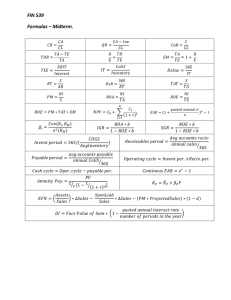

CHAPTER 18 FINANCIAL STATEMENT ANALYSIS FINANCIAL STATEMENT ANALYSIS • Analysing financial statements involves evaluating three characteristics of a company: Who needs to know: 1. its liquidity - short-term creditor 2. its profitability – long-term creditor, investors, shareholders. 3. its solvency -long-term creditors, investors, shareholders COMPARATIVE ANALYSIS • Three types of comparisons: 1. Intracompany basis – focused within company 2. Intercompany basis – focuses on you vs. competition 3. Industry averages - focuses on your industry 1. Intracompany Basis • Compares an item or account on a financial statement within the company in a given year with the same item or relationship in prior years. – ie. Cash as a % of total current assets for the last three years. • Useful for detecting changes in financial relationships and significant trends within a company 2. Intercompany Basis • Compares an item within the company in a given year with the same item in one or more competing companies. – ie. Walmart’s total sales compared to HBCs total sales • Useful for understanding a company’s competitive position 3. Industry Averages • Compares an item of a company with industry averages (or norms) • Averages found in annual publications such as: – The Financial Post’s Industry Reports – Statistics Canada • Financial Performance Indicators for Canadian Business. • Provides info about a company’s relative performance within the industry. COMPARATIVE ANALYSIS • Three tools: 1. Horizontal analysis (Trend Analysis) Evaluates a series of financial statement data over a period of years. Used primarily in intracompany comparisons 2. Vertical analysis (Common Size Analysis) Evaluates financial statement data by expressing each item in a financial statement as a percentage for the same period of time Used in both intracompany and intercompany comparisons. 3. Ratio analysis Expresses the relationship among selected items of financial statement data. Used in intracompany, intercompany, and industry average comparisons. HORIZONTAL ANALYSIS Determines an increase or decrease that has taken place. May be expressed as either a $ amount or as a % percentage. Current year amount — Base year amount ——————————————————————— Base year amount Change since base period ANY COMPANY INC. Assumed Net Sales For the Year Ended December 31 (in millions 2003 $ 6,562 127% 2002 $ 6,295 121% ) 2001 2000 1999 $ 6,190 119% $ 5,786 112% $ 5,181 100% For 2003: 6562.8 / 5181.4 = 1.266 = 127% VERTICAL ANALYSIS • Expresses each item in a financial statement as a percent of a base amount ANY COMPANY, INC. Condensed Balance Sheets (Partial) December 31 (in millions) Assets Current assets Capital assets Other assets Total assets 2002 Amount $1,496.5 2,888.8 666.2 $5,051.5 Percent 29.6 57.2 13.2 100.0% 2001 . Amount Percent $1,467.7 30.1 2,733.3 56.9 636.6 13.0 $4,837.6 100.0% RATIO ANALYSIS • Liquidity Ratios – Measure short-term ability of the enterprise to pay its maturing obligations (current liabilities) and to meet unexpected needs for cash. • Profitability Ratios – Measure the income or operating success of an enterprise for a given period of time. • Solvency Ratios – Measure the ability of the enterprise to survive over a long period of time. Ratio Analysis Can be expressed in 3 ways: Example: Current Assets are $33.4 million and Current Liabilities are $13.8 million. 1. 2. 3. By Percentage: Current assets are 240% of current liabilities. By Rate: Current assets are 2.4 times greater than current liabilities. By Proportion: The relationship of current assets to liabilities is 2.4 : 1 LIQUIDITY RATIOS • • • • • • • Current ratio Acid test ratio Cash current debt coverage ratio Receivables turnover Collection period Inventory turnover Days sales in inventory CURRENT RATIO Working Capital Ratio Current Ratio = Current Assets Current Liabilities • Measures short-term debt-paying ability • Limitations: Portion of CA may be tied up in uncollectable A/R’s or slow moving inventory. • Useful when comparing to industry averages (Discussed in Chapter 4) ACID TEST (QUICK) RATIO Acid test ratio = Cash + temporary investments + net receivables Current liabilities • • • • • Measures immediate term debt-paying ability Generally a 1 : 1 is adequate. Does not include Inventory and Prepaids Compare it to the industry average. Limitations: Year end account balances may not represent position during most of the year. RECEIVABLES TURNOVER Receivables turnover = Net credit sales Average net receivables • Measures liquidity of receivables – the number of times receivables are collected during the fiscal period. Net Credit Sales = Net Sales – Cash Sales Net Sales = Total Sales – Sales Returns and Discounts. Average Net Receivables = Beginning Net Receivables + Ending Net Receivables 2 (Discussed in Chapter 9) COLLECTION PERIOD Collection period = 365 days Receivables turnover • Measures number of days receivables are outstanding. (The number of days it takes to collect the