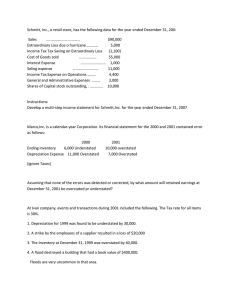

lOMoARcPSD|9190468 Pdfcoffee Notes Engineering Economics (Caraga State University) StuDocu is not sponsored or endorsed by any college or university Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 Philippine School of Business Administration ACCOUNTING 13: Accounting Policies, Changes in Accounting Estimates And Errors Submitted to: Prof. Rene Boy Ariola Submitted by: LITONJUA, KIM CAMILLE MANLANGIT, CHARMAINE MOLINA, CLAZELLE ANNE OPPUS, KATHLEEN DEI RAMIREZ, FATIMA Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 THEORIES 1. Which of the following is not a counterbalancing error? a. An understatement of purchases in the current period because the invoice was received late. b. Omission of depreciation for equipment purchased during the current period. c. Omission of an adjustment to take up the unused supplies during the period. d. Understatement of accrued salaries expense. 2. A company using a periodic inventory system neglected to record a purchase of merchandise on account at year end. This merchandise was omitted from the year end physical count. How will these errors affect assets, liabilities and equity at year end and net earnings for the year end? Assets Liabilities Equity Net Earnings a. No Effect b. No effect c. Understated d. Understated Understated Overstated Understated No effect Overstated Understated No effect Understated Overstated Understated No effect Understated 3. Which of the following if discovered in the accounting period subsequent to the period of occurrence, requires an entity to report the correction of an error? a. The estimate of useful life of a depreciable asset should have been revised. b. A change from double declining to straight line depreciation. c. Capitalization of an expense. d. Change in percentage of sales used for determining bad debt expense. 4. Which of the following would cause income of the current period to be understated? a. b. c. d. Capitalizing research and development cost. Failure to recognize unearned rent revenue. Changing from weighted average to FIFO for merchandise inventory. Understating estimate of residual value. 5. At the end of the current year, special insurance costs, incurred but unpaid, were not recorded. If these insurance costs were related to work in process, what is the effect of the omission on accrued liabilities and retained earnings in the current year-end statement of financial statement? Accrued Liabilities Retained Earnings a. b. c. d. No effect No effect Understated Understated No effect Overstated No effect Overstated 6. Which of the following errors would result in an overstatement of both current assets and shareholders’ equity? Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 a. b. c. d. An understatement of accrued sales commissions. Noncurrent note receivable principal is misclassified as current asset. Annual depreciation on manufacturing machinery is understated. Holiday pay expense for administrative employees is misclassified as manufacturing overhead. 7. Which of the following errors will not self-correct in the next year? a. b. c. d. Accrued expenses not recognized at year-end. Accrued revenue not recognized at year-end. Depreciation expense overstated for the year. Prepaid expenses not recognized at year-end. 8. Failure to record the expired amount of prepaid rent expense would not: a. b. c. d. Understate expense Overstate income Overstate owners’ equity Understate liabilities 9. The effect of a change in the expected pattern of consumption of economic benefit of a depreciable asset shall be a. Included in the determination of income or loss in the period of change only. b. Included in the determination of income or loss in the period of change and future periods. c. Included in the statement of retained earnings as an adjustment in the beginning balance. d. Included in the other comprehensive income. e. 10. A change from the straight line method depreciation of sum of year’s digits method is accounted for as a. b. c. d. Change in accounting policy Change in accounting estimate Prior period error Accounting error 11. If at the end of reporting period, an entity erroneously excluded some goods from its ending inventory and also erroneously did not record the purchase of these goods in its accounting records, these error would cause, a. The ending inventory cost of goods available for sale and retained earnings to be understated. b. The ending inventory cost of goods sold and retained earnings to be understated. c. No effect on net income, working capital and retained earnings. d. Cost of goods available for sale, cost of goods sold and net income to be understated. Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 12. Failure to record depreciation at the end of an accounting period results in a. b. c. d. Understated income Understated assets Overstated expenses Overstated assets 13. An entity uses a periodic inventory system. If the entity’s beginning inventory in the current year is overstated, that is the only error in the current year, then the entity’s income for the current year would be a. b. c. d. Understated and assets correctly stated Understated and assets overstated Overstated and assets overstated Understated and assets understated 14. Which of the following statements is TRUE? I. A change in accounting principle is a change that occurs as the result of new information or additional experience. Errors in financial statements result from mathematical mistakes or oversight or misuse of facts that existed when preparing the financial statements. II. a. b. c. d. Statement I only Statement II only Both statements Neither I or II 15. Which of the following statements is TRUE? I. II. Companies report changes in accounting estimates retrospectively. When it is impossible to determine whether a change in principle or change in estimate has occurred, the change is considered a change in estimate. a. b. c. d. Statement I only Statement II only Both statements Neither I or II 16. Which of the following statements is TRUE? I. II. Companies for a change in depreciation methods as a change in accounting principle. When companies make changes that result in different reporting entities, the change is reported prospectively. Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 a. b. c. d. Statement I only Statement II only Both statements Neither I or II 17. Counterbalancing errors do not include a. b. c. d. Errors that correct themselves in two years Errors that correct themselves in three years An understatement of purchases An overstatement of unearned revenue 18. An example of a correction of an error in previously issued financial statements is a change a. b. c. d. From the FIFO method of inventory valuation to the average method In the service life of plant assets, based on changes in the economic environment From the cash basis of accounting to the accrual basis of accounting In the tax assessment related to a prior period 19. Accounting changes are often made and the monetary impact is reflected in the financial statements of a company even though, in theory, this may be a violation of the accounting concept of a. b. c. d. Materiality Consistency Prudence Objectivity 20. On December 31, 2010, special insurance costs, incurred but unpaid, were not recorded. If these insurance costs were related to work in process, what is the effect of the omission on accrued liabilities and retained earnings in the December 31, 2011 statement of financial position? Accrued Liabilities a. b. c. d. No effect No effect Understated Understated Retained Earnings No effect Overstated No effect Overstated Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 PROBLEMS MULTIPLE CHOICE 1. Tan, Inc. is a calendar-year corporation whose financial statements for 2011 and 2012 included errors as follows: YEAR ENDING INVENTORY DEPRECIATION EXPENSE 2011 P 162,000 overstated P 135,000 overstated 2012 54,000 understated 45,000 understated Assume that purchases were recorded correctly and that no correcting entries were made at December 31, 2011, or at December 31, 2012. Ignoring income taxes, by how much should Tan’s retained earnings be retroactively adjusted at January 1, 2013? a. b. c. d. P144,000 increase P36,000 decrease P18,000 decrease P9,000 increase 2. On January 1, 2011, Richmond Corp. acquired a machine at a cost of P500,000. It is to be depreciated on the straight-line method over a five-year period with no residual value. Because of a bookkeeping error, no depreciation was recognized in Richmond’s 2011 financial statements. The oversight was discovered during the preparation of Richmond’s 2012 financial statements. Depreciation expense on this machine for 2012 should be a. b. c. d. P0 P100,000 P125,000 P200,000 3. Paulo Company began operations on January 1, 2011, and uses the FIFO method in costing its raw material inventory. Management is contemplating a change to the average method and is interested in determining what effect such a change will have on net income. Accordingly, the following information has been developed: FINAL INVENTORY FIFO Average NET INCOME (Computed under the FIFO method) 2011 P320,000 240,000 2012 P360,000 300,000 500,000 600,000 Based upon the above information, a change to the average method in 2012 would result in net income for 2012 of Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 a. b. c. d. P540,000 P600,000 P620,000 P660,000 4. The retained earnings account of Jeric Corporation is reproduced below: RETAINED EARNINGS Date 2009 Jan. 1 Dec. 31 2010 Jan. 10 Mar. 6 Dec. 31 2011 Jan. 9 Dec. 31 Item Debit Balance Net income for year Credit P 81,000 18,000 Dividends paid Stock sold – excess over par Net Loss for year P 15,000 Dividends paid Balance 15,000 89,800 P 131,000 32,000 11,200 P 131,000 The audit of the December 31, 2011, financial statements of the company reveals the following: a. Dividends declared on December 10, 2009 and 2010 had not been recorded in the books until paid. b. Improvements in buildings and equipment of P 9,600 had been charged to expense at the end of April 2008. Improvements are estimated to have an 8-year life. Antigua computes depreciation to the nearest month and uses the straight-line depreciation. c. The physical inventory of merchandise had been understated by P 3,000 at the end of 2009, and by P 4,300 at the end of 2010. d. Merchandise in transit and to which the company had title at December 31, 2010 and 2011 was not included in the year-end inventories. These shipments of P 3,800 and P 5,500 were recorded as purchases in January of 2011 and 2012, respectively. e. The company had failed to recognize supplies on hand of P 1,200 and P 2,500 at the end of 2010 and 2011, respectively. Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 f. The company had failed to recognize supplies on hand of P 1,200 and P 2,500 at the end of 2010 and 2011, respectively. g. The company reported a net loss of P 12,400 for the year ended December 31, 2011. What is the corrected net loss of Jeric Corporation for the year ended December 31, 2011? a. P 7,600 b. P 17,000 C. P 6,000 D. P 16,200 5. WAVSKI CO. Reported pretax incomes of P 505,000 and P 387,000 for the years ended December 31, 2010 and 2011, respectively. However, the auditor noted that the following errors had been made: a. Sales for 2010 included amounts of P 191,000 which had been received in cash during 2010, but for which the related goods were shipped in 2011. Title did not pass to the buyer until 2011. b. The inventory on December 31, 2010, was understated by P 43,200. c. The company’s accountant, in recording interest expense for both 2010 and 2011 on bonds payable, made the following entry to an annual basis: Interest Expense Cash 75,000 75,000 The bonds have a face value of P 1,250,000 and pay a nominal interest rate of 6%. They were issued at a discount of P 75,000 on January 1, 2010, to yield an effective interest rate of 7%. d. Ordinary repairs to equipment had been erroneously charged to the Equipment account during 2010 and 2011. Repairs of P 42,500 and P 47,000 had been incurred in 2010 and 2011, respectively. In determining depreciation charges, Chile applies a rate of 10% to the balance in the Equipment account at the end of the year. What is the corrected pretax income for 2011? a. P 488,992 b. P 480,042 C. P 484,292 D. P 575,392 6. On January 1, 2011, management of CPA COMPANY decided to make a revision in the estimates associated with its production equipment. The equipment was acquired in January 3, 2009, for P 800,000 and had been depreciated using straight-line method. At the date of acquisition, it had an estimated useful life of 10 years with an estimated salvage value of P 50,000. Management has determined that the equipment’s remaining useful life is 4 years and that it has an estimated residual value of P 60,000. What is the amount of depreciation expense that should be recognized in 2011 as a result of the changes in estimates? Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 a. P 147,200 b. P 75,000 C. P 125,000 D. P 150,000 7. The unaudited books of TRESE Company showed the following information: 2012 2013 Profit P195,000 P120,000 Inventory overstatement at year-end 36,000 Accrued expenses not recorded at year-end 40,000 Supplies inventory not recorded at year-end 15,000 What is the adjusted net income at December 31, 2013? a. 191,000 c. 221,000 b. 301,000 d. 229,000 8. On January 1, 2012, ALEX Corporation acquired a machine at a cost of P200,000. It was to be depreciated on the straight line method over a five year period with no residual value. Because of a bookkeeping error, no depreciation was recognized in Alex’s 2012 financial statements. The oversight was discovered during the preparation of Alex’s 2012 financial statements. What is the depreciation expense on this machine for 2013? a. 0 c. 80,000 b. 40,000 d. 120,000 9. SHIN Company began operations on January 1, 2012. Prior to any adjustments, the retained earnings account is reproduced below. 1/1/12 12/31/12 Profit for the year 8/31/13 Dividends paid 12/31/13 Profit for the year Debit - Credit 1,200,000 400,000 1,500,000 Balance 0 1,200,000 800,000 2,300,000 The company failed to properly recognize accruals and prepayments. Selected accounts revealed the following information: 2012 2013 Prepaid expenses 80,000 60,000 Accrued expenses 25,000 40,000 Unearned income 110,000 50,000 Accrued income 70,000 100,000 A. What is the adjusted net income at December 31, 2012? a. 1,175,000 c. 1,205,000 b. 1,265,000 d. 1,215,000 B. What is the adjusted net income at December 31, 2013? a. 1,055,000 c. 1,555,000 b. 1,155,000 d. 1,955,000 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 C. What is the adjusted retained earnings at December 31, 2013? a. 2,355,000 c. 2,385,000 b. 2,370,000 d. 2,570,000 10. On December 30, 2013, FINE Company sold merchandise for 75,000 to Wise Company. The terms of the sale were n/30, FOB shipping point. The merchandise was shipped on December 31, 2013, and arrived at Wise on January 2, 2014. Due to clerical error, the sale was not recorded until January 2014 and the merchandise, sold at a 25% mark up on cost, was included in Fine’s inventory at December 31, 2013. As a result, Fine’s cost of goods sold for the year ended December 31, 2013 was? a. Understated by 15,000 c. Understated by 60,000 b. Understated by 75,000 d. Overstated by 60,000 11. SEY Company has been using accrual basis of accounting. However, an examination of the records reveals that some expenses and revenues have been handled on a cash basis by the inexperienced bookkeeper of the company. The statements of comprehensive income prepared by the bookkeeper reported P145,000 profit for 2012 and P185,000 profit for 2013. Further review of the records reveals that the following items were handled improperly. i. ii. iii. Rent of 6,500 was received from a lessee on December 23, 2012 and credited to income. This amount represents rent for 2013. Invoices for office supplies purchased were charged to expense accounts upon