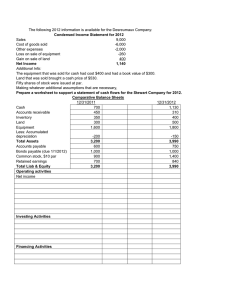

Case #19 - Real Fresh Foods, Inc. Real Fresh Foods is a mail-order company operating out of a winery near Santa Rosa, California. The company specializes in sending California specialties to catalog customers nationwide. Sales are seasonal, with most occurring in November and December—when people select Real Fresh’s Famous Fruit Fantasy boxes as Christmas gifts. Although seasonal, the company’s sales are fairly predictable, because the bulk of Real Fresh customers are regulars who come back year after year. The company has also managed to smooth out its sales somewhat by offering incentives, such as the Fruit of the Month club, that encourage customers to buy throughout the year. The nature of the mail-order business is such that most of Real Fresh’s sales are on credit; therefore, the company has historically had a high accounts receivable balance relative to sales. It has also historically been short of cash, forcing it to delay payments to suppliers as long as possible (its average time to pay accounts in 2010, was 67 days). In January 2011, Tom Appleby and Alice Plummer, the president and treasurer of Real Fresh, respectively, were discussing the cash flow problem over lunch. “You know, Tom,” Alice said as she sliced a piece of avocado, “I was reading the other day about a company called Kringle’s Candles & Ornaments, and it occurred to me that we’re a lot like them. Most of our assets are current ones like their accounts receivable and inventory; and over half of ours are financed just like theirs, by current liabilities—that is, accounts payable.” She paused for a sip of chardonnay, and continued, “They got around their cash flow problems by issuing long-term debt, which took the pressure off their current obligations. I’ve been looking at that for our company, too; but then I got to thinking, there’s another way that’s a good deal easier and would produce results just as quickly.” “Oh? What’s that?” Tom replied, his interest captured. “All we have to do,” she said, “is to reduce our accounts receivable balance. That will help reduce our accounts payable balance—since, as our customers begin paying us earlier, we can pay our suppliers earlier in turn. If we could get enough customers to pay us right away, we could even pay some of the suppliers. In time to take advantage of the 2 percent discount they offer for payments within 10 days.” (Real Fresh’s suppliers operated on a 2/10, net 60 basis.) “That would increase our net income and free up even more cash to take advantage of even more discounts!” She looked excited at the prospect. “Sounds great, but how do we get people to pay us earlier?” Tom inquired, doubtfully. “Easy,” Alice continued. “Up to now we’ve been giving them incentives to pay later. Remember our ‘Buy Now, No Payments for Two Months’ program? Well, a lot of our customers use it, and it’s caused our accounts receivable balance to runway up. So, what we have to do now is give them incentives to pay earlier. What I propose is to cancel the buy now/pay later plan and offer a 10 percent discount to Page 1 of 4 everyone who pays with their order, instead. “But won’t that cause our revenues to drop?” Tom asked, again still doubtful. “Yes, but the drop will be offset by even more new customers who will come in to take advantage of the discount. I figure the net effect on sales will be just about zero, but our accounts receivable balance could be cut in half! Now here’s a kicker that I just thought of: After we’ve reduced our accounts receivable balance as far as practical, I’d like to look into the possibility of reducing our accounts payable still further by replacing them with a bank loan. The effective rate of interest that we pay by not taking our suppliers’ discounts is, after all, pretty high. So what I’d like to do is take out a loan once a year of a sufficient size that would enable us to take all the discounts our suppliers offer. The interest that we’ll pay on the loan is bound to be less than what we pay in discounts lost—so we’ll see another gain in earnings on our income statement. In fact, these two initiatives together might have a really significant impact!” “You’ve convinced me,” Tom said, “Let’s go back to the office and run some figures to see what happens!” Financial statements for Real Fresh Foods, Inc., are presented in Figure 1 (income statement) and Figure 2 (balance sheet). To Do 1. Using the data in Figures 1 and 2, compute the company’s average collection period (ACP) in days. Use a 360-day year when calculating sales per day. 2. Compute the cost, as a percent, that the company is paying for not taking the supplier’s discounts. (The supplier’s terms are 2/10, net 60; but note from the bottom of Figure 2 that Real Fresh has been taking 67 days to pay its suppliers, making that the effective final due date for accounts payable.) 3. Assume that Alice Plummer’s first initiative to offer a 10 percent discount was implemented, and the company’s average collection period dropped to 32 days. If net sales per day remained the same, as Alice expects, what would be the new accounts receivable balance? How much cash was freed up by the reduction in accounts receivable? What is the new accounts payable balance if the money is used to pay off suppliers? 4. Alice’s second initiative calls for Real Fresh to obtain a bank loan of a sufficient size to enable the company to take all suppliers’ discounts. What is the minimum size of this loan? (Hint: To take all suppliers’ discounts, the average payment period must be 10 days, and net purchases will be purchases – (Purchases from Figure 1 x .02). Assume that all this happens, and solve the following formula for the new accounts payable balance, using: Accounts payable = Average payment period x Purchase per day (based on net purchases/360) Page 2 of 4 5. Now compare the accounts payable you just solved with the new accounts payable balance you found in question 3. The difference is the size of the loan that is required. 6. Assume that Fresh &Fruity does obtain an 8 percent loan for one year in the amount you solved in question 5, and it reduces its accounts payable balance accordingly. Now the company is taking 2 percent discounts on all purchases and paying 8 percent a year on the loan balance. What is the net gain from taking the discounts and paying the interest on a before-tax basis? On an aftertax basis? 7. Assume that Fresh &Fruity does obtain an 8 percent loan for one year in the amount you solved in question 5, and it reduces its accounts payable balance accordingly. Now the company is taking 2 percent discounts on all purchases and paying 8 percent a year on the loan balance. What is the net gain from taking the discounts and paying the interest on a before-tax basis? On an aftertax basis? 8. Suppose the 8 percent loan that Real Fresh obtained was a discount loan, and the bank further required a 20 percent compensating balance of the full loan amount. What is the effective rate of interest to Real Fresh? How does this compare to your answer in question 2 for the cost of not taking a cash discount? Figure 1 Current Situation REAL FRESH FOODS, INC Income Statement, 2013 Revenue from sales Gross sales (credit) .................................................................... $1,179,000 Cost of goods sold: Beginning inventory................................................................... $ 141,000 Purchases............................................................................... $969,000 Less: Cash 0 discounts ....................................................................................... Net purchases ........................................................................ 969,000 Goods available for sale ............................................................ 1,110,000 Less: Ending inventory ............................................................... 79,557 Cost of goods sold .....................................................................1,030,443 Gross profit .................................................................................... 148,557 Selling and administrative expenses ............................................. 73,000 Earnings before interest and tax ................................................... 75,557 Interest expense ............................................................................ 0 Earnings before tax........................................................................ 75,557 Income taxes @ 33% ..................................................................... 24,934 Net income .................................................................................... $ 50,623 Page 3 of 4 Figure 2 Current Situation REAL FRESH FOODS, INC Balance Sheet As of December 31, 2013 Assets: Cash ........................................................................................... $ 3,560 Accounts receivable................................................................... 209,686 Inventory ................................................................................... 79,557 Total current assets ...............................................................$292,803 Property, plant and equipment, 11,430 net.................................................................................................. Total assets $304,233 Liabilities and equity: Accounts payable ...................................................................... $180,633 Notes payable (bank loans) ....................................................... 0 Total current liabilities...........................................................$180,633 Long-term debt .......................................................................... 0 Total liabilities ....................................................................... 180,633 Common stock ........................................................................... 13,600 Additional paid-in capital .......................................................... 83,000 Retained earnings ...................................................................... 27,000 Total equity............................................................................ 123,600 Total liabilities and equity .............................................................$304,233 Selected ratios Profit Margin ............................................................................. 4.29% Return on equity........................................................................ 40.96% Inventory turnover .................................................................... 14.82 Receivables turnover ................................................................. 5.62 Average payment period ........................................................... 67 Page 4 of 4