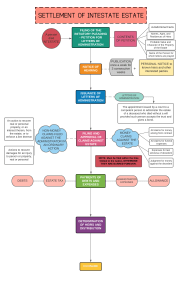

Chapter 1 Succession and Transfer Taxes According to Civil Code ownership may be acquired through: 1. Occupation 2. Intellectual Creation 3. Law 4. Donation 5. Tradition 6. Contract 7. Prescription 8. Succession Transfer taxes taxes imposed upon the gratuitous disposition of private properties or rights an excise tax Types of transfer taxes 1. Estate tax – donation mortis causa/time of death of donor 2. Donor’s tax – donation inter vivos/lifetime of both the donor and donee Succession – mode of acquisition by virtue of which, the property, rights, and obligations to the extent of the value of the inheritance, of a person are transmitted through his death to another or others either by his will or by operation of law The amount of obligation acquired/inherited by an heir should not be kore than the combined value of the properties and rights inherited Estate tax accrues the date of death of the decedent and payment of tax is distinct from the obligation to pay the same Succession takes place at the date of death of the decedent and the right of the State to the tax the privilege to transmit the estate vests instantly upon death Kinds of Succession 1. Testamentary or testate succession – designation of heir; made in a will executed in the form prescribed by law 2. Legal or interstate succession – effected by operation of law 3. Mixed succession – partly by will and partly by operation of law Causes of Legal Succession or Intestacy 1. If a person dies without a will, or with a void will, or one which has subsequently lost its validity 2. When the will does not institute an heir 3. Partial institution of heir (intestacy takes place as to the undisposed portion) 4. When the heir instituted is incapable of succeeding 5. Other causes: a. Non-fulfillment of suspensive condition b. Preterition – omission of one, some or all of the compulsory heirs which has the effect of annulling the institution of heir c. Fulfillment of resolutory condition d. Expiration of term or period of institution e. Non-compliance or impossibility of compliance with the will f. Repudiation of the instituted heir Elements of Succession 1. Decedent 2. Inheritance (estate) 3. Successor a. Compulsory heirs – those who succeed by force of law to some portion of the inheritance, in an amount predetermined by law, known as the legitime Kinds of Compulsory Heirs Primary – those who have precedence over and exclude other compulsory heirs Secondary – those who succeed only in the absence of the primary compulsory heirs Concurring – those who succeed together with the primary or secondary compulsory heirs *insert table b. Voluntary heirs – those instituted by the testator in his will to succeed to the inheritance of the portion thereof of which the testator can freely dispose c. Legal or intestate heirs – those who succeed the estate of the decedent by operation of law Composition of Gross Estate Legitime 75% Free portion 25% Order of Intestate Succession 1. Legitimate children or descendants 2. Legitimate parents or ascendants 3. Illegitimate children or descendants 4. Surviving spouse 5. Brothers and sisters, nephews and nieces 6. Other collateral relatives within the 5th degree 7. Stet or the government Consanguinity – relation of person descending from the same stock or common ancestors Lineal consanguinity – which may be descending or ascending, is that which subsists between persons of whom one is descended in a direct line from the other Collateral consanguinity – which subsists between persons who have the same ancestors, but who do not descend one from the other Will – an act whereby a person is permitted, with the formalities prescribed by law, to control to a certain degree the disposition of his estate to take effect after his death Kinds of Wills: 1. Notarial or ordinary or attested will 2. Holographic will Probate of a will is a court procedure by which a will is proved to be valid or invalid Codicil – supplement or addition to a will, made after the execution of a will and annexed to be taken as a part thereof, by which any disposition made in the original will is explained, added to, or altered Disinheritance – testamentary disposition by which a compulsory heir is deprived of, or excluded from the inheritance to which he has a right Requisites for disinheritance: 1. Effected only through a valid will 2. For a cause expressly stated by law 3. Cause must be stated in the will itself 4. Cause must be certain and true 5. Unconditional 6. Total (no partial disinheritance) 