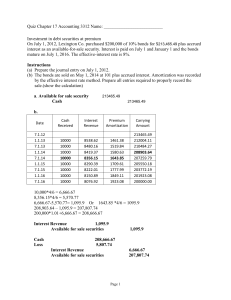

Investment in shares and bonds. Corporations invest in shares & bonds due one of the 3 reasons - Corporation may have excess cash. - To generate earnings from investment income. - For strategic reasons. Types of Investments Investments in: Shares Bonds What are shares and bonds? Shares Shares: Investment in the equity of a company which gives ownership rights to the investor. Proof of ownership is evidenced by a share certificate (stock certificate) which is transferable. The share certificate mainly shows: Name of the issuing company Name of the investor (shareholder) Par value of shares Number of shares in the name of the investor Date of issue/transfer Bonds Bonds are a form of interest bearing notes payable. The issuance of bonds payable is a technique of splitting a very large loan into many transferable units. Investment in bonds is like giving a long-term loan with option to transfer the loan to another party who desires to invest in bonds. The bond paper issued to bond holder mainly shows: Name of the issuing company Name of the investor (bond holder) Par value of the bond Number of bonds Date of issue/transfer of bonds Interest rate Maturity date (date of repayment) When bonds are purchased from the market between interest payment dates, the purchaser pays: Market price of bond + interest accrued since the last interest date Example: Purchased 10 bonds on August 1, 2010 at a price of $9,900 Par value of bond = $1,000 Interest Date: June 1st and December 1st Interest Rate = 9% per year Paid brokerage of $50 Interest from June 1st to August 1st (2 months) $10,000 x 9/100 x 2/12 = $150 Aug 1 Dec 1 Debt securities Bond Interest receivable Cash Cash 9,950 150 10,100 450 Bond Interest receivable Bond interest revenue 150 300 The investor closes its accounts on Dec 31st: Dec 31 Bond Interest Receivable Bond Interest Revenue 75 75 Example: Sale of Bonds 10 bonds of EK Corporation are carried in the accounts at $9,800. Sold at $9,400 plus interest of $90 (less brokerage of $50) Proceeds from sale (9400+90-50) $9,440 Less: proceeds representing interest revenue 90 Sale price of bonds (excluding interest received) $9,350 Cost of bonds (in the books of A/Cs) $9,800 Loss on sale $ 450 Journal entry to record sale of bonds Dr 9,440 450 Cash (9400+90-50) Loss on sale of debt securities Debt securities (original cost) Bond interest revenue Cr 9,800 90 ACCOUNTING FOR STOCK INVESTMENTS Accounting for sale of stocks Recording Sale of Stock Sold 1000 shares for $39,500 after deducting brokerage of $500 Cash Loss on sale of stock investments Stock investments Dr 39,500 1000 Cr 40,500 The loss is normally reported under ‘’Other expenses and losses’’ in the income statement. Accounting & shareholders control over company How shareholders exercise control over a (public) company listed on the stock exchange? All powers are vested in the Board of Directors of the company. Board of Directors elects the CEO/ Managing Director (by majority vote) who runs the company. The shareholders elect the Directors on Board. Voting power of each shareholder depends on the percentage of shares held by him. In Pakistan, a public company must have at least 7 directors on the board. In case 70% votes are cast, then any person holding 10% shares can elect one director on the Board. Why “significant” control with 20 to 50% shareholding? In 2018 Pakistan Tehreek-e-Insaf emerged as the winner by bagging 16.9 million votes out of total registered voters of 107.5 million. It got about 15.7% of total registered votes; and got 34.1% of the votes actually cast. Some-thing similar happens in every elections. You see the power of 34.1% votes! About 49.5 million citizens voted in the 2018 election out total voters of 107.5 million. This means that less than half (46%) of the registered citizens voted. Voting for directors is done in a some what similar manner. All share-holders do not vote. So a shareholder with 20 to 50% shares can exercise significant control over the company. EQUITY METHOD Holdings between 20% and 50% (medium control) With such holding the investee company, in some sense, becomes part of the investor company due to its control and influence. So investor companies use ‘equity method’ i.e. the investor records its share of net income of the investee in the year it is earned. Accounting when control is medium: Example MM Corporation acquires 30% of the common stock of Beck Company Limited for $120,000 (including brokerage) on Jan 1, 2010. Purchase of Stocks Dr Jan 1 Stock Investment 120,000 Cash To record purchase of Beck Common Stock Cr 120,000 For 2010, Beck reports Net Income of $100,000. It declares and pays cash dividend of $40,000. MM Corporation’s share in income is $30,000 (30% of $100,000). To record 30% share in income Dr Cr Dec 31 Stock investments 30,000 Revenue from investment in Beck Company 30,000 To record receipt of dividend Dec 31 Cash Stock investments 12,000 12,000 Stock Investments Jan 1 Dec 31 120,000 30,000 Bal. Dec 31 12,000 138,000 Revenue from investment in Beck Company Dec 31 30,000 Accounting: absolute control Holding of more than 50% shares A company that owns more than 50% of the common stock of another company is known as the parent company. The other company is called the subsidiary (affiliated) company. The parent company usually prepares consolidated financial statements, i.e. assets, liabilities, revenues and expenses of the parent company are combined with those of the subsidiary in the balance sheet, income statement etc. Categories of securities for valuation and reporting in financial statements Trading securities or Marketable securities are purchased primarily for sale in the near term to generate income on short-term price difference. Available for sale securities are purchased with the intent of selling them some time in the future. Held to maturity securities are debt securities that the investor has the intent and ability to hold to maturity. Cost Principle does not apply to Investments for sale These are valued at fair market prices On 31 December 2009 Cost Trading Securities $ 93, 600 Available for Sale Securities 48,800 Fair Value 102, 800 43,050 Unrealized Gain/(Loss)$ 9,200 (5,750) 31-12-2009 - Entry for Trading Securities (Marketable Securities) Dr. Cr. Market Adjustment – Trading 9, 200 Unrealized Gain – Income 9, 200 31-12-2009 - Entry for Available for Sale Securities Dr. Unrealized Loss- Equity 5,750 Market Adjustment – Available for SaleSecurities Cr. 5,750 Cost + Balance in the Market Adjustment A/C = (in the stock investment A/C) Market Value (in the market adjustment A/C) Example: For recording securities at market value (fair value) As on Dec 31, 2010 PH Corporation is holding the following securities: Cost $ Fair Value $ Unrealized gain/(loss) $ 93,600 94,900 1,300 Available for sale Securities 48,800 51,400 2,600 Trading Securities As on Dec 31, 2009 Market Adjustment-Trading 31/12/09 9,200 Market Adjustment-Available for sale 31/12/09 5,750 ‘Market Adjustment’ Accounts act as ‘Adjunct Accounts’ or ‘Contra Accounts’ depending on whether the account has a debit or credit balance. Many times, it may act as an ‘Adjunct Account’ (having a debit balance) to the Investment Account. Market Adjustment-Trading 31/12/09 Bal. (required) 9,200 31/12/10 7,900 1,300 Market Adjustment-Available for sale 31/12/10 Bal. (required) 8,350 31/12/09 2,600 Trading Securities-cost 93,600 Available for sale Securities 48,800 5,750 Entries required to get balances of $1,300 and $2,600 in the “Market adjustment-trading” and “Market adjustment-available for sale” accounts respectively. Trading Securities Unrealized Loss-Income 7,900 Market adjustment-trading 7,900 Available for sale Securities Market adjustment-available for sale Unrealized gain or loss-equity 8,350 8,350 The unrealized gain of $8,350 is not shown in the income statement as the shares will be sold in future by which time the gain may not remain at $8,350. In this way, net profit for 2010 is reported correctly. Presentation in the Balance Sheet A) Marketable Securities (or short-term investments) Securities that are: Readily marketable or saleable Intended to be converted into cash within one year PACE CORPORATION Balance Sheet (partial) As on 31 Dec, 2010 Current Assets Cash Short-term investments (or Marketable Securities) at fair value Accounts Receivable $55,000 147,000 900,560 B) Long term Investments Not intended to be converted into cash within one year Long term investments in available-for-sale securities are reported at fair value Investment in common stock accounted for under equity method are reported at their equity value XY Company Ltd. Income Statement (partial) For the year ended 31-12-2010 Non-operating Revenue and gains: Interest Revenue Dividend Revenue Gain on sale of Investment Unrealized Gain-Income Non-operating expenses and losses: Loss on sale of investments Unrealized Loss-Income Rs. 150,500 500,000 475,000 93,600 56,200 84,125 IFRS Self-Test Questions The following asset is not considered a financial asset under IFRS: a) trading securities. b) held-for-collection securities. c) equity securities. d) inventories. IFRS Self-Test Questions Under IFRS, the equity method of accounting for long-term investments in common stock should be used when the investor has significant influence over an investee and owns: a) between 20% and 50% of the investee’s common stock. b) 30% or more of the investee’s common stock. c) more than 50% of the investee’s common stock. d) less than 20% of the investee’s common stock. IFRS Self-Test Questions Under IFRS, unrealized gains on non-trading stock investments should: a) be reported as other revenues and gains in the income statement as part of net income. b) be reported as other gains on the income statement as part of net income. c) not be reported on the income statement or balance sheet. d) be reported as other comprehensive income. CORPORATE FORM OF ORGANIZATION Corporation (or Limited Company) is a separate legal entity and distinct from its owners. Can sue or can be sued like a person. Should follow laws and pay taxes. Publicly held or privately held corporations Publicly held corporations are owned by general public. Privately held corporations are owned by few shareholders, not by general public. Characteristics of a Corporation: Separate legal existence Limited liability of stockholders Ownership transferable Ability to acquire capital Continuous life An unrealized loss on available-for-sale securities is: a. reported under Other Expenses and Losses in the income statement. b. closed-out at the end of the accounting period. c. reported as a separate component of stockholders' equity. d. deducted from the cost of the investment. Unrealized gains and losses related to availablefor-sale securities are reported in other comprehensive income under GAAP and IFRS. These gains and losses that accumulate are then reported in the balance sheet.