Hubbell Investor Day Presentation

advertisement

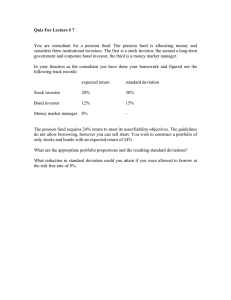

Investor Day February 27, 2013 Forward Looking Statements Certain statements contained in this presentation may constitute forwardlooking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words or phrases such as “expects”, “projected”, “scheduled”, “could”, “believe”, “anticipated” and others. Such forward-looking statements involve numerous assumptions, known and unknown risks, uncertainties and other factors which may cause actual and future performance or achievements of the Company to be materially different from any future results, performance, or achievements expressed or implied by such forward-looking statements. Such factors include: achieving sales levels to fulfill revenue expectations; unexpected costs or charges, certain of which may be outside the control of the Company; general economic and business conditions; and competition For additional information identifying factors that may cause actual results to vary materially from those stated in the forward-looking statements, refer to our most recent 10-K for the year ended December 31, 2012 that is filed with the SEC and is also available at www.hubbell.com. -2- 2013 INVESTOR DAY Today’s Agenda Introduction and Strategy Executive Officer Dave Nord – Chief Business Unit Updates • Power Systems Bill Tolley – Platform President • Lighting Scott Muse – Platform President • Electrical Systems Gary Amato – Platform President Financial Update Bill Sperry – Chief Financial Officer Concluding Remarks Dave Nord – Chief Executive Officer -3- 2013 INVESTOR DAY Introduction and Strategy Dave Nord Performance Sales OP Margin ($ Billions) (% of Sales) 16% $3.5 $3.0 $3.0 14% $2.9 $2.7 $2.5 $2.5 $2.5 $2.4 12% $2.4 $2.1 $2.0 10% $1.5 8% '05 '06 '07 '08 '09 '10 '11 '12 -5- Structurally improved to a larger and more profitable organization 2013 INVESTOR DAY Market Positioning U.S. Electrical Components Market 2012 E $75 Billion Large, Global Competitors • Capital intensive Apparatus $16 Billion Hubbell’s Focus • Branded Products Electrical Components and Connectors • Broad Number of SKUs • Serving Distributors $37 Billion Wire, Conduit, Lamps and Ballasts $22 Billion Commodity Type Products • Difficult to generate margin -6- We are positioned in the most attractive segment of the market 2013 INVESTOR DAY Hubbell Today ($ Billions) Electrical Segment Segment Platform Electrical Systems Products Lighting Business Wiring and Grounding Power Systems Electrical Products Addressable Market $ 8 $ 4 $ 8 $ 4 2012 Sales $ 0.7 $ 0.7 $ 0.7 $ 0.9 Key Brands -7- Hubbell is well positioned in large and diverse end markets 2013 INVESTOR DAY Hubbell Strategic Objectives Reliable Electrical Solutions Our Strategic Objectives Are The Critical Few Serving Our Customers Operating with Discipline Growing the Enterprise Developing Our People -8- 2013 INVESTOR DAY Serving Our Customers We will work to exceed our customer expectations with differentiated products and services Our success will be determined by how well we: Build innovative, high quality products Provide exceptional service at every touch point Deliver market leading e-commerce capabilities Broadly define our customers -9- 2013 INVESTOR DAY Operating With Discipline We will focus on results using our lean methodology to establish industry leading processes Our success will be determined by how well we: Execute flexible and efficient processes Make timely decisions Ensure a safe and compliant organization Share our best practices -10- 2013 INVESTOR DAY Growing The Enterprise We will grow our organization through new product innovation and acquisition Our success will be determined by how well we: Develop innovative new products and increase market penetration Acquire complementary businesses worldwide Consistently and successfully integrate Invest in capabilities to support growth -11- 2013 INVESTOR DAY Developing Our People We will develop talent that anticipates the increasing size and complexity of our enterprise Our success will be determined by how well we: Develop and attract high quality talent in all areas Enhance the capability of all of our people Increase diversity of talent Build on our reputation as an ethical, career-oriented company -12- 2013 INVESTOR DAY Hubbell Power Systems Bill Tolley Gerben Bakker Ken Carlson Mark Mikes Business Overview ($Billions) Segment Electrical Segment Addressable Market Size 2012 Sales POWER SYSTEMS $ 4 $ 0.9 Business Units -14- 2013 INVESTOR DAY Power Systems Value Proposition Broadest product offering -- quality brands Value-added service and total cost of ownership Relationships with distribution partners and end users Financially sound provider Best people in the industry -15- Managed SKU complexity + lower TCO = peace of mind 2013 INVESTOR DAY What’s Changing? Industry consolidation Increased international competition Increased macro uncertainty Smart Grid development Grid rebuild and investment -16- Pace of change is increasing 2013 INVESTOR DAY Markets North America 2013 Growth Outlook Rest of World Mid single digits Telecom/Other Low single digits Transmission / Substation Mid single digits Distribution Low single digits -17- 4 – 6% overall sales growth expected in 2013 2013 INVESTOR DAY 2013 Strategic Objectives Serving our Customers • Quality improvement • Service (On-time and MTO lead time) • Web/E-commerce projects Operating with Discipline • Supply chain optimization • Further SAP integrations • Transportation management Growing the Enterprise • New products/Smart Grid • Acquisitions • Transmission/International Developing our • Build depth with focus on Engineering • Hi potentials into new roles People -18- Key initiatives to drive growth and operating performance 2013 INVESTOR DAY Transmission Outlook North American Transmission Spend ($ Billions) 16 14 12 10 8 6 4 2 0 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E Source: Edison Electric Institute -19- Growth rate slowing 2013 INVESTOR DAY Transmission Industry Forecasts Average Growth Forecast by Analysts 20% % Growth 16% 12% 8% 4% 0% 2010 2011 2012 2013 2014 -20- Transmission projects drive growth but at a slower pace 2013 INVESTOR DAY Smart Grid HPS role • Distribution automation • Fault location • Isolation and restoration Current products • AR switch • Recloser • Sectionalizer The greatest source of outages occurs between the substation and the home. Future products Future Products: • 3 phase recloser • 3 phase sectionalizer • Motor operators • Capacitor and padmounted switches • Vacuum switches • SCADA -21- Products that support a wide range of smart applications 2013 INVESTOR DAY New Product Conversion Dashboard measure for all Business Units and Sales Force $25M new product sales in 2013 Monthly tracking of activities with key customers Tracking key steps: target, evaluation, approval, order What’s Next – Product Development Funnel Events to ID and prioritize product gaps -22- Active engagement in driving NPD growth 2013 INVESTOR DAY Value-Added Service MTO Lead Time On-Time Deliveries 95% 39 93% 37 91% 35 89% 33 87% 31 85% 29 2010 2011 2012 (In Days) 2010 2011 2012 -23- Best in class service, support, performance and cost 2013 INVESTOR DAY E-Commerce EDI Orders Non EDI Orders 50 Electronic Data Interchange (EDI) 40 • 46,000+ orders processed in ’12 • 65% of total orders are EDI 30 20 10 Vendor Managed Inventory (VMI) • Proven productivity results • 2X growth in VMI volume in ’12 • 50 locations - $50M sales 0 2010 2011 VMI Order $M 2012 VMI Locations Industry Data Warehouse (IDW) 50 40 • 23,000+ SKU’s in IDW • Platinum status 30 20 10 0 2009 2010 2011 2012e -24- E-Commerce solutions drive customer loyalty 2013 INVESTOR DAY International Growth $Millions 160 Power Systems Rest of World Orders 140 120 ROW 2-3x larger than North America Growing faster Small HPS share Product (IEC) limitations Develop or acquire IEC products Expand sales and engineering resources Localize 100 80 60 40 20 0 2009 2010 1.111 Latin America 2011 Asia 1.112 2012 Europe 1.1113 Middle East Africa -25- Huge opportunity for growth 2013 INVESTOR DAY HPS Platform Timeline 2013-14 2012 Add more engineers 7% sales growth 23% OP growth New product rollouts New product vitality 6% Service execution Accelerate IEC product development Execute new product spec conversions Add to international sales force 2015 North America share growth Accelerated international growth $25M+ annually in new products New product vitality > 8% LCC/Supply Chain optimization - On-time % - Lead time reduction - Storm response SAP - enclosures business E-Commerce investments SAP – Electro Composite and Brazil -26- 2013 INVESTOR DAY HPS Summary Well positioned • Compelling value proposition • Attractive markets Opportunities to expand • Hubbell Power Systems –is peace of mind New products, markets, geographies Substantial acquisition pipeline -27- Best people, best products, best service create great opportunities 2013 INVESTOR DAY Lighting Scott Muse Jim Decker Kevin Poyck Business Overview ($Billions) Electrical Segment Segment Platform Electrical Systems LIGHTING Addressable Market Size $ 8 2012 Sales $ 0.7 Business Units Power Systems Commercial and Industrial Residential Controls -29- 2013 INVESTOR DAY Lighting Strategic Roadmap #1 Specification Brands # 1 Residential Brands Increase Market Share and Enhance OP Margins Targeted Market Penetration New Product Technology and Development Continuous Cost Reduction Superior Customer Support -30- Four primary strategies 2013 INVESTOR DAY Key Vertical Markets Hospitals Schools Health Care Education Industrials Federal Government Residential Home Building GSA -31- Focus to maximize market penetration 2013 INVESTOR DAY Solid State Lighting Focus Hubbell Lighting’s LED Adoption Leading Technology Deployment • Center of Excellence • Modular, Scalable Solutions Projection 30%+ 30% • Reliability Testing Evolving Supply Chain Management 20% 10% Compelling Value Proposition 0% Complete Solutions Provider 2007 2008 2009 2010 2011 2012 2015 -32- LED represented 21% of total sales in Q4 2012 2013 INVESTOR DAY Solid State Lighting Supply Chain Legacy Technologies Emerging Technologies -33- Amount of Hubbell Lighting value-add increases with SSL 2013 INVESTOR DAY 2012 IES Progress Report Fifth consecutