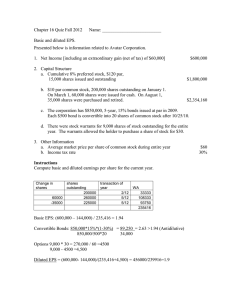

1) Alamo, Inc., had $300 million in taxable income for the current year. Alamo also had a decrease in deferred tax assets of $30 million and an increase in deferred tax liabilities of $60 million. The company is subject to a tax rate of 40%. The total income tax expense for the year was A. $150 million. B. $180 million. C. $ 390 million. D. $210 million. 2) When tax rates are changed subsequent to the creation of deferred tax asset or liability, IFRS requires that: A. Only the current deferred tax accounts are adjusted to reflect the new tax rates B. The beginning deferred tax accounts are left unchanged C. Only the noncurrent deferred tax accounts are adjusted to reflect the new tax rates D. All deferred tax accounts be adjusted to reflect the new tax rates. 3) At 30 June 20X3, the gross amount of the accounts receivable of Atom Ltd (Atom) was $10 000. At the same date, there was a related allowance for doubtful debts of $500. Revenue from sales is included in the statement of profit or loss and other comprehensive income in the same period as it is included in taxable profit. The tax rate is 30 per cent. At 30 June 20X3, Atom would recognise which one of the following items in its statement of financial position? A. Deferred tax liability of $2850 B. Deferred tax liability of $150 C. Deferred tax asset of $2850 D. Deferred tax asset of $150 4) If restricted shares are forfeited because an employee leaves the company., the appropriate accounting procedure is to: A. Do nothing B. Prepare correct entries C. Reverse related entries previously made D. Record an income item 5) At December 31, 2011 Hansen Corporation had 50,000 shares of common stock and 5,000 shares of 6%, $100 par cumulative stock outstanding. No dividends were declared or paid in 2011. Net income was reported as $200,000. What is basic EPS? A. $4.02 B. $3.64 C. $3.40 D. $4.00 6) During 2018, Angel Corporation had 900,000 shares of common stock and 50,000 shares of 6% preferred stock outstanding. The preferred stock does not have cumulative or convertible features. Angel declared and paid cash dividends of $300,000 and $150,000 to common and preferred shareholders, respectively, during 2018. On January 1, 2017, Angel issued $2,000,000 of convertible 5% bonds at face value. Each $1,000 bond is convertible into five common shares. Angel's net income for the year ended December 31, 2018, was $6 million. The income tax rate is 20%. What is Angel's basic earnings per share for 2018, rounded to the nearest cent? A. None of these is correct B. $5.29 C. $6.50 D. $5.57 Answer: $6.5 per share Explanation: Given that, Net income = $6,000,000 Preferred dividend = $150,000 Weighted average number of common shares = 900,000 Angel's Basic earnings per share: [Net income - Preferred dividend ] ÷ Weighted average number of common shares = [$6,000,000 - $150,000] ÷ 900,000 = 5,850,000 ÷ 900,000 = $6.5 per share 7) ABC declared and paid cash dividends to its common shareholders in January of the current year. The dividend: A. Has no effect on the earnings per share for the coming year. B. Will be subtracted from numerator of the earnings per share fraction for the current year C. Will be added to the denominator of the earnings per share fraction for the current year D. Will be added to the numerator of the earnings per share fraction for the current year 8) A deferred tax asset represent a: A. Future tax refund B. Future income tax benefit C. Future amount of money to be paid out D. Future cash collection 9) Diluted convertible bonds affect both the numerator and the denominator in computing diluted EPS: A. True B. False 10) A. B. C. D. Nonconvertible bonds affect the calculation of: Diluted earnings per share. None of these answer choices are correct Basic earnings per share. Basic earnings per share and Diluted earnings per share. 11) A. B. C. D. A simple capital structure might include: Stock rights Convertible bonds. Nonconvertible preferred stock Stock purchase warrants. 12) Which of the following causes a temporary difference between taxable and pretax accounting income? A. Investment expenses incurred to generate tax-exempt income. B. MACRS used for depreciating equipment. C. The dividends received deduction. D. Life insurance proceeds received due to the death of an executive. 13) During the current year, Stern Company had pretax accounting income of $45 million. Stern's only temporary difference for the year was rent received for the following year in the amount of $15 million. Stern's taxable income for the year would be: A. $60 million. B. $30 million. C. $50 million. D. $45 million. 