7. The heir disinherited must be designated in such a manner that there can be no doubt as to his identity Chapter 2 Gross Estate Composition of Gross Estate Decedent Gross Estate 1. Property Citizen (real or Nonresident personal) Citizen worldwide Resident 2. Intangible Alien personal property worldwide 1. Real Nonresident property Alien situated in the Phil. 2. Tangible personal property situated in the Phil. 3. Intangible personal property with situs in the Philippines UNLESS excluded bc of reciprocity Intangible Assets with Situs “Within” the Philippines 1. Franchise exercised in the Phil. 2. Shares, obligation or bonds issued by any corporation or sociedad anonima organized in the Phil. In accordance with its laws 3. Shares , obligations, or bonds issued by any foreign corporation, 85% of the business of which is located in the Phil. 4. Shares, obligations, or bonds issued by any foreign corporation if such shares, obligations or bonds have acquired a business situs in the Philippines 5. Shares or rights in any partnership, business or industry established in the Philippines Note: Generally, the situs of intangible personal property is the domicile of the owner (only for convenience) Valuation of Gross Estate 1. In General: FMV at time of death 2. Real Property Higher between: o FMV Commissioner o FMV Assessors 3. Personal Property: FMV at time of death 4. Shares of stock o Unlisted CS: Book Value o Unlisted PS: Par Value o Listed Shares: FMV using arithmetic mean between the highest and lowest quotation at the time nearest the DOD 5. Units pf participation in any association, recreation, or amusement club o Bid price nearest the DOD published 6. Right to usufruct, use or habitation, and annuity o According to the latest Basic Standard Mortality Table Exemptions and Exclusions from the Gross Estate A. Exclusions under Section 85 and 104 1. Exclusive property of the surviving spouse o GE shall include exclusive properties and common properties of the decedent o Capital = exclusive properties of husband o Paraphernal = exclusive properties of wife 2. Properties outside the Philippines for NRA 3. Intangible personal property in the Philippines of an NRA under Reciprocity Law B. Exclusions under Section 87 1. Merger of usufruct in the owner of the naked title 2. Fideicommisary (1 degree apart) Elements: o Substitution must not go beyond 1 degree from orginal heir o Fiduciary and fideicommissary must be both living at the time of testator’s death 3. Transfer under special power of appointment 4. All bequest devises, legacies or transfers to social welfare, cultural and charitable institutions C. Exclusions under Special Laws 1. Proceeds of life insurance and benefits from GSIS 2. Accruals an benefits received from SSS 3. Amounts received from Philippines and US government for war damages 4. Amounts received from US Veterans administration 5. Payment from the Philippines of US government to the legal heirs of deceased of WW2 Veterans 6. Retirement benefits from a private firm 7. Personal Equtiy and Retirement Account (PERA) 8. Compensation paid to HCW for death caused by COVID-19 Composition of Gross Estate Real Property Personal Property Intangible Personal Property Shares of stock Bank deposit Dividends declared BEFORE death but received AFTER death Partnership profit which have accrued before death Usufructuary and rights I. PROPERTY OWNED ACTUALLY AND PHYSICALLY PRESENT a. Decedent’s interest Extend of equity or ownership participation of the decedent on any property physically existing II. III. PROPERTY NOT PHYSICALLY IN THE ESTATE BUT ARE SUBJECT TO ESTATE TAX a. Transfer in contemplation of death b. Revocable transfers terms of enjoyment of property may be altered, amended, revoked or terminated It is sufficient that he had the power to revoke though not exercised c. Transfers under a General Power of Appointment Donee of a GPA holds the appointed property with all the attributes of ownership d. Transfers for Insufficient Consideration 1. Consideration vs. FMV @ time of transfer/sale – see if adequate 2. If inadequate, find difference between consideration and FMV @ time of death to be included in GE MISCELLANEOUS ITEMS a. Claims against insolvent persons Should be included in computation of GE Claim which is not collectible should be allowed as deduction from GE Prorate the payment of liabs b. Proceeds of life insurance 1. Must be insurance on life of decedent 2. Beneficiary must be either: Estate or executore/administrato r Any third person provided that the designation