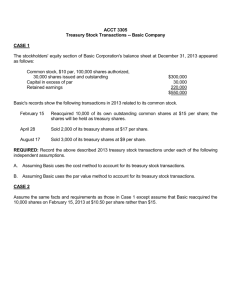

Corporations and Stocks By Midhat Kidwai 1 Difference between a Corporation and Sole Proprietorship & Partnership 1. Separate Legal Existence: As an entity separate and distinct from its owners, the corporations acts under its own name rather than in the name of its stakeholders. Engro Foods may buy, own and sell property. It may borrow money, and may enter legally binding contracts in its own name. It may also sue or be sued, and it pays its own taxes. Remember that in a partnership the acts of the owners (partners) bind the partnership. In contrast, the act of its owners (stockholders) do not bind the corporation unless such owners are agents of the corporations. For example, if you owned shares of Engro Foods stock, you would have the right to purchase raw materials for the company unless you were appointed as an agent of the company, such as a purchasing agent. 2. Limited Liability of Stockholders: Since a corporation is a separate legal entity, creditors have recourse only to corporate assets to satisfy their claims. The liability of stockholders is normally limited to their investment in the corporation. Creditors have no legal claim on the personal assets of the owners. Even in the event of bankruptcy, stockholders' losses are generally limited to their capital investment in the corporation. 2 3. Transferable ownership rights: Shares of capital stock give ownership in a corporation. These shares are transferable units. Stockholders may dispose of part or all of their interest in the corporation simply by selling their stock. Remember that the transfer of an ownership interest in a partnership requires the consent of each owner. In contrast, the transfer of stock is entirely at the discretion of the stockholder. The transfer of ownership rights between stockholders normally has no effect on the daily operating activities of the corporation. Nor does it affect the corporation’s assets, liabilities and total ownership equity. The transfer of these ownership rights is a transaction between individual owners. After it first issues the capital stock, the company does not participate in such transfers. 4. Ability to acquire capital: It is relatively easy for a corporation to obtain capital through the issuance of stock. Investors buy stock in a corporation to earn money over time as the share price grows, and because a stockholder has limited liability and shares of stock are readily transferable. Also, individuals can become stockholders by investing relatively small amounts of money. In sum, the ability of a successful corporation to obtain capital is virtually unlimited. 5. Continuous Life: The life if a corporation is stated in its charter. The life may be perpetual, or it may be limited to a specific number of years. If it is limited, the company can extend the life through renewal of the charter. Since a corporation is a separate legal entity, its continuance as a going concern is not affected by the withdrawal, death, or incapacity of a stockholder, employee, or 3 officer. As a result, a successful enterprise can have a continuous and perpetual life. Forming a Corporation (Limited Liability Company) in Pakistan 1. Obtain approval of company name from SECP. 2. Register the company with SECP (online). Documents to be submitted to SECP: a) Form 1: Declaration of compliance with the pre-requisites for formation of the company b) Copy of NIC of each subscriber to the Memorandum and Articles of Association c) Memorandum (Charter) and Articles of Association (internal rules for conducting business) signed by each member . d) Authorization by sponsors to rectify Memorandum and Articles of Association and to collect certificate of incorporation. e) Form 21: Notify registered office. Registration fee challans must also be submitted to SECP along with the above documents. 3. A few days later SECP will issue a Certificate of Incorporation. This certificate signifies that the company has been legally incorporated 4 Steps of Incorporation in Pakistan (on-line): 5 Several steps must be taken after incorporation. Some of the steps are: 1. Appointment of first directors by subscribers of the Memorandum and Articles of association and notification to registrar (SECP) within 14 days. 2. First election of directors at first Annual General Meeting (AGM). 3. Directors to appoint first Managing Director (CEO) within 15 days if incorporation. 4. Appointment of first auditor within 60 days by directors. 5. Appointment of company secretary within 15 days by the directors. 6 6. Obtain “Commencement of Business” certificate from the registrar (SECP). To be able to function, the company must register with the following Government departments: 1. Income Tax Department 2. Sales Tax Department 3. Excise and Taxation Department 4. Sindh Employees Social Security Institution (SESSI) 5. Employees Old-Age Benefits Institution (EOBI) 6. Labour Department 7 STOCK (SHARES) Authorized Stock (Authorized Capital): This is the maximum amount of shares the company is authorized to issue. This amount covers the initial and future needs of capital. Authorized capital is mentioned in the Memorandum of Association. This requires no accounting entry. Mentioned in the Balance Sheet but not added to equity items. Issuance of stocks: A company sets the selling price of its new shares (at the time of issue) considering: a) It’s anticipated future earnings b) It’s expected dividend rate c) It’s current financial position d) Current state of economy e) State of share market Underwriting: A company may sell (issue) shares directly to investors (as is always done in Pakistan). However, at times companies request some bank to underwrite the share issue. 