a nominal value of R50 000 000 is issued at a discount of 9.95% for a period of 91 days. An acceptance commission of 1.5% of the nominal value is payable: Calculate the proceeds if you exclude the acceptance commission 9.95 91 P = 50m × 1 − × 100 365 = R 48 759 657.53 26 Money Markets Discount Instruments Example 12: Commercial Paper You are interested in investing in a commercial paper issue with a face value of $20 million and181 days to maturity at a yield of 5.05% Calculate the amount that you would need to invest 20 ,000 ,000 P= 181 5.05 1 + × 360 100 = $19,504,768.51 27 Discount to Yield Instrument Money Markets Discount to Yield Instrument Example 13: Commercial Paper (Zero Coupon) A small South African company issues zero-coupon commercial paper at the going YTM (yield) rate of 7.5% p.a. for 182-days, and a face value (FV) of R1m. Calculate the investment price? NB! We are looking for the discounted price to FV 1,000,000 Price Pr ice = 182 1 + 0.075 × 365 P = R 963950,88 Note: At maturity recieve R 1 000 000.00 i.e. the Future value 29 Money Markets Discount to Yield Instrument Example 14: Commercial Paper (Zero Coupon) A CP of face value of EUR 10 million with 91 days to maturity at a yield of 4.10% 10 ,000 ,000 91 4.1 × 1 + 360 100 = EUR 9,897,424.20 30 Returns and Yields Money Markets Returns and Yields Example 15: Commercial Paper (Zero Coupon) Example: NCD, issued for 91 days at 11.15% p.a. OR TB, issued for 91 days at 10.80% p.a. Conversion from discount to yield Formula: Example: Discountrate days − × discountra te 1 Base Yield = Yield = 10.80% 91 1 − 10.80% × 365 = 11.10% 32 Money Markets Returns and Yields Example 15 (cont.): Comparing Discount to Yield Issued Securities Example continued: NCD, issued for 91 days at 11.15% p.a. OR TB, issued for 91 days at 10.80% p.a. Conversion from yield to discount Formula: Discountrate = Yield days + × yield 1 Base Example: Discountrate = 11.15% 91 + × 1 11 . 15 % 365 Discountrate = 10.85% 33 Money Markets Returns and Yields Example 16: Comparing Discount to Yield Issued Securities Convert the following rates: id = 6.7%, d = 30, B = 365 to iy iy = 12.3%, d = 30, B = 365 to id iy id = id = 100 iy d × 1 + 100 B 0.123 30 1 + 0.123 × 365 = 12.1769% iy iy = id 100 = d i 1 − d × 100 B 0.067 30 1 − 0.067 × 365 = 6.7371% 34 Money Markets Returns and Yields Example 17: Holding Period Return – Yield Instruments Calculate the holding period return for the NCD, with a face value of R10m, issued for a period of 91 days and a maturity value of R10,277,986.30. 10,277,986.30 36500 = 11.15% − 1 × 𝑖𝑖ℎ = 91 10,000,000 Using the financial calculator N =1 PV = -10,000,000 FV = 10,277,986.30, PMT = 0, I% = 2,7799 (x 365/91) to annualize 35 Money Markets Returns and Yields Example 17 (cont.): Holding Period Return – Yield Instruments Calculate the holding period return for the NCD, if it was sold after 61 days for issued for a R10 186 309.52,and has a maturity value of R10,277,986.30. 