14) Premium on bonds payable is a contra account to bonds payable that increases its value and is added to bonds payable in the long‐term liability section of the balance sheet. A. True B. False 15) On January 1, 2016, Oliver Foods issued stock options for 40,000 shares to a division manager. The options have an estimated fair value of $5 each. To provide additional incentive for managerial achievement, the options are not exercisable unless Oliver Foods' stock price increases by 5% in four years. Oliver Foods initially estimates that it is not probable the goal will be achieved. How much compensation will be recorded in each of the next four years? A. $200.000 B. $0 C. $50.000 D. $800.000 E. $210.000 16) Given the definition adopted in IAS 32 financial instruments: presentation, which one of the following would not be a financial instrument A. Cash at bank. B. Bill of exchange. C. Prepaid insurance. D. Forward exchange 17) The most important accounting objective for executive stock options is: A. Measuring and reporting the amount of compensation expense during the service period B. Measuring their FV for balance sheet purposes C. None of these answer choices are correct D. To disclose increases or decreases in the stock options held at the end of each accounting period 18) On January 1, 2013, an investor paid $291,000 for bonds with a face amount of $300,000. The contract rate of interest is 8% while the current market rate of interest is 10%. Using the effective interest method, how much interest income is recognized by the investor in 2014 (assume annual interest payments and amortization)? A. $23,280 B. $25,140 C. $29,100 D. $29,610 19) According to IAS 32, which one of the following instruments would be classified as equity A. Redeemable preference shares with a fixed redemption date B. Redeemable preference share at the discretion of the issuer C. Redeemable preference share in fice years at the request of the holder D. Redeemable preference shares redeemable at the discretion of the issuer, who has given formal notification of such intention 20) Pretax accounting income for the year ended December 31, 2013, was $50 million for Truffles Company. Truffles' taxable income was $60 million. This was a result of differences between straight-line depreciation for financial reporting purposes and MACRS for tax purposes. The enacted tax rate is 30% for 2013 and 40% thereafter. What amount should Truffles report as the current portion of income tax expense for 2013? A. $15 million B. $18 million ($60.000 x 30%) C. $20 million D. $24 million 21) Straight-line amortization of bond discount or premium: A. Can be used for amortization of discount or premium in all cases and circumstances B. Provides the same amount of interest expense each period as does effective interest method C. Is appropriate for deep discount bonds D. Provides the same total amount of interest expense over the life of the bond issue as does the effective interest method 22) Which one of the following instruments does not satisfy the sole payments of interest A. A variable rate loan where the rate varies based on LIBOR up to a specified upper cap B. A variable rate loan where the rate varies based on LIBOR and any changes in the credit risk C. A variable rate loan where, if the loan is repaid before maturity, the borrower pays a 25% premium as penalty for early repayment D. A variable rate loan where the loan can be extended and the amount to be repaid is determined based on the amount outstanding at the applicable interest rate at the time 23) Which of following statement is wrong? A. At inception, accountant does no record the journal entry for forward contract B. When there is a gain on the purchased option, there is a loss on the written option C. At closing of position or at expiration of contract, accountant always records the increase in cash for purchased option D. All of free-standing derivatives are recognized gain or loss during their life 24) A company enters a forward exchange contract to hedge a USD receivable. Assuming that the receivable is measured at fair value, what is the required measurement of the forward exchange contract under IFRS 9 Financial Instrument? A. Cost B. Fair value C. Lower of cost and fair value D. Any of the above 25) On January 1, 2013, M Company granted 90,000 stock options to certain executives. The options are exercisable no sooner than December 31, 2015, and expire on January 1, 2019. Each option can be exercised to acquire one share of $1 par common stock for $12. An option-pricing model estimates the fair value of the