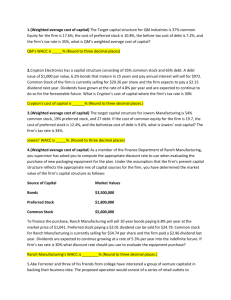

COST OF CAPITAL AND CAPITAL STRUCTURE A. Given the following information, calculate the weighted average cost of capital for the Holy Corporation: Percent of Capital Structure: Preference shares 10% Ordinary equity 60% Debt 30% Additional information: Corporate Tax rate Dividend, preference Dividend, expected, ordinary Price, preference Growth rate Bond yield Flotation cost, preference Price, Ordinary 34% P9.00 P3.50 P102.00 6% 10% P3.20 P70.00 B. Compute the cost for the following sources of long term financing: a. A P1,000 par value bond with a market price of P970 and a coupon interest rate of 10 percent. Flotation costs for a new issue would be approximately 5 percent. The bonds mature in ten years and the corporate tax rate is 34 percent. b. A preference share selling for P100 with annual dividend payment of P8. If the company sells a new issue, the flotation cost will be P9 percent. The company’s marginal tax rate is 30 percent. c. Internal ordinary equity where the current market price of the ordinary share is P38. The expected dividend this coming year should be P3, increasing thereafter at a 4 percent annual growth rate. The corporate tax rate is 34 percent. d. New ordinary share where the most recent dividend was P2.80. The company’s dividend per share should continue to increase at an 8 percent growth rate into the indefinite future. The market price of the ordinary share is currently P53; however, flotation costs of P6 per share are expected if the new stock is issued. C. Happy Gilmore Co. is trying to calculate its cost of capital for use in capital budgeting decisions. Mr. Shooter, the vice president for finance, has given you the following information and has asked you to compute the weighted average cost of capital. The company currently has outstanding bond with an 11.2 percent coupon rate and another bond with a 7.5 percent rate. The firm has been informed by its investment banker that the bonds of equal risk and credit ratings are now selling to yield 12.4 percent. The ordinary share has a price of P54 and an expected dividend of P2.70 per share. The firm’s historical growth rate of earnings and dividends per share has been 14.5 percent, but security analysts expect this growth rate to slow to 12 percent in future years. The preference share is selling at P50 per share and carries a dividend of P4.75 per share. The corporate tax rate is 35 percent. The flotation cost is 2.8 percent of the selling price for preference share. The optimum capital structure for the firm seems to be 35 percent debt, 10 percent preference shares, and 55 percent ordinary equity in the form of retained earnings. Required: Compute the cost of capital for the individual components in the capital structure and then calculate the weighted average cost of capital. D. Analyst has collected the following information regarding Christopher Company: The company’s cost of capital structure is 70 percent equity, and 30 percent debt. The yield to maturity on the company’s bonds is 9 percent. The company’s year-end dividend is forecasted to be $0.80 The company expects that its dividend will grow at a constant rate of 9 percent a year. The company’s stock price is $25. The company’s tax rate is 40 percent. The company anticipates that it will need to raise new common stock this year. Its investment bankers anticipate that the total flotation cost will equal 10 percent of the amount issued. Assume the company accounts for flotation costs by adjusting the cost of capital. Required: Calculate the Company’s Weighted Average Cost of Capital E. Jefferson Corp. requires a $15 million to fund its current year capital projects. Jefferson will finance part of its needs with $9 million in internally generated funds. The firm’s common stock market price is $120 per share. The firm’s last dividend was $5 per share and is expected to grow at a rate of 11 percent annually for the foreseeable future. Another portion of the required funds will come from the issue of 9,375 shares of 12 percent $100 par preferred stock that will be privately placed. The firm will net $96 per share form the sale these shares. The remainder of the funding needs will be met with debt. Five thousand 10year $1,000 bonds with a coupon rate of 15 percent will be issued to net the firm $1,020 each. Interest will be paid annually on the bonds. Required: The firm’s tax rate is 30 percent. What is Jefferson’s weighted average cost of capital? F. Zenon Co. recently issued 10-year 12 3/4 percent coupon bonds at face value. Zenon's beta is .62, its target debt/equity ratio is .60, and the tax rate is 34 percent. If the market risk premium is 8 percent and the risk-free rate is 10 percent, estimate Zenon's weighted average required return? G. The Argon Company has the following capital structure: 8% long-term debt due 1999 $ 2,000,000 8% cumulative preferred stock $ 2,000,000 Common stock $6,000,000 Other information is as follows: Beta of Argon stock 1.5 Tax rate 34% Market rate of return 12% Risk-free rate 6% Market cost of debt 10% What is the weighted average required return for Argon? H. Assume the risk-free rate is 8 percent, beta is 1.5, and the return on the market is 12 percent. The firm has a D/A ratio of .4. The cost of debt is 10 percent and the tax rate is 34 percent. What is the weighted average required return? I. Druid Corp. has the following capital structure: Debt Equity Total $ 18,000,000 $ 27,000,000 $ 45,000,000 Given KM of 15%, KRF of 8%, beta of 0.875, a before-tax cost of debt of 11%, and a tax rate of 34%, calculate Druid's weighted average required return assuming that the firm intends to use only retained