8 Underwriting (cont’d): In Pakistan the underwriting bank guarantees to take up all the shares that may remain unsubscribed (unsold). This way the company ensures that it will be able to raise the required capital. Underwriter charges a fee/commission. In USA underwriting banks buy the entire stock issue and then resell the shares to investors and charge a fee. Market Value: Shares are traded on the stock exchange. In general, share prices are affected by factors mentioned under Issuance of Shares above. Trading of shares involves transfer of already issued shares from an existing shareholder to another investor. These transactions have no impact on the stockholders’ equity. At the time of transfer no entry is required in the books of the company that had previously issued the shares. 9 Par Value and No Par Value Stock Par Value Stock is capital stock to which charter (Memorandum of Association) has assigned a value per share. In Pakistan, shares of all companies have a par value. Most shares in Pakistan have par value of Rs. 10 each. Par value determines the legal capital per share that a company must retain in business for protecting corporate creditors. In Pakistan a company is not allowed to distribute dividends to shareholders from par value of shares. Dividends are allowed to be distributed out of retained earnings. No Par Value Stock (in US) is capital stock to which charter has not assigned a par value. Instead the board of directors , in some companies of USA assign a stated value. In Pakistan we do not have no-par value stock. 10 Accounting for Issue of Common Stock Issuing Par Value Common Stock for Cash Shares can be issued at a price equal to, less than or greater than par value. a) If a company issues 5,000,000 shares at par value of Rs. 10 each, the journal entry will be: Dr Cash Cr 50,000,000 Common Stock 50,000,000 b) If the company issues 5,000,000 shares at Rs. 15 (par value is Rs. 10 each), The journal entry will be: Dr Cash Cr 75,000,000 Common Stock 50,000,000 Paid in Capital in Excess of Par value(Share Premium) 25,000,000 11 Issuing No Par Common Stock for cash When no par common stock has a stated value, the entries are similar to those illustrated for par value stock. a) If company issues 5,000,0000 no- par-value stock for $15 with a stated value of $10 per share, the entry will be: Dr Cash Cr 75,000,000 Common Stock 50,000,000 Paid in Capital in Excess of Stated value 25,000,000 b) If no par stock has no stated value, then entry will be: Dr Cash Common Stock Cr 75,000,000 75,000,000 12 Issuing Common stock for services or non-cash assets: In such a situation what cost should be recognized in the exchange transaction? Answer: Comply with the cost principle. Cost, in such, cases, is the cash equivalent price. Cost is either the fair market value of the shares issued or the fair market value of the service or non-cash asset received, whichever is more clearly determinable (Objectivity Principle). If a lawyer has sent a bill for $10,000 for helping J.J. Company to incorporate, then J.J. Company will pass the following entry: The value of the services received is clear from the bill and at the time of incorporation shares are not listed on the stock exchange (so market of shares can not be determined). 8000 shares with par value $1 each are issued to the lawyer Dr Organization Expense Cr 10,000 Common Stock 8,000 Paid in Capital in Excess of Par 2,000 13 MM Corporation is an existing company listed on the stock exchange with par value of $5 and traded at $8 per share. Mr. P Jones desiring to sell his land, had put an advertisement asking for a price of $170,000. MM Corporation buys the land by issuing 20,000 shares to Mr. P Jones. Entry in the books of MM Corporation: Dr Land 160,000 Common Stock Paid in Capital in Excess of Par value Cr 100,000 60,000 In this case the market values of the shares is more clearly determinable so the transaction is based on $160,000, which is the value of shares. 14 Accounting for Treasury Stock Treasury stock is a corporation’s own stock that it has issued and subsequently reacquired from shareholders, but not retired (not cancelled). These can be resold by the company. In US about 60% of corporations quoted on the stock exchange have Treasury Stock on their Balance Sheets. In Pakistan up to 2009, under law, companies were not allowed to purchase their own shares. Upto 2009 companies were not allowed to resell the acquired shares. The acquired shares had to be cancelled. This meant that companies were not allowed to have treasury stock in Pakistan. In 2009 an Ordinance was issued which permitted companies to have treasury stock. The ordinance was allowed to lapse. In 2017, National Assembly passed the Companies Act 2017 which permits companies to buy their own shares 15 from shareholders and to re-sell them on the market. Reasons for acquiring Treasury Stock: 1. To reissue the shares to officers and employees under bonus and stock compensation plans. 