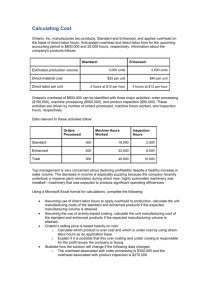

ACTIVITY-BASED COSTING *Normal costing uses only one cost driver as the application basis for all overhead costs (e.g. FOH cost per labor hour, ignores other possible cost drivers such as machine hours and material cost). To avoid that disadvantage, businesses who accept job orders may use activity-based costing (ABC). *Activity-based costing allows entities to charge job orders their respective overhead costs by applying overhead rates based on multiple cost drivers. SAMPLE PROBLEM: ABC Corporation has the budgeted overhead Cost Description Cost Amount Order Acceptance P 480,000 Equipment Set-up 1,000,000 Material Requisition 2,000,000 Pre-delivery Inspection 600,000 Depreciation and other OH 3,000,000 costs and capacities for the year: Capacity 96,000 orders 125,000 set-ups 200,000 requests 120,000 inspections 900,000 machine hours If an order would require two set-ups of equipment, four material requisitions, two pre-delivery inspection, and twelve machine hours, how much overhead cost should ABC record for the order? SOLUTION: Cost Description Order Acceptance Equipment Set-up Material Requisition Pre-delivery Inspection Depreciation and other OH Cost Amount P 480,000 1,000,000 2,000,000 600,000 3,000,000 Cost Description Order Acceptance Equipment Set-up Material Requisition Pre-delivery Inspection Depreciation and other OH Total overhead cost Capacity Cost/Driver 96,000 orders 125,000 set ups 200,000 requests 120,000 inspections 900,000 machine hours P5/order P8/ set-up P10/request P5/inspec. P3.33/MH Cost/Driver A P5/order P8/ set-up P10/request P5/inspec. P3.33/MH Capacity Required B 1 order 2 set ups 4 requests 2 inspections 12 machine hours OH Cost (AxB) P 5 16 40 10 40 P111