is NOT IRREVOCABLE (revocable) If silent, revocable meaning added to GE Proceeds of Life Insurance Beneficiary Designation GE Inclusion Estate R or IR Executor R or IR Administrator R or IR 3rd Party R rd 3 Party IR X ESTATE TAX RATE Net estate whether resident or nonresident shall be subject to an estate tax rate of 6% Chapter 3 Deductions from Gross Estate Classification: 1. Ordinary Deductions 2. Special Deductions 3. Share of the surviving spouse, if the decedent is married I. ORDINARY DEDUCTIONS A. LITe (Losses, Indebtedness, taxes, etc.) 1. Losses o Pertains to casual losses Requisites: o Arising exclusively from acts of God and man o Not compensated by insurance o Not deducted from income tax return o Incurred during the settlement period of the estate (within 1 year from date of death) 2. Indebtedness or Claims against estate Requisites: o Personal obligation existing at the time of death (not after death) o Contracted in good faith and for adequate and full consideration o Debt or claim is valid in law and enforceable in court o Debt must not be condoned by creditor Substantiation Requirements: In case of simple loan a. Duly notarized debt instrument b. Duly notarized Certification of the creditor c. Proof of financial capacity of the creditor to lend d. Statement under oath executed by the administrator or executor of the estate reflecting the disposition of the proceeds of the loan if said loan was contracted within 3 years prior to the death of the decedent If unpaid obligation arose from purchase a. Pertinent documents evidencing purchase b. Duly notarized Certification from the creditor as to the unpaid balance of the debt c. Certified true copy of the latest audited BS of the creditor d. Pertinent documents filed with the Court evidencing the claims against the estate UNPAID MORTGAGES OR INDEBTEDNESS ON PROPERTY o Deductions allowed when a decedent leaves property encumbered by a mortgage or indebtedness contracted in good faith and for adequate and full consideration o GE must include the FMV of property encumbered in order to be deducted o ACCOMMODATION LOAN o Where loan proceeds went to another person, the value of the unpaid loan must be included as a receivable of the estate 3. Taxes o Unpaid taxes that accrued prior to the death of the decedent o Not allowed as deduction: Income tax on income received AFTER death Property taxes accrued AFTER death Estate tax 4. Claims Against Insolvent Persons Requisites: (judicial declaration NOT required) o Incapacity of the debtor o Full amount owed by the insolvent must first be included in the decedent’s gross estate o and the amount uncollectible shall be allowed as deduction o Insolvent could only pay partial amount, the full amount owed shall be included in GE and the amount uncollectible be allowed as deductions o o B. TRANSFER FOR PUBLIC USE (TFPU) o Dispositions in a last will and testament or transfers to take effect after the death in favor of the government of the Philippines or any of its political subdivision for exclusive public purposes o Allowed as deduction from GE provided same amount was included in the computation of the decedent’s GE C. VANISHING DEDUCTIONS (PROPERTY PREVIOUSLY TAXED) Requisites: o o o Death of present decedent within 5 years from the date of death of prior decedent or date of gift Identity of property Property must be located in the Philippines Property must have formed part of the situated in the Philippines of the prior decedent Estate tax on the prior succession or the donor’s tax on the gift must have been finally determined and paid (purpose is to lessen double taxation) No previous vanishing deduction on the property Rates: Within 1 year Beyond 1 year – 2 Beyond 2 years – 3 Beyond 3 years – 4 Beyond 4 years – 5 100% 80% 60% 40% 20% Computation: VALUE TO TAKE Lower between o Gross estate of prior decedent or gross gift of the donor o Gross estate of present decedent LESS: MORTGAGE PAID (paid by present decedent from mortgage assumed) INITIAL BASIS LESS: Proportional Deduction Initial Basis/Gross Estate x LIT + TFPU FINAL BASIS x Vanishing deduction rate VANISHING DEDUCTION II. SPECIAL DEDUCTIONS A. STANDARD DEDUCTION o Citizen or Resident – P5 Million o Nonresident Alien – P500,000 o The only special deduction allowed to a NRA decedent B. FAMILY HOME o Allowable as a deduction would be whichever is lower of P10 Million or the FMV at the time of the decedent’s death Limitation: o Availing of a family home deduction to the extent allowable, a person may constitute only 1 family