options to be $5 on the date of grant. What amount should M recognize as compensation expense for 2013? A. $150.000 B. $30.000 C. $60.000 D. $120.000 26) On January 1, 2013, M Company granted 90,000 stock options to certain executives. The options are exercisable no sooner than December 31, 2015, and expire on January 1, 2019. Each option can be exercised to acquire one share of $1 par common stock for $12. An option-pricing model estimates the fair value of the options to be $5 on the date of grant. If unexpected turnover in 2014 caused the company to estimate that 10% of the options would be forfeited, what amount should M recognize as compensation expense for 2014? A. $150.000 B. $30.000 C. $60.000 D. $120.000 27) Changes in enacted tax rates that do not become effective in the current period affect deferred tax accounts only after the new rates take effect A. True B. False 28) Changes in enacted tax rates only affect income tax expense in the years those changes affect tax payable. A. True B. False 29) On June 30, 2013, Blair Industries had outstanding $80 million of 8% convertible bonds that mature on June 30, 2014. Interest is payable each year on June 30 and December 31. The bonds are convertible into 6 million shares of $10 par common stock. At June 30, 2013, the unamortized balance in the discount on bonds payable account was $4 million. On June 30, 2013, half the bonds were converted when Blair's common stock had a market price of $30 per share. When recording the conversion, Blair should credit paid-in capitalexcess of par: A. $6 million. B. $8 million. C. $10 million. D. $12 million. 30) Woody Corp. had taxable income of $8,000 in the current year. The amount of MACRS depreciation was $3,000, while the amount of depreciation reported in the income statement was $1,000. Assuming no other differences between tax and accounting income, Woody's pretax accounting income was: A. $5,000 B. $6,000. C. $10,000. D. $11,000. 31) Under its executive stock option plan, N Corporation granted options on January 1, 2013, that permit executives to purchase 15 million of the company's $1 par common shares within the next eight years, but not before December 31, 2015 (the vesting date). The exercise price is the market price of the shares on the date of grant, $18 per share. The fair value of the options, estimated by an appropriate option pricing model, is $4 per option. No forfeitures are anticipated. Ignoring taxes, what is the effect on earnings in the year after the options are granted to executives? A. $0 B. $20m (=4x15/3) C. $60m D. $90m 32) FX Services granted 15 million of its $1 par common shares to executives, subject to forfeiture if employment is terminated within three years. The common shares have a market price of $8 per share on the grant date. Ignoring taxes, what is the effect on earnings in the year after the shares are granted to executives? A. $0. B. $15 million. C. $40 million. D. $120 million. 33) XYZ Ltd issues five-year interest-bearing bonds. The bonds are convertible to a fixed number of equity instruments of the issuer at the discretion of the holder. How should the bonds be classified unter IAS 32? A. As equity B. As a liability C. As either equity or a liability D. As having equity and liability components 34) On December 31, 2012, the Bennett Company had 100,000 shares of common stock issued and outstanding. On July 1, 2013, the company sold 20,000 additional shares for cash. Bennett's net income for the year ended December 31, 2013, was $650,000. During 2013, Bennett declared and paid $89,000 in cash dividends on its nonconvertible preferred stock. What is the 2013 basic earnings per share? A. $5.91 B. 5.61 C. 5.10 D. None of these is correct 35) In 2013, Bodily Corporation reported $300,000 pretax accounting income. The income tax rate for that year was 30%. Bodily had an unused $120,000 net operating loss carryforward from 2011 when the tax rate was 40%. Bodily's income tax payable for 2013 would be: A. $54.000 B. $90.000 C. $42.000 D. $72.000 36) On December31, 2012, Albacore Company had 300,000 shares of common stock issued and outstanding. Albacore issued a 10% stock dividend on June 30,2013. On September 30, 2013, 12,000 shares of common shares were reacquired as treasury stock. What is the appropriate number of shares to be used in the basic earnings per share computation for 2013? A. 303,000 B. 342,000 C. 312,000 D. 327,000 Acct 325 Exam 2- EPS Flashcards | Quizlet CHAPTER 34 SHARE-BASED PAYMENT. - ppt video online download (slideplayer.com) docx.pdf TRẮC NGHIỆM KTQT 2 Flashcards | Quizlet Theory Chapter 16 Flashcards | Quizlet