receivables.) • Used to assess a company’s credit and collection policies. • Collection period should not exceed the credit term period (net 30). (Discussed in Chapter 9) INVENTORY TURNOVER Inventory turnover = Cost of goods sold Average inventory • Measures liquidity of inventory – the average number of times the inventory is sold during the period. • Average Inventory = Beginning Inventory + Ending Inventory 2 (Discussed in Chapter 5) DAYS SALES IN INVENTORY • Measures number of days inventory is on hand or average selling time. Days in inventory = 365 days Inventory turnover (Discussed in Chapter 5) PROFITABILITY RATIOS Measure income or operating success for a specific period of time Profitability impacts company’s ability to obtain debt and equity financing. • • • • • • Profit margin Gross profit margin Cash return on sales Asset turnover Return on assets Return on common shareholders’ equity • • • • • • Book value per share Cash flow per share Earnings per share (EPS) Price-earnings (PE) ratio Payout ratio Dividend yield PROFIT MARGIN • Measures net income generated by each dollar of sales Profit margin = Net income Net sales (Discussed in Chapter 5) GROSS PROFIT MARGIN • Indicates a company’s ability to maintain its selling price above its cost of goods sold. Gross profit margin = Gross profit Net sales (Discussed in Chapter 5) CASH RETURN ON SALES • Measures net cash flow generated by each dollar of sales • Measures profit margin based on cash basis of accounting. Does not include sales in A/R. Cash return on sales = Net cash provided by operating activities Net sales (Discussed in Chapter 18) ASSET TURNOVER • Measures how efficiently assets are used to generate sales indicates the dollar of sales produced by each dollar of assets. Asset turnover = Net sales Average total assets (Discussed in Chapter 10) RETURN ON ASSETS • Measures overall profitability of assets Return on assets = Net income Average total assets (Discussed in Chapter 10) RETURN ON COMMON SHAREHOLDERS’ EQUITY • Measures profitability of common shareholders’ investment Return on common shareholders’ equity = Net income Average common shareholders’ equity Common Shareholder’s Equity = Total Shareholder’s Equity – Preferred Shares (Discussed in Chapter 14) BOOK VALUE PER SHARE • Measures the equity (net assets) per common share Book value per share = Common shareholders’ equity Number of common shares (Discussed in Chapter 14) CASH FLOW PER SHARE • Measures the net cash flow per common share Cash flow per share = Net cash provided by all activities Number of common shares • Don’t need to know (Discussed in Chapter 18) EARNINGS PER SHARE (EPS) • Measures net income earned on each common share • This is only meaningful when used as an intracompany comparison Earnings per share = Net income Number of common shares issued (Discussed in Chapter 15) PRICE-EARNINGS (PE) RATIO • Measures relationship between market price per share and earnings per share • Reflects investors’ assessment of a company’s future earnings. • Share sold for “ratio” times the amount that was earned on each share. Price-earnings ratio = Share price Earnings per share (Discussed in Chapter 15) PAYOUT RATIO • Measures % of earnings distributed in the form of cash dividends Payout ratio = Cash dividends Net income • Companies with high growth rate usually have low payout ratios because they reinvest most of their net income in the business. • Companies with stable earnings usually have high payout ratios. (Discussed in Chapter 15) DIVIDEND YIELD • Measures rate of return earned from dividends Dividend yield = Cash dividends per share Share price Cash Dividend Per Share = Cash Dividend / # of Common Shares (Discussed in Chapter 15) SOLVENCY RATIOS Measures a company’s ability to survive over a long period of time. Ability to pay interest on long-term debt and repay principal when it comes due. Ratios include: • Debt to total assets • Interest coverage • Cash interest coverage • Cash total debt coverage DEBT TO TOTAL ASSETS • Measures % of total assets provided by creditors Debt to total assets = Total liabilities Total assets (Discussed in Chapter 16) INTEREST COVERAGE • Measures ability to meet interest payments as they come due based on accrual method. Interest coverage = Income before interest expense and income tax expense (EBIT) Interest expense • The higher the number the better (Discussed in Chapter 16) CASH INTEREST COVERAGE • Measures cash available to meet interest payments as they come due (cash basis) Cash interest coverage = Income before interest expense, income tax expense, and amortization expense (EBITDA) Interest expense (Discussed in Chapter 16) CASH TOTAL DEBT COVERAGE • Measures long-term debt-paying ability (cash basis) without having to liquidate assets Cash total debt coverage ratio = Net cash provided by operating activities Average total liabilities • If CTDC was .2 times, then it would mean that it would take five years (1/.2) to generate enough cash to pay off all its liabilities. (Discussed in Chapter 18)