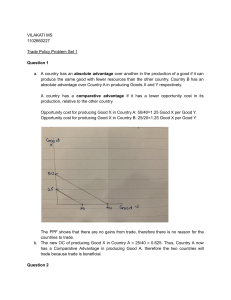

ECONOMICS AS AN APPLIED SCIENCE Applied Economics It is the study of economics in relation to the real world situations, as opposed to the theory of economics. It is the application of economic principles and theories to real situations, and trying to predict what the outcomes might be. Applied economics involves economists taking generally accepted theory and applying those theories to something that is happening in the real world, with an eye toward determining what can reasonably be expected to happen next. Applied Economic Application Applying economic theories to current economic conditions can be extremely helpful for three key reasons. First, applying economics to the status of the economy of a company, a household or a country helps to sweep aside all attempts to dress up the situation so that it will appear to be worse or better than it actually is. Second, applied economics acts as a mechanism to determine what steps can reasonably be taken to improve the current economic situation. Examining each aspect of the current economic condition will often yield sound ideas on ways to maintain aspects that are working at a reasonable rate of efficiency and strengthen areas where the performance is weak. Last, applied economics can teach valuable lessons on how to avoid the recurrence of a negative situation, or at last minimize the impact. What is Econometrics? Econometrics is the application of statistical and mathematical theories to economics for the purpose of testing hypotheses and forecasting future trends. Econometrics takes economic models and tests them through statistical trials. The results are then compared and contrasted against real-life examples. Econometrics can be subdivided into two major categories: theoretical and applied. Econometrics uses tools such as frequency distributions, probability and probability distributions, statistical inference, simple and multiple regression analysis, simultaneous equation models and time series methods. Some problems faced by Economic System 1. What to produce? 2. How to Produce 3. For whom shall goods and services be produced? 4. Are the countries resources being utilized, or some of them are lying idle and unemployed? 5. Is the economy’s capacity to produce goods growing or remaining the same overtime? THE ECONOMIC SYSTEM Traditional Economy In traditional economy, everything is mostly based on what is popular, production responds to what is in demand from the people. An example of this would be in the prehistoric times where farmers grazed animals and produced food. In some parts of the Philippines, this type of economic system still permeates. Some families or tribes are self-sufficient. They produce goods and services only for their own consumption. If ever there are surpluses in their goods, they resort to barter, the method of exchange of goods which is of equal value. The Market Economy The exchange and trading of goods and services is what takes place in a market economy. This is a form of a free market hence also being known as “free market economy”. In a market economy, what to produce is determined by what the people demand. For example, in a city with no roads, cars would not need to be produced or traded due to the fact that there is no demand for them. In terms of how to produce, a market economy is the complete opposite of a planned economy where the government decides what to produce and in what quantities to produce, a market economy allows for much freedom. Everything in a market economy is produced for people in exchange of goods or services. An example would be an individual purchasing an automobile due to their need of transportation; money would need to be exchanged for the product. In a market economy, there is something known as the “invisible hand” which represents the supply and demand market forces. This defines what is produced, in what quantity and at what price. One example of a country, which embraces such an economy, would be the United States of America, which actually includes more market economy traits than Western Europe countries. Transaction in this market occur when both buyers and sellers agree on the price of a given good or service. Government intervention is minimal and confines itself more on regulation. People are free to engage in business if they so decided. However, they have to face some risks and consequences in a competitive market. Planned Economy A planned economy is a complete opposite of a market economy. A market economy is towards production being based on the supply and demand, or the “invisible hand” , a planned economy is mostly government controlled with the government deciding everything. In a planned economy, the government decides what gets produced, at what quantity and what price. The state-owned as well as the private enterprises in such economies receive guidance and directives from the government regarding economic problems including what to produce, how to produce and for whom to produce. Mixed Economy In a mixed economy, both capitalism and socialist economies are found. This economy is basically a mix of a rather free economy such as a market combined with a planned economy as well as avoiding the issues with capitalism and socialist economies. Production Possibility Frontier (PPF) Under the field of macroeconomics, the production possibility frontier (PPF) represents the point at which an economy is most efficiently producing its goods and services, and therefore allocating its resources in the best way possible. If the economy is not producing quantities indicated by the PPF, resources are being managed inefficiently, and the production of society will dwindle. The production possibility frontier shows there are limits to production, so an economy, to achieve efficiency, must decide what combination of goods and services can be produced. Unemployed Resources and Inefficiency Even casual observers of modern life know that society has unemployed resources in the form of idle workers, idle factories, unutilized minerals and raw materials, idle land, unused brain, etc. Such an economy is not on its PPF, but well inside it. Importance of PPF 1. It illustrates the definition of economics as the science of choosing what goods to produce. 2. PPF provides a rigorous definition of scarcity. It shows the outer limit of producible goods dictated by the law of scarcity. Scarcity is a reflection of the limitation on our living standards imposed by PPF. 3. PPF can illustrate the three basic problems of economic life-what, how and for whom. 4. PPF can illustrate the general point that we are always choosing among limited opportunities. Opportunity Cost It is the value of what is forgone in order to have something else. The value is unique for each individual. This is important to the PPF because a country will decide how to best allocate its resources according to its opportunity cost.