receipt. Inventories of supplies on hand at the end of each year have been ignored and no adjusting entry has been made. Office supplies inventories at the end of 2011, 2012 and 2013 were P6,500, P3,700 and P7,100, respectively. Salaries payable at the end of each year was consistently omitted from the records and were recorded as expense when paid in the following year. Accrued salaries at the end of 2011, 2012 and 2013 were P5,500, P7,500 and P4,700, respectively. A. Adjusted net income for 2012. a. 133,700 b. 113,700 B. Adjusted net income for 2013. a. 190,600 b. 207,100 c. 148,700 d. 146,700 c. 197,700 d. 187,700 12. During 2013, Cadbury Company discovered that the ending inventories reported on its financial statement were incorrect by the following amounts: 2011—60,000 understated; 2012—75,000 overstated. Cadbury Company uses the periodic inventory system to ascertain year-end quantities that are converted to peso amounts using FIFO cost method. A. By how much would retained earnings at January 1, 2013 be misstated prior to any adjustments for these errors and ignoring income taxes? Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 a. b. c. d. 75,000 overstated 75,000 understated 15,000 overstated 15,000 understated B. Effect in 2012 net income a. b. c. d. 135,000 overstated 60,000 understated 60,000 overstated 135,000 understated 13. During 2013, Kerr Company determined that machinery previously depreciated over a sevenyear life had a total estimated useful life of only five years. An accounting change was made in 2013 to reflect the change in estimate. If the change had been made in 2012, accumulated depreciation would have been P800,000 on December 31, 2012, instead of P600,000. As a result of this change, the 2013 depreciation expense was P50,000 greater. The income tax rate was 30%. What should be reported in Kerr’s income statement for the year ended December 31, 2013 as the cumulative effect on prior years of changing the estimated useful life of the machinery? a. b. c. d. 0 130,000 150,000 200,000 14. On January 1, 2008, Brazilia Company purchased for P4,800,000 a machine with a useful life of ten years and a residual value of P200,000. The machine was depreciated by the doubledeclining balance method and the carrying amount of the machine was P3,072,000 on December 31, 2009. Brazilia changed to straight line method on January 1, 2010. The residual value did not change. What should be the depreciation expense on this machine for the year ended December 31, 2010? a. b. c. d. 287,200 384,000 460,000 359,000 15. On January 1, 2009, Kevin Company purchased a machine for P2,750,000. The machine was depreciated using the sum of year’s digits method based on a useful life of 10 years with no residual value. On January 1, 2010, Kevin Company changed to the straight line method of depreciation. Kevin Company can justify the change. What is the depreciation of the machine for 2010? Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 a. b. c. d. 180,000 220,000 250,000 275,000 16. On January 1, 2006, Roma Company purchased heavy duty equipment for P4,000,000. On the date of installation, it was estimated that the equipment has a useful life of 10 years and a residual value of P400,000. On January 1, 2010, the entity decided to review the useful life of the equipment and its residual value and technical experts were consulted. The experts have determined that the useful life of the equipment was 12 years from the date of acquisition and its residual value was P460,000. What is the depreciation of the equipment for 2010? a. b. c. d. 175,000 262,500 360,000 300,000 17. Universal Company failed to accrue warranty cost of P100,000 in its December 31, 2009 financial statements. In addition, a change from straight line to accelerated depreciation made at the beginning of 2010 resulted in a cumulative effect of P60,000 on Universal’s retained earnings. What amount before tax should Universal report as prior period error in 2010? a. b. c. d. 100,000 160,000 60,000 0 18. On January 1, 2009, Aker Company acquired a machine at a cost of P2,000,000. The machine is depreciated on the straight line method over a five-year period with no residual value. Because of a bookkeeping error, no depreciation was recognized in Aker’s 2009 financial statements. The oversight was discovered during the preparation of Aker’s 2010 financial statements. What is the depreciation expense on the machine for 2010? a. b. c. d. 800,000 400,000 500,000 0 19. The draft financial statements for Savior Company for the year ended December 31, 2010 have been prepared. A final review of the draft reveals an overvaluation of the ending inventory of P2,000,000 on December 31, 2009. Further investigation shows that there was an overvaluation of ending inventory on December 31, 2008 of P1,200,000. Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 What adjustment should be made to the profit for the year ended December 31, 2009 presented as the comparative figure in the 2010 financial statements? a. b. c. d. 2,000,000 decrease 1,200,000 decrease 800,000 decrease 0 20. After the issuance of its 2009 financial statements, Narra Company discovered a computational error of P150,000 in the calculation of its December 31, 2009 inventory. The error resulted in a P150,000 overstatement in the cost of goods sold for the year ended December 31, 2009. In October 2010, Narra paid the amount of P500,000 in settlement of litigation instituted against it during 2009. Ignore income tax. In the 2010 financial statements, what is the adjustment of the retained earnings on January 1, 2010? a. b. c. d. 150,000 credit 350,000 debit 500,000 debit 650,000 credit 21. The audited income statement of Manuel Co. shows a net income of P350000 for the year ended December 31, 2012. Adjustments were made for the following errors: i. ii. iii. December 31, 2011, inventory overstated by P45000. December 31, 2012, inventory understated by P75000. A P20000 customer’s deposit received in December 31, 2012, was credited to sales in 2012. The goods were actually shipped in January 2013. What is the unadjusted net income of Manuel Co. for the year ended December 31, 2012? a. P340000 c. P400000 b. P468000 d. P250000 22. On January 1, 2012, management of Danzelle Company decided to make a revision in the estimates associated with its production equipment. The equipment was acquired on January 3, 2010 for P1600000 and had been depreciated using a straight-line method. At the date of acquisition, it had an estimated life of 10 years with an estimated salvage value of P100000. Management has determined that the equipment’s remaining useful life is 4 years and that it has an estimated residual value of P120000. What is the amount of depreciation expense that should be recognized in 2012 as a result of the changes in estimate? a. P150000 b. P250000 c. P295000 d. P300000 23. In the past, Perez Company has depreciated its computer hardware using the straight-line method. The computer hardware has a 10 % salvage value and an estimated useful life of 5 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 years. As a result of rapid advancement in information technology, management of Perez has determined that it receives most of the benefits from its computer facilities in the first few years of ownership. Hence, as of January 1, 2012 Perez purposes changing to the sum-of-years’-digits method for depreciating its computer hardware. The following computer purchase was made by Perez at the beginning of the year. 2011 60000 How much depreciation expense was recorded by Perez in 2012? a. P 17280 c. P43200 b. P 10800 d. P23060 24. The December 31 year-end financial statements of Tarel Company contained the following errors: December 31, 2011 December 31, 2012 Ending inventory P 48000 understated P 40500 overstated Depreciation expense P 11500 understated -------An insurance premium of P 330000 was prepaid in 2011 covering the years 2011, 2012 and 2013. The entire amount was charged to expense in 2011. In addition, on December 31, 2012, a fully depreciated machinery was sold for P 75000 cash, but the sale was not recorded until 2013. There were no other errors during 2011 and 2012, and no corrections have been made for any error. Ignore income tax effects. What is the total effect of the errors on Tarel’s 2012 net income? a. P 27500 overstatement c. P 192500 understatement b. P 177500 understatement d. P 123500 overstatement 25. On January 1, 2010, Keith Corporation acquired machinery at a cost of P600,000. Keith adopted the straight-line method of depreciation for this machine and had been recording depreciation over an estimated useful life of ten years, with no residual value. At the beginning of2013, a decision was made to change to the double-declining balance method of depreciation for this machine. A. Assuming a 30% tax rate, the effect of this accounting change on beginning retained earnings, is a. P67,200 b. P0 c. P78,960 d. P112,800 B. The amount that Keith should record as depreciation expense for 2013 is a. P60,000 b. P84,000 c. P120,000 d. P0 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 COMPREHENSIVE PROBLEMS I. Tan Corporation’s current assets and liabilities section of the statement of financial position as of December 31, 2010 appear as follows: Current assets Cash Accounts Receivable Less allowance for doubtful accounts Inventories Prepaid expenses Total current assets P1,200,000 P2,670,000 210,000 Current liabilities Accounts payable Notes payable Total current liabilities 2,460,000 5,130,000 270,000 P9,060,000 P1,830,000 2,010,000 P3,840,000 The following errors in the corporation’s accounting have been discovered: a. January 2011 cash disbursements entered as of December 2010 included payment of accounts payable in the amount of P1,170,000, on which a cash discount of 2% was taken. b. The inventory included P810,000 of merchandise that have been received at December 31 but for which no purchase invoices have been received or entered. Of this amount P360,000 had been received on consignment; the remainder was purchased f.o.b. destination, terms 2/10, n/30. c. Sales for the first four days in January 2011 in the amount of P900,000 were entered in the sales book as December 31, 2010. Of these, P645,000 were sales on account and the remainder were cash sales. d. Cash, not including cash sales, collected in January 2011 and entered as of December 31, 2010, totaled P1,059,720. Of this amount, P699,720 was received on account after cash discounts of 2% had been deducted; the remainder represented the proceeds of a bank loan. QUESTIONS: Based on the above and the result of your audit, determine the following: 1. Adjusted cash balance as of December 31, 2010 2. Adjusted accounts receivable balance as of December 31, 2010 3. Adjusted accounts payable balance as of December 31, 2010 4. Adjusted working capital as of December 31, 2010 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 II. Speed R Corporation reported net income as follows: 2011 15,000,000 2012 20,000,000 2013 28,000,000 An audit of the records disclosed the following: Accounts receivable instead of notes receivable was debited in 2013. 