2. To signal to the stock market that management believes the stock is underpriced, in the hope of enhancing its market value. 3. To have additional shares available for use in the acquisition of other companies. 4. To reduce the number of shares outstanding and thereby increase earnings per share. 5. To rid the company of disgruntled investors, perhaps to avoid a takeover. -Treasury stock is a contra stockholder’s equity account (like a withdrawal account). Thus, acquisition of treasury stock reduces stockholders’ equity. SECP notified Buy Back regulations on 23rd May 2019. 16 Purchase of Treasury Stock Treasury stock is accounted for by the cost method. On 1st Jan 2010, Mead Incorporated equity section showed: 100,000 shares issued at par of $5 Retained Earnings Total Stockholders’ equity =$500,000 =$200,000 =$700,000 On 1st Feb 2010, Mead acquires 4000 shares of its stock at $8 per share. The entry is: Date 1 Feb Dr Treasury Stock Cash Cr 32,000 32,000 17 18 Note the difference in the terms “Shares issued” and “Shares Outstanding” Shares Issued =100,000 shares Less: Treasury Stock =4,000 shares Shares Outstanding =96,000 shares Disposal of Treasury Stock SALE ABOVE COST: Suppose Meads purchased its own shares (4000 shares) at $8/share from the market on Feb 1,2010. Later on July 1, 2010, the company sells 1000 shares at $10/share. The entry to record sale of treasury stock is as follows: Date 1 July Dr Cash Cr 10,000 Treasury Stock 8,000 Paid in Capital from Treasury Stock 2,000 19 Treasury Stock 1 Feb. 32,000 1 July. 8,000 Paid in Capital from Treasury Stock 1 July. 2,000 20 Treasury stock is not an asset (it is a contra equity account). So, there can be no gain on sale of Treasury stock. There can be no gain or loss on stock transactions with its own stockholders (owners). Treasury stock is something similar to withdrawal by the owners. Sale of treasury stock below cost Out of the balance 3,000 shares (Treasury stock, Meads previously purchased at $8/share) sold 800 shares on 1/10 at $7. Entry at the time of sales of shares will be: Date 1/10 Dr Cash Paid in Capital from Treasury Stock Treasury Stock (800 X 8) Cr 5,600 800 6,400 21 Treasury Stock 1/2 1/10 32,000 1/7 1/10 8,000 6,4oo Bal 17,600 Paid in Capital from Treasury Stock 1/10 800 1 July. 1/10 2,000 Bal 1,200 22 In situations of sale of treasury stock below cost, if the balance in the “Paid in Capital from Treasury Stock” account is fully exhausted, we should debit Retained earnings. For example, if Meads sells the remaining 2,200 shares at $7/share on 1st Dec, the entry will be: Date 1 Dec Dr Cash 15,400 Paid in capital from Treasury Stock 1,200 Retained Earnings 1,000 Treasury Stock Cr 17,600 “Paid in capital from Treasury Stock” account only has a balance of $1200, whereas the cash received is $2200 short as compared to Treasury Stock ($17,600) sold. So, we should debit Retained earnings by $1,000 23 Treasury Stock 1/2 1/10 32,000 Bal 1/7 8,000 1/10 6,4oo 17,600 Paid in Capital from Treasury Stock 1/10 1/12 800 1 July. 2,000 1/10 Bal 1,200 1/12 Bal 0 1,200 Retained Earning 1/12 1,000 Bal 200,000 24 Restriction of Retained Earnings for Treasury Stock Owned: Purchase of treasury stock, like cash dividends, are distribution of assets to the stockholders in the corporation. Many states in the US have a legal requirement that distribution to stockholders (including purchases of treasury stock) cannot exceed the balance in the Retained Earnings Account. Therefore, retained earnings usually are restricted by an amount equal to the cost of any shares held in the treasury. 25 Preferred Stock: Another class of stock. Typically preferred stockholders get priority (preference) over common stockholders as to: 1) Distribution of earnings (dividend) 2) Assets in the event of liquidation However, generally they do not have voting rights. The dividend rate on preferred stock is fixed at the time of issuance. Sometimes, dividend amount per share is fixed. If Stine Corporation issues 100,000 shares of $10 par value preferred stock for $12 cash per share, then to record the issuance, the entry is: Dr Cash Preferred Stock Paid in Capital in Excess of Par valuePreferred Stock Cr 1,200,000 1,000,000 200,000 26 Cumulative Preferred Stock and Cumulative Dividend: Preferred stock may contain a cumulative dividend feature. This means that preferred stockholders must be paid both current year’s dividends and any unpaid prior-year dividends before common stockholders receive dividends. When dividend is not declared on cumulative Preferred stock, such undeclared dividends are called “dividend in arrears”. Dividend in arrears is not a liability. No payment obligation exists until the board of directors declare a dividend. However, separate disclosure of “dividend in arrears” should be made as a note to the financial statements. 27 28 29 30 THAT’S IT 31