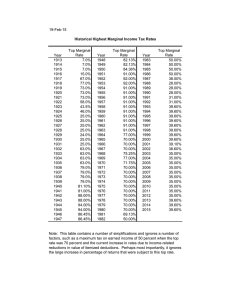

social security rules and marginal tax rates

advertisement