home Requisites: o Decedent was married or if single, was head of the family o Family home as well as the land on which it stand must be own by the decedent o Must be the actual residential home of the decedent and his family at the time of death o Allowable deduction must be in an amount equivalent to the current FMV of the family or extent of the decedent’s interest (if conjugal) whichever is lower but not exceeding P10 Million C. AMOUNT RECEIVED BY HEIRS UNDER RA 4917 o Any amount received by heirs from the decedent’s employer as a consequence of the death of the decdent-employee, provided such amount is included as part of the gross estate of the decedent NET SHARE OF THE SURVIVING SPOUSE The amount deductible under this category is the net share of the surviving spouse in the conjugal partnership property Equivalent to 50% of the conjugal property after deducting the obligations chargeable to such property Chapter 6 Donor’s Tax A tax levied, assessed, collected, and paid upon the transfer by any person, resident or nonresident, of the property by gift. Direct tax & excise tax Applies to both natural and juridical persons Perfection – moment the donor knows of the acceptance by the donee Completion – actual or constructive delivery ELEMENTS OF DONATION (all must be present) 1. Capacity of the donor to make a donation o Must have capacity to contract and capacity to dispose (determined at the perfection of the donation) 2. Donative intent or intent to make a gift on the part of the donor o Intent is required only in direct gifts 3. Delivery o Applies to completed gift (when delivered) INCOMPLETE GIFT o Because of reserved powers, becomes complete when either: Donor renounces the power Donor’s right to exercise power ceases because of the happening of some event or contingency 4. Acceptance o Donation is a contract that requires the meeting of the minds o Transfer is perfected the moment the donor knows of the acceptance of the donee PURPOSE OF DONOR’S TAX 1. To prevent avoidance of estate tax 2. To prevent or compensate for the loss of the progressive rates of income tax when large estates are split up by gifts to numerous donees FORMALITIES Donation not in a formal contract is void Type Amount Form Personal ≤P5,000 Oral or in Property writing >P5,000 In writing Real Property Any amount Public instrument Acceptance of immovable property To be valid, immovable property may be accepted: In the same deed of donation In a separate public document CHARACTERISTICS OF DONOR’S TAX 1. Excise tax not a property tax 2. Donor’s tax does not apply if gift is not completed 3. Perfected the moment the donor knows of the acceptance by the done 4. Donor’s tax is a direct tax CLASSIFICATION OF DONATION 1. Simple – cause is pure liberality 2. Renumeratory – due to past services rendered or future services or charges 3. Modal – consideration is less than the value of the thing donated VOID DONATIONS 1. Those made between persons who were guilty of adultery or concubinage at the time of the donation 2. Those made between persons found guilty of the same criminal offense, in consideration thereof 3. Those made to a public officer or his wide, descendants, and ascendants by reason of his office VALUATION OF GROSS GIFTS General rule: FMV @ time donated Property Valuation Real Property HIGHER: FMV determined by the Commissioner and FMV fixed by assessors (appraised value not included) Listed Stocks Not traded: Ordinary Shares Preferred Shares Arithmetic mean between the highest and lowest quotation at the date nearest the date of death Book value Par value DONOR’S TAX RATE 6% on the basis of the total gifts in excess of P250,000 GROSS GIFT Same rules for estate tax Inclusions: 1. Direct gifts 2. Gifts through the creation of trust 3. Transfer for insufficient fund 4. Condonation of debt 5. Repudiation of inheritance 6. Renunciation of the surviving spouse of share in common property TRANSFER FOR INSUFFICIENT CONSIDERATION EXCEPT for real property subject to CGT FMV – Considetion/Selling Price shall be deemed as a gift Fictitious consideration – entire value shall be subject to donor’s tax *insert table Shares of Stock not traded o Excess of FMV over selling price shall be treated as a gift subject to Donor’s tax CONDONATION OR CANCELLATION OF INDEBTEDNESS Condonation due to rendition of service – effect of payment compensation (subject to income tax) Condonation was made by a corporation in favor of its shareholders – effect of payment of dividend by issuing corporation (subject to final tax) PAYMENT