200,000 Purchases account was debited in 2013 instead of office supplies. 50,000 The physical inventory on December 31, 2011 was overstated. 100,000 The physical inventory on December 31, 2012 was understated. 150,000 Advances to suppliers were recorded as purchases but the merchandise was received in subsequent year: 2011 300,000 2012 400,000 Advances from customers recorded as sales but the goods were delivered in the following year: 2011 250,000 2012 500,000 Insurance premium for three years paid in 2011 was charged entirely to expense in 2011. 150,000 Salaries accrued not recorded: 2011 300,000 2013 600,000 Rent for two years received in 2012 was entirely credited to income. Unrecorded accrued interest receivable: 2012 2013 100,000 100,000 250,000 Improvements on building had been charged to expense on January 1, 2012. Improvements have a life of five years. 1,000,000 On January 1, 2012, an equipment costing 40,000 was sold for 20,000. At the date of sale, the equipment had an accumulated depreciation of 25,000. The cash received was recorded as other income in 2012. What is the adjusted net income for (5.) 2011, (6.) 2012, and (7.) 2013? 8. What is the retained earnings for 2013? Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 III. You were engaged by Lanao Company to audit its financial statements for the first time. In examining the books, you found out that certain adjustments had been overlooked at the end of 2009 and 2010. You also discovered that other items had been improperly recorded. These omissions and other failures for each year are summarized below: 12/31/10 12/31/09 Salaries Payable 780,000 873,600 Interest Receivable 213,000 259,200 Prepaid Insurance 307,800 384,000 561,000 470,400 522,000 564,000 Advances from customers (collections from Customers had been recorded as sales but Should have been recognized as advances From customers because goods were not Shipped until the following year) Machinery (Capital expenditures had been Recorded as repairs but should have been Charged to Machinery; the depreciation Rate is 10% per year, but depreciation in the Year of expenditure is to be recognized at 5%) QUESTIONS: 9. What is the net effect of the errors on the 2009 profit? 10. What is the net effect of the errors on the 2010 profit? 11. What is the net effect of the errors on the company’s working capital at December 31, 2010? 12. What is the net effect of the errors on the balance of the company’s retained earnings at December 31, 2010? IV. The following information pertains to Molina Company’s depreciable assets: 1. Machine X was purchased for P150000 on January 1, 2008. The entire cost was expensed in the year of the acquisition. The estimated useful life of this machine is 15 years with no residual value. 2. Machine Y cost P525000 and was acquired on January 1, 2009. On the acquisition date, the expected useful life was 12 years with no residual value. The straight-line method depreciation Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 was made. On January 2, 2013, it was estimated that the remaining life of the asset would be 4 years and that there would be a P25000 residual value. 3. A building was purchased on January 3, 2010, for P3000000. The building was expected to have a useful life of 20 years with no residual value. The straight-line depreciation method was used. On January 1, 2013, a change was made to the sum-of-the-years’-digits method of depreciation. No change was made to the estimated useful life and residual value of the building. The adjusting entry on January 1, 2013, relative to machine X should include a credit to a. Accumulated depreciation of P60000 b. Retained earnings of P100000 c. Machinery of P150000 d. No adjusting entry is necessary 13. What is the carrying value of machine Y on January 1, 2013? 14. What is the depreciation expense of machine Y for 2013? 15. What is the book value of the building at December 31, 2012? 16. What is the book value of the building on December 31, 2013? V. Madam Corporation reported the following amounts of net income for the years ended December 31, 2010, 2011 and 2012: 2010 2011 2012 P127,000 150,000 128,500 You are performing the audit for the year ended December 31, 2012. During your examination, you discover the following errors: a. As a result of errors in the physical count, ending inventories were misstated as follows: December 31, 2011 P14,000 understated December 31, 2012 P23,000 overstated b. On December 29, 2012, Madam recorded as purchase merchandise in transit which costP15,000. The merchandise was shipped FOB destination and had it arrived by December 31. The merchandise was not included in the ending inventory. c. Madam records sales on the accrual basis but failed to record sales on account made near the end of each year’s follows: 2010 2011 2012 P4,000 5,000 3,500 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 