earnings and debt? J. Neon Corp. has the following capital structure: Debt $ 2O,000,000 Equity $ 25,000,000 Tota l $ 45,000,000 Neon Corp.'s profit margin, payout ratio, and sales are expected to be 10%, 40%, and $50 million respectively. If Neon does not wish to issue any new common stock, what is the maximum amount of new capital that can be raised for investment projects? K. CWF, Inc. had total earnings of $120,000 during the past year. The company pays out 60 percent of its earnings as dividends. CWF has determined that its optimal capital structure is 40 percent debt and 60 percent equity. Given this information, how much new capital (retained earnings plus new debt) can be raised before CWF is forced to issue new common stock, assuming it stays at its target capital structure? L. Zapata Enterprises is financed by two sources of funds: bonds and common stock. The cost of capital for funds provided by bonds is ki, and ke is the cost of capital for equity funds. The capital structure consists of B dollars’ worth of bonds and S dollars’ worth of stock, where the amounts represent market values. Compute the overall weighted average of cost of capital, ko. M. Assume that B (in Problem L) is $3 million and S is $7 million. The bonds have a 14 percent yield to maturity, and the stock is expected to pay $500,000 in dividends this year. The growth rate of dividends has been 11 percent and is expected to continue at the same rate. Find the cost of capital if the corporation tax rate on income is 40 percent. N. On January 1, 20X1, International Copy Machines (ICOM), one of the favorites of the stock market, was priced at $300 per share. This price was based on an expected dividend at the end of the year of $3 per share and an expected annual growth rate in dividends of 20 percent into the future. By January 20X2, economic indicators have turned down, and investors have revised their estimate for future dividend growth of ICOM downward to 15 percent. What should be the price of the firm’s common stock in January 20X2? Assume the following: a. A constant dividend growth valuation model is a reasonable representation of the way the market values ICOM. b. The firm does not change the risk complexion of its assets nor its financial leverage. c. The expected dividend at the end of 20X2 is $3.45 per share. O. Far Stores has launched an expansion program that should result in the saturation of the Bay Area marketing region of California in six years. As a result, the company is predicting a growth in earnings of 12 percent for three years and 6 percent for the fourth through sixth years, after which it expects constant earnings forever. The company expects to increase its annual dividend per share, most recently $2, in keeping with this growth pattern. Currently, the market price of the stock is $25 per share. Estimate the company’s cost of equity capital. Q.The Manx Company was recently formed to manufacture a new product. It has the following capital structure in market value terms: Debentures Preferred stock Common stock (320,000 shares) $ 6,000,000 2,000,000 8,000,000 $16,000,000 The company has a marginal tax rate of 40 percent. A study of publicly held companies in this line of business suggests that the required return on equity is about 17 percent. (The CAPM approach was used to determine the required rate of return.) The Manx Company’s debt is currently yielding 13 percent, and its preferred stock is yielding 12 percent. Compute the firm’s present weighted average cost of capital. R.The R-Bar-M Ranch in Montana would like a new mechanized barn, which will require a $600,000 initial cash outlay. The barn is expected to provide after-tax annual cash savings of $90,000 indefinitely (for practical purposes of computation, forever). The ranch, which is incorporated and has a public market for its stock, has a weighted average cost of capital of 14.5 percent. For this project, Mark O. Witz, the president, intends to provide $200,000 from a new debt issue and another $200,000 from a new issue of common stock. The balance of the financing would be provided internally by retaining earnings. The present value of the after-tax flotation costs on the debt issue amount to 2 percent of the total debt raised, whereas flotation costs on the new common stock issue come to 15 percent of the issue. What is the net present value of the project after allowance for flotation costs? Should the ranch invest in the new barn? S. Cohn and Sitwell, Inc., is considering manufacturing special drill bits and other equipment for oil rigs. The proposed project is currently regarded as complementary to its other lines of business, and the company has certain expertise by virtue of its having a large mechanical engineering staff. Because of the large outlays required to get into the business, management is concerned that Cohn and Sitwell earn a proper return. Since the new venture is believed to be sufficiently different from the company’s existing operations, management feels that a required rate of return other than the company’s present one should be employed. The financial manager’s staff has identified several companies (with capital structures similar to that of Cohn and Sitwell) engaged solely in the manufacture and sale of oildrilling equipment whose common stocks are publicly traded. Over the last five years, the median average beta for these companies has been 1.28. The staff believes that 18 percent is a reasonable estimate of the average return on stocks “in general” for the foreseeable future and that the risk-free rate will be around 12 percent. In financing projects, Cohn and Sitwell uses 40 percent debt and 60 percent