OF LOAN BY THE GUARANTOR General rule: guarantee is gratuitous unless stated otherwise Exception: if jointly entered by guarantor and borrower REPUDIATION OF INHERITANCE General rule: “general renunciation” is not subject to donor’s tax UNLESS: 1. Renunciation was categorically done in favor of identified heirs; AND 2. To the exclusion or disadvantage of other co-heirs Note: if common property is renounced by spouse it is subject to donor’s tax, however, renunciation of hereditary estate is subject to donor’s tax only if the aforementioned are present *INSERT DIAGRAM EXEMPT GIFTS AND/OR DEDUCTIONS FROM GROSS GIFTS 1. Donations not exceeding P250,000 2. Gifts to or for the use of the National Government 3. Gifts in favor of non-profit educational and/or charitable, religious, cultural or social welfare corporation, institution, etc. EXCEPT: o When conducted for profit o More than 30% is used for administrative purposes 4. Donations made to entities as exempted under special laws 5. Encumbrances on the property donated if assumed by the done 6. Diminutions – decrease in the value of the donated property as a result of a condition made by a donor to the done DONATIONS MADE BY SPOUSES Gift from common property – the gift is taxable one-half to each donor spouse Donation between husband and wife during marriage General rule: Void Exception: Moderate gifts Note: The agreement that the done shall pay the donor’s tax due is binding only between the donor and one. It will not bind the BIR. DONATIONS MADE BY FOREIGN CORPORATION Subject to donor’s tax only if property donated is located in the Philippines Donation of its own shares is NOT subject to donor’s tax Donation of its shares in favor of a resident employee is not subject to a donor’s tax (employer-employee relationship) Chapter 7 Introduction to Business Taxes Business taxes – those imposed upon onerous transfers such as sale, barter, exchange and importation. Generally based on gross sales or gross receipts “In the course of trade or business” means regular conduct or pursuit of a commercial or an economic activity, including transactions incidental thereto, by any person, regardless of whether the person engaged therein is a nonstock private organization or government entity. ISOLATED TRANSACTIONS Residents – considered not in the ordinary course of trade or business, thus, not subject to vat Nonresidents – considered in the ordinary course of trade or business, thus subject to FWT Note: If asset sold is an ordinary asset used in the business and is an incidental transaction, it is subject to vat. Types of Business Taxes 1. Value Added Tax (VAT) 2. Other Percentage Taxes (OPT) 3. Excise Taxes GR: All sales and services made in the normal course of trade or business are subject to vat EX: Exempt under law (may be subject to OPT) VAT & OPT are mutually exclusive but both can be subject to excise tax Business Taxes SALE of goods/properties/services VAT, in general VAT exempt, but OPT Exempt from BT Manufac/Import & Sale of Sinproducts, Non-essential VAT OPT VAT / x E OPT x / E ExT x X - VAT / x OPT x / ExT / / I. VALUE ADDED TAX Tax on the value added by every seller to the purchase price or cost in the sale or lease of goods, property or services in the ordinary course of trade or business as well as importation of goods into the Philippines, whether for personal or business use. Kinds of VAT 1. VAT on sale of goods or properties 2. VAT on importation of goods 3. VAT on sale of services and use or lease of properties Persons Liable Sale in the Ordinary Course: seller & importer in the course of his trade or business Importation: indiv or corpo whether or not made for trade/business TRANSFER BY A TAX-EXEMPT ENTITY TO NONETAX EXEMPT ENTITY - In case of tax free importation of goods into the Philippines by persons, entities, or agencies exempt from tax where such goods are subsequently sold, transferred, or exchanged in the Philippines to non-exempt persons or entities, the purchasers, transferees or recipients shall be considered the importers thereof, who shall be liable for any internal revenue tax on such importation MEANING OF THE TERM “GOODS OR PROPERTIES” All tangible and intangible objects which are capable of pecuniary estimation and shall include: 1. Real properties held primarily for sale to customers or held for lease in the ordinary course of trade or business 2. The right or the privilege to use patent, copyright, design or model, plan, secret formula or process, goodwill, trademark, trade brand or other like property or right 3. The right or the privilege to use motion picture films, films, tapes, and discs 4. Radio, television, satellite transmission and cable television time SALE OF SERVICES - Performance of services in the Philippines - Vat on sale of service is a tax on payments for services - Indirect tax which may be passed on to the customer - Accrues at the time service fee is collected SALE OF REAL PROPERTIES - Sale of real properties held primarily for sale to customers or held for lease in the ordinary course of trade or business of seller - Installment sale – installment payment including interest & penalties (actual/constructive) subject to vat Characteristics of Vat 1. Indirect tax where tax shifting is always presumed o Burden of the tax is borne by the final consumer; producers & suppliers file these VAT returns o Burden is passed but not the liability to the BIR 2. Consumption-based 3. Imposed on the value-added in each stage of production and distribution process 4. Credit-invoice method value-added tax BASIS FOR VAT 1. Sale of goods or properties o Gross Selling Price o Discount may be deducted if not dependent upon the happening of a future event o Returns are deductible if a proper credit/credit memo is given o Add excise tax to get tax base 2. Sale of service o Gross Receipts o Receivables not included although earned (only cash actual or constructively received) 3. Dealer in securities and lending investors o Gross Income o Add other income subject to basic tax Note: If vat is not billed separately in the document of sale, the SP shall be deemed to be inclusive of vat GROSS SELLING PRICE - Total amount of money or its equivalent - Excise tax, if any, shall form part of the GSP - Sale, barter, or exchange subject to vat shall mean consideration stated in the sales document or FMV whichever is higher - FMV – 1) FMV determined by Commissioner 2) FMV by provincial/city assessors - If GSP is based on FMV it shall be deemed exclusive of vat GROSS RECEIPTS - Total amount of money or its equivalent representing contract price, compensation, service fee, rental, or royalty - Including amount charged for materials supplied with the services and deposits applies as payments for services rendered AND advance payments actually or constructively received during the taxable period, excluding vat - “constructive receipt” when money consideration or its equivalent is placed at the control of the person who rendered the service w/o restriction VAT REGISTRATION A. MANDATORY REGISTRATION 1. Gross sales/receipts exceed P3 Million for the past 12 months (except those vat exempt) or there are reasons to believe that the gross sales/receipts for the next 12 months will exceed P3 Million 2. Radio and/or television broadcasting companies whose annual gross receipts of the preceding year exceeds P10 Million (mandatory registration applies within 30 days from the end of the taxable year) 3. Person to register as VAT taxpayer but failed to register Note: Penalty of non-registration – taxpayer shall be liable to pay the tax as if he were VAT registered person but cannot avail of the benefits of input tax credit for the period he was not properly registered B. OPTIONAL REGISTRATION 1. Registering with the RDO and shall not be allowed to cancel registration for the next 3 years 2. Franchise grantees of radio and/or television broadcasting whose annual gross receipts of the preceding year does not exceed P10 Million. Once exercises, shall be irrevocable. - Shall register not later than 10 days before the beginning of the calendar quarter and shall pay the registration fee unless they have already paid at the beginning of the year; effective on the first day of the month following registration Power of Commissioner to Suspend Business Operations - Suspension/closure for not less than 5 days 1. Failure to issue receipts or invoices 2. Failure to file vat return 3. “Understatement” of taxable sales or receipts by 30% or more of the correct taxable sales or receipts for the taxable quarter 4. Failure of any person to register as required under the law II. OTHER PERCENTAGE TAXES (OPT) Any person who is not a VAT registered person and is not exempt from business tax shall be subject to other percentage taxes. III. EXCISE TAXES Apply to goods manufactured or produced in the Philippines for domestic sales or consumption or for any other disposition, and goods imported. The goods manufactured or imported under this category are classified as either “sin products” or “non-essential goods.” Chapter 10 Excise Taxes