d. The company failed to record accrued office salaries as follows: December 31, 2010 P10,000 December 31, 2011 14,000 e. On March 1, 2011, a 10% stock dividend was declared and distributed. The par value of the shares amounted to P10,000 and market value was P13,000. The stock dividend was recorded as follows: Miscellaneous expense 13,000 Ordinary share capital 10,000 Retained earnings 3,000 f. On July 1, 2011, Madam acquired a three-year insurance policy. The three- year premium of P6000 was paid on that date, and the entire premium was recorded as insurance expense. g. On January 1, 2012, Madam retired bonds with book value of P120,000 for P106,000. The gain was incorrectly deferred and is being amortized over 10 years as a reduction of interest expense on other outstanding obligations. 17. What is the adjusted net income for the year ended December 31, 2010? 18. What is the adjusted net income for the year ended December 31, 2011? 19. What is the adjusted net income for the year ended December 31, 2012? 20. What is the adjusting entry should be made on December 31, 2012 to correct the error described in item B? Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 THEORIES: Answers: 1. B 6. D 11.C 16.D 2. C 7. C 12.D 17.B 3. C 8. D 13.A 18.C 4. D 9. B 14.C 19.B 5. C 10.B 15.B 20.C SOLUTIONS: MULTIPLE CHOICES 1. A Understatement of 2012 ending inventory Overstatement of 2011 depreciation expense Understatement of 2012 depreciation expense 2. B Depreciation Expense Retained Earnings Accumulated Depreciation RETAINED EARNINGS P54,000 increase 135,000 increase (45,000) decrease P144,000 increase P100,000** 100,000* P200,000 Acquisition cost P500,000 Useful life / 5 years Depreciation expense for 2011 P100,000* (Since the book for 2011 is closed, the understatement of depreciation expense will be adjusted to the Retained Earnings account) Depreciation expense for 2012 3. 4. P100,000** C Net income for 2012 under FIFO method Change in final inventory from FIFO to average method (P360,000 – 300,000) Net income for 2012 under FIFO method D Reported net income (loss) P600,000 60,000 P540,000 P (12,400) Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 Omission of depreciation Understatement of physical inventory at Dec. 31, 2010 Overstatement of sales commissions expense (P 2,100 – P1,700) Overstatement of supplies expense (P2,500 – P1,200) Corrected net income (loss) 5. 400 1,300 P (16,200) 2010 2011 P 505,000 P 387,000 (191,000) 191,000 43,200 (43,200) (7,250) ( 7,758) (42,500) (47,500) 4,250 8,950 P 311,700 P 488,992 A Cost of equipment Less: Accumulated depreciation, Dec. 31, 2010 (P 75,000 x 2) Book value, Jan. 1, 2010 Less: Revised salvage value Remaining depreciable cost Divide by revised useful life Revised annual depreciation 7. (4,300) A Pretax income Sales revenue erroneously recognized in 2010 Understatement of 2010 ending inventory Understatement of bond interest expense Ordinary repairs erroneously capitalized Overstatement of depreciation Corrected pretax income 6. (1,200) P 800,000 150,000 650,000 60,000 590,000 ÷ 4 yrs. P 147,500 B 2012 195,000 (36,000) (40,000) Unadjusted profit Inventory -2012 overstated Accrued expenses not recorded Supplies not recorded ADJUSTED NET INCOME 119,000 8. B Machine= 200,000/5ys= 40,000 9. (A.) D; (B.)B; Unadjusted balance Prepaid expenses Accrued expenses 2013 210,000 36,000 40,000 15,000 301,000 (C.)B 2012 1,200,000 80,000 (25,000) 2013 1,500,000 (80,000) (60,000) 25,000 (40,000) Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) RE 1,500,000 (60,000) (40,000) lOMoARcPSD|9190468 Unearned income (110,000) Accrued income 70,000 Dividends paid ADJUSTED NET INCOME 10. 110,000 (50,000) (70,000) 100,000 400,000 1,155,000 (400,000) 1,215,000 (50,000) 100,000 2,370,000 C The December 31, 2013 inventory was overstated. Therefore, cost of goods sold for 2013 was understated by 60,000 (75,000/125%) 11. (A.) A; (B.)C 2012 145,000 (6,500) Unadjusted income Unearned rent Office supplies not recorded 2013 185,000 6,500 (6,500) (3,700) 7,100 3,700 Accrued Salaries 5,500 (7,500) 133,700 12. (A.) A ; 7,500 (4,700) 197,700 (B.) B Inventor - understated -overstated 2012 60,000 _____ 2013 Retained Earnings (60,000) (75,000) (75,000) 60,000 13. A The change in estimated useful life is a change in accounting estimate. Accordingly, there is no cumulative effect. 14. D Depreciation for 2010 (3,072,000 – 200,000 / 8) 359,000 15. C SYD (1 + 2 + 3 + 4 + 5 + 6 + 7 + 8 + 9 + 10) 55 Cost – January 1, 2009 2,750,000 Accumulated Depreciation – January 1, 2010 (10/55 x 2,750,000) (500,000) Carrying Amount – January 1, 2010 2,250,000 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 Straight line depreciation for 2010 (2,250,000 / 9 years remaining) 16. 250,000 B Cost – January 1, 2006 4,000,000 Accumulated depreciation – January 1, 2010 (4,000,000 – 400,000 / 10 x 4) 1,440,000 Carrying amount – January 1, 2010 2,560,000 Depreciation for 2010 (2,560,000 – 460,000/8) 17. 262,500 A Only the unrecorded warranty cost of P100,000 on December 31, 2009 should be accounted for as a prior period error. The change from straight line to accelerated depreciation is accounted for as a change in accounting estimated and therefore should be treated currently and prospectively. 18. B Depreciation for 2010 (2,000,000 / 5) 400,000 The under depreciation of P400,000 in 2009 is reported as a prior period error in the statement of retained earnings. 