equity. The after-tax cost of debt is 8 percent. a. On the basis of this information, determine a required rate of return for the project, using the CAPM approach. b. Is the figure obtained likely to be a realistic estimate of the required rate of return on the project? T. BoardWalk, Inc. currently has the following structure: Bonds - $5 million face value, 10% coupon, annual interest payment Common stock - 2,000,000 shares outstanding The following is considering a $10 million expansion program which can be financed in the following ways: Plan A – Issue a $10 million in new bonds. The bonds would be sold at par value and would have a 12% annual coupon. Plan B – Issue $10 million in new common shares at $40 per share. The company’s marginal tax rate is 40%. Next year, the expected EBIT is $4 million if the expansion program is expected. U. David Ding Baseball Bat Company currently has $3 million in debt outstanding, bearing an interest rate of 12 percent. It wishes to finance a $4 million expansion program and is considering three alternatives: additional debt at 14 percent interest (option 1), preferred stock with a 12 percent dividend (option 2), and the sale of common stock at $16 per share (option 3). The company currently has 800,000 shares of common stock outstanding and is in a 40 percent tax bracket. a. If earnings before interest and taxes are currently $1.5 million, what would be earnings per share for the three alternatives, assuming no immediate increase in operating profit? b. Develop a break-even, or indifference, chart for these alternatives. What are the approximate indifference points? To check one of these points, mathematically determine the indifference point between the debt plan and the common stock plan. What are the horizontal axis intercepts? c. Compute the degree of financial leverage (DFL) for each alternative at the expected EBIT level of $1.5 million. d. Which alternative do you prefer? How much would EBIT need to increase before the next alternative would be “better” (in terms of EPS)? V.Cybernauts, Ltd., is a new firm that wishes to determine an appropriate capital structure. It can issue 16 percent debt or 15 percent preferred stock. The total capitalization of the company will be $5 million, and common stock can be sold at $20 per share. The company is expected to have a 50 percent tax rate (federal plus state). Four possible capital structures being considered are as follows: PLAN 1 2 3 4 DEB 0% 30 50 50 T PREFERRED 0% 0 0 20 EQUITY 100% 70 50 30 a. Construct an EBIT-EPS chart for the four plans. (EBIT is expected to be $1 million.) Be sure to identify the relevant indifference points and determine the horizontal-axis intercepts. b. Using Eq. (16.12), verify the indifference point on your graph between plans 1 and 3 and between plans 3 and 4. c. Compute the degree of financial leverage (DFL) for each alternative at an expected EBIT level of $1 million. d. Which plan is best? Why? W..Hi-Grade Regulator Company currently has 100,000 shares of common stock outstanding with a market price of $60 per share. It also has $2 million in 6 percent bonds. The company is considering a $3 million expansion program that it can finance with all common stock at $60 a share (option 1), straight bonds at 8 percent interest (option 2), preferred stock at 7 percent (option 3), and half common stock at $60 per share and half 8 percent bonds (option 4). a. For an expected EBIT level of $1 million after the expansion program, calculate the earnings per share for each of the alternative methods of financing. Assume a tax rate of 50 percent. b. Construct an EBIT-EPS chart. Calculate the indifference points between alternatives. What is your interpretation of them? X. Hi-Grade Regulator Company (see Problem W) expects the EBIT level after the expansion program to be $1 million, with a two-thirds probability that it will be between $600,000 and $1,400,000. a. Which financing alternative do you prefer? Why? b. Suppose that the expected EBIT level were $1.5 million and that there is a twothirds probability that it would be between $1.3 million and $1.7 million. Which financing alternative would you prefer? Why? Y. Fazio Pump Corporation currently has 1.1 million shares of common stock outstanding and $8 million in debt bearing an interest rate of 10 percent on average. It is considering a $5 million expansion program financed with common stock at $20 per share being realized (option 1), or debt at an interest rate of 11 percent (option 2), or preferred stock with a 10 percent dividend rate (option 3). Earnings before interest and taxes (EBIT) after the new funds are raised are expected to be $6 million, and the company’s tax rate is 35 percent. a. Determine likely earnings per share after financing for each of the three alternatives. b. What would happen if EBIT were $3 million? $4 million? $8 million? c. What would happen under the original conditions if the tax rate were 46 percent? If the interest rate on new debt were 8 percent and the preferred stock dividend rate were 7 percent? If the common could be sold for $40 per share? Z.. Boehm-Gau Real Estate Speculators, Inc., and the Northern California Electric Utility Company have the following EBIT and debt-servicing burden: Expected EBIT Annual interest Annual principal payments on debt BOEHM-GAU $5,000,000 1,600,000 2,000,000 NORTHERN CALIFORNIA $100,000,000 45,000,000 35,000,000 The tax rate for Boehm-Gau is 40 percent, and for Northern California Electric Utility is 36 percent. Compute the interest coverage and the debt-service coverage ratios for the two companies. With which company would you feel more comfortable if you were a lender? Why?