Strategic cost final study guid

advertisement

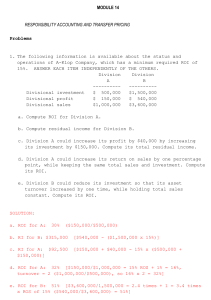

Capacity/product costs o Practical Capacity Level of capacity that reduces theoretical capacity by considering unavoidable operating interruptions (maintenance, holidays, etc.) o Theoretical Capacity Level of capacity based on producing at full efficiency all the time o Cost of Unused Capacity In the short run, capacity costs are fixed Actual capacity used/needed rarely matches available capacity Accounting in the presence of excess capacity can lead to incorrect profitability signals Happens when you assign excess capacity costs to current products Generally, occurs when demand is changing (growing or declining companies) UCC = FC x (1 – Actual used/practical capacity) o Two rules to remember about capacity Charge the cost of unused capacity to those who demand it Do not charge the cost of excess capacity to customers Customer lifetime value o To better understand how valuable a customer is, firms focus on these customer related strategies Cost to acquire a customer Profit the customer generates for the firm Retention rate (how long the customer is likely to continue the relationship with the firm) o Issues? Can be difficult to calculate Depends on a number of different factors that may differ based upon product, how customer was acquired, etc. The input to the calculation assumes that these values do not change over time Performance measures o Goals To motivate managers to exert a high level of effort to achieve the goals set by top management (bonuses) To provide the incentive for managers, acting autonomously, to make decisions consistent with the goals set by top management To develop fairly the rewards earned by managers for their effort and skill and the effectiveness of their decision-making o ROI= accounting income/ investment Popular for two reasons: Blends all the ingredients of profitability (revenues, costs, and investment) into a single percentage May be compared to other ROIs both inside and outside the firm Underlying Factors (Income/sales revenue) * (Sales revenue/invested capital) Or return on sales * investment turnover Sales margin* capital turnover Improving ROI Increase sales margin o Increase sales price or cut expenses Increase capital turnover o Increase sales price or decrease total investment Advantages and limitations Advantages o Easily understood by managers o Comparable to interest rates and the rates of return on alternative investments o Widely used and reported in the business press Limitations o Goal congruency issues: incentive for high ROI units to invest in projects with ROI higher than the minimum rate of return but lower than the unit’s current ROI o Residual Income= income- (RRR*Investment) RRR= Required rate of return (discount rate, cost of capital) RRR * investment= imputed cost of the investment Imputed costs are costs recognized in some situations, but not in the financial accounting records o EVA =(After-tax operating income – [WACC*(Assets-current liabilities)] Specific type of residual income calculation that has recently gained popularity A business unit’s income after taxes and after deducting the cost of capital (also called economic profit) Generally include unrecorded intangibles in assets such as R&D or Advertising and gross up income for these items WACC= after-tax average cost of all long-term funds in use = [(After-tax cost of debt capital *market value of debt)+(cost of equity capital*market value of equity)]/(Market value of debt+ market value of equity) o Advantages & Limitations of Residual Income Advantages Supports incentives to accept all projects with ROI > minimum rate of return Can use the minimum rate of return to adjust for differences in risk Can use a different minimum rate of return for different types of assets Limitations Favors large units Not as intuitive as ROI May be difficult to obtain a minimum rate of return at the subunit level Balanced scorecard o Financial Financial goals Evaluates the profitability of the strategy Uses the most objective measures in the scorecard The other three perspectives eventually feed back into this dimension o Customer What customers do we want to serve and how do we win and retain them? Identifies targeted customer and market segments and measures the company’s success in these segments o Internal How can we excel at our internal business processes? What processes are critical to providing value to our customers? Focuses in internal operations that create value for customers that, in turn, furthers the financial perspective by increasing shareholder value o Learning & Growth How can we continue to learn and create? Identifies the capabilities the organization must excel at to achieve superior internal processes that create value for customers and shareholders o Sustainability The fifth perspective for many organizations The balancing of short-term and long-term goals in all three dimensions of the company’s performance-economic, social, and environmental Environmental reports use environmental performance indicators (EPIS) to measure sustainability. These indicators are in three areas: Operational (measure stresses to the environment/regulatory compliance issues) Management (try to reduce environmental effects) Environmental condition (measure environmental quality) o Common Balanced Scorecard Measures Financial Perspective Income measures: operating income, gross margin percentage Revenue and cost measures: revenue growth, revenues from new products, cost reductions in key areas Income and investment measures: Economic value added, return on investment Customer perspective Market share, customer satisfaction, customer-retention percentage, time taken to fulfill customers’ requests, number of customer complaints Internal-Business-Process Perspective Innovation Process: Operating capabilities, number of new products or services, new- product development times, and number of new patents Operations Process: Yield, defect rates, time taken to deliver product to customers, percentage of on-time deliveries, average time taken to respond to orders, setup time, manufacturing downtime Postsales Service Process: Time taken to replace or repair defective products, hours of customer training for using the product Learning- and- Growth Perspective Employee measures: Employee education and skill levels, employee-satisfaction ratings, employee turnover rates, percentage of employee suggestions implemented, percentage of compensation based on individual and team incentives Technology measures: information system availability, percentage of processes with advanced controls o Features of a Good Balanced Scorecard Must motivate managers to take actions that eventually result in improvements in financial performance Tells the story of a firm’s strategy, articulating a sequence of cause- andeffect relationships Must have commitment and leadership from top management and communicate the strategy to all members of the organization Translate the strategy into a coherent and linked set of understandable and measurable operational targets, identifying only the most critical ones o Implementation Pitfalls Managers should not assume the cause- and-effect linkages are precisethey are merely hypotheses Managers should not seek improvements across all of the measures all of the time Managers should not use only objective measures: subjective measures are important as well Managers should not use too many measures