19. C Overvaluation of 12/31/2009 inventory Overvaluation of 12/31/2008 inventory Net decrease in 2009 profit 20. A Inventory – January 1, 2010 Retained Earnings 150,000 150,000 Litigation loss Cash 21. (2,000,000) 1,200,000 (800,000) 500,000 500,000 D Unadjusted net income December 31, 2011, inventory overstated December 31, 2012, inventory understated Customer’s deposit recognized as sales revenue Adjusted net income P250000 45000 75000 ( 20000) P350000 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 22. C Cost of equipment Less: Accumulated depreciation,12/31/2011 ( 150000 x 2 ) Book value, 1/1/2012 Less: Revised salvage value Remaining depreciable cost Divide by revised useful life Revised annual depreciation 23. 300000 1300000 120000 1180000 4 P 295000 A Cost Less: Accumulated depreciation (P60000 x 90% / 5) Book value, January 1, 2012 Less: Salvage value (10% x 60000) Remaining depreciable cost SYD rate [4 x (4+1)/2] Depreciation expense in 2012 24. P1600000 P60000 10800 49200 6000 43200 x 4/10 P 17280 D Understatement of 2011 ending inventory Overstatement of 2012 ending inventory Prepaid insurance charged to expense in 2012 (330000/3) Unrecorded sale of fully depreciated machinery in 2012 Total effect of errors on net income 25. (A.) B; P 48000 40500 110000 (75000) P 123500 (B.) C Cost Accumulated Depreciation (600,000 x 3/10) Carrying Value Depreciation expense P600,000 180,000 420,000 X 2/7 P120,000 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 COMPREHENSIVE PROBLEMS I. Question No.1 Unadjusted cash balance January cash payments (P1,170,000 * .98) January cash sales (P900,000 – P645,000) January cash collections and load proceeds Adjusted cash balance P1,200,000 1,146,600 (255,000) (1,059,720) P1,031,880 Question No.2 Unadjusted accounts receivable January sales on account January collections on AR (P699,720/.98) Adjusted accounts receivable P2,670,000 (645,000) 714,000 P2,739,000 Question No.3 Unadjusted accounts payable January payments on AP Unrecorded purchases (P810,000 – P360,000) Adjusted accounts payable P1,830,000 1,170,000 450,000 P3,450,000 Question No.4 Current assets: Cash P1,031,880 Accounts receivable 2,739,000 Allowance for doubtful accounts (210,000) Inventories (P5,130,000 – P360,000) 4,770,000 Prepaid expenses 270,000 Less current liabilities: Accounts payable 3,450,000 Notes payable [P2,010,000 – (P1,059,720 – P699,720)] 1,650,000 Working capital P8,600,000 5,100,000 P3,500,880 II. 2011 2012 2013 Retained 1,500,000 2,000,000 2,800,000 (10,000) 10,000 15,000 (15,000) (15,000) (30,000) 40,000 (40,000) (40,000) Earnings Net income a. No effect b. No effect c. 2011 inventory overstated d. 2012 inventory understated e. Advances recorded as purchases 2011 2012 30,000 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) lOMoARcPSD|9190468 f. Advances recorded as sales 2011 2012 g. Insurance premium-2009 h. Salaries accrued unrecorded 2011 2013 i. Rent income j. Interest receivable unrecorded 2012 2013 k. Improvements DR to expense Depreciation l. Overstatement of other income (25,000) 10,000 25,000 (50,000) (5,000) (30,000) 30,000 (5,000) 10,000 50,000 (5,000) 50,000 (5,000) (60,000) 5,000 5,000 (10,000) 25,000 (10,000) 100,000 (100,000) (20,000) (20,000) 20,000 _ _ 15,000__ 15,000 (5.)1,475,000 (6.) 2,105,000 (7.) 2,730,000 (8.) 80,000 III. Salaries Payable 2009 2010 Interest Receivable 2009 2010 Prepaid Insurance 2009 2010 Advances from customers 2009 2010 Machinery 2009 Profit 2009 Profit 2010 WC 12/31/10 RE 12/31/10 873,600 (873,600) 780,000 780,000 780,000 259,200 (213,000) (213,000) (213,000) 384,000 (307,800) (307,800) (307,800) (470,400) 561,000 561,000 561,000 (259,200) (384,000) 470,400 (564,000) 28,200 2010 Over (under) 165,000 (564,000) 84,600 (522,000) 26,100 56,400 (522,000) 26,100 (320,100) 820,200 IV. Machinery X Accumulated depreciation-Machinery (P150000x 5/15) Retained earnings 150000 50000 100000 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com) (155,100) lOMoARcPSD|9190468 Cost of machine Y Less: Accumulated depreciation (P525000x 4/12) Carrying value, Dec. 31, 2012 175000 P350000 Carrying value, Dec. 31, 2012 Less: Salvage value Remaining depreciable cost Divided by revised remaining life Depreciation for 2013 P350000 25000 325000 4 years P 81250 Cost of building Less: Accumulated depreciation, 12/31/12 (P3000000x3/20) Book value of building, Dec. 31, 2013 P3000000 450000 Book value of building, Dec. 31, 2012 Less: Depreciation for 2013 (P2550000x17/153) Book value of building, Dec. 31, 2013 P525000 P2550000 P2550000 283333 P2266667 SYD= 17[(17+1)/2]= 153 V. Reported net income a. 2011 ending inventory understated 2012 ending inventory overstated b. 2013 purchase recorded in 2012 c. Unrecorded sales on account: 2010 2011 2012 d. Unrecorded accrued salaries: 2010 2011 e. Stock dividend charged to expense f. Insurance premium expensed g. Deferred gain on bond retirement Amortization of deferred gain Adjusted net income ADJUSTING ENTRY: Accounts payable Purchases 2010 P127,000 4,000 (10,000) P121,000 2011 P150,000 14,000 - 2013 P128,500 (14,000) (23,000) 15,000 (4,000) 5,000 - (5,000) 3,500 10,000 (14,000) 13,000 5,000 P179,000 14,000 (2,000) 14,000 (1,400) P129,600 15,000 15,000 Downloaded by Meisha Guzman (bonjourchocolatte@gmail.com)