10,277,986.30 36500 = 10.95% − 1 × 𝑖𝑖ℎ = 30 10,186,309.52 Note: 10.95% is the true yield on this investment. Using the financial calculator N =1 PV = -10,186,309.52 FV = 10,277,986.30 PMT = 0 I% = 0.90 (x 365/30) = 10.95% 36 Money Markets Returns and Yields Example 18: Holding Period Return – Yield Instruments You invested in a 270 day NCD with a face value of R10,000,000 and a coupon of 12.25%. You sold the NCD at a yield of 11.85% with 92 days left to maturity. Calculate your HPY on this NCD? ih 12.25 270 × 1 + 100 365 365 −1 × = 11.85 92 178 1 + 100 × 365 = 12.0955% 37 Money Markets Returns and Yields Example 19: Price, Yield and EAY – Discount Instrument Assume that you decide to tender for Treasury Bills at the weekly Friday SARB tender (91 day TBs) at a rate of 10.75%. Calculate the tender price 10.75 91 P = 100 × 1 − × 100 365 = 97,32% (97.3199) 38 Money Markets Returns and Yields Example 19 (cont.): Price, Yield and EAY – Discount Instrument Assume that you decide to tender for Treasury Bills at the weekly Friday SARB tender (91 day TBs) at a rate of 10.75%. Calculate the yield (both methods) 100 − 97.32 365 iy = × 97.32 91 = 11.05% (11.0455) OR iy = 0.1075 91 1 − 0.1075 × 365 = 11.05% (11.0460 ) 39 Money Markets Returns and Yields Example 19 (cont.): Price, Yield and EAY – Discount Instrument Assume that you decide to tender for Treasury Bills at the weekly Friday SARB tender (91 day TBs) at a rate of 10.75%. Calculate the effective rate? 11.05 100 ie = 1 + 365 91 365 91 −1 = 11.52% (11.5168) 40 Money Markets Returns and Yields Example 20: Holding Period Yield and EAY – Discount Instrument You purchased a Treasury Bill issued for 91 days at 12.35%. You sell the Bill after 33 days at 12%. Assuming a face value of R5,000,000. Calculate your holding period yield? i d P = N × 1- d × sm 100 B 12.35 91 = 5,000,000 × 1- × 100 365 = R 4,846,047.95 i d P = N × 1- d × sm 100 B 12.00 58 = 5,000,000 × 1- × 100 365 FV B ih = − 1 × PV d is 4,904,657.53 365 = − 1 × 4,846,047.95 33 = 13.38% = R 4,904,657.53 41 Money Markets Returns and Yields Example 20 (cont.): Holding Period Yield and EAY – Discount Instrument You purchased a Treasury Bill issued for 91 days at 12.35%. You sell the Bill after 33 days at 12%. Assuming a face value of R5,000,000. Calculate your holding period yield? 𝑖𝑖ℎ = 𝑖𝑖ℎ = 𝑖𝑖𝑡𝑡𝑡𝑡𝑡𝑡𝑡𝑡𝑡𝑡 𝑑𝑑𝑠𝑠𝑠𝑠 x 100 𝐵𝐵 𝑖𝑖 𝑑𝑑 1 − 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 x 𝑖𝑖𝑖𝑖 100 𝐵𝐵 1− 12 58 x 100 365 12.35 91 1− x 100 365 1− 𝑖𝑖ℎ = 13.38% 𝐵𝐵 −1 x 𝑑𝑑𝑖𝑖𝑖𝑖 365 −1 x 33 42 Money Markets Returns and Yields Example 20 (cont.): Holding Period Yield and EAY – Discount Instrument You purchased a Treasury Bill issued for 91 days at 12.35%. You sell the Bill after 33 days at 12%. Assuming a face value of R5,000,000. Calculate the effective yield? iy 100 ie = 1 + B d B d −1 13.38 100 = 1 + 365 33 = 14.2247% 365 33 −1 43 Money Markets Returns and Yields Example 21: Price and Holding Period Yield – Discount Instrument Assume that you decide to tender for Treasury Bills at a SARB special tender (135 day TBs) at a rate of 11.55%. Calculate the tender price? 11.55 135 P = 100 × 1 − × 100 365 = 95,73% (95.7281) 44 Money Markets Returns and Yields Example 21 (cont.): Price and Holding Period Yield – Discount Instrument Assume that you decide to tender for Treasury Bills at a SARB special tender (135 day TBs) at a rate of 11.55%. Calculate the yield (both methods)? 100 − 95.73 365 iy = × 95.73 135 = 12.06% (12.0598) iy = OR 0.1155 135 1 − 0.1155 × 365 = 12.07% (12.0654 ) 45 Money Markets Returns and Yields Example 21 (cont.): Price and Holding Period Yield – Discount Instrument Assume that you decide to tender for Treasury Bills at a SARB special tender (135 day TBs) at a rate of 11.55%. Calculate the effective rate? 12.07 100 ie = 1 + 365 135 365 135 −1 = 12.53% (12.5338) 46 End of lecture 2: Money Markets – Worked Examples