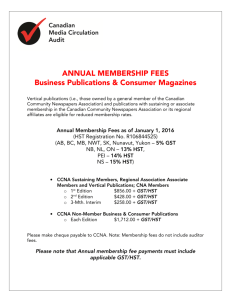

Doing Business in Canada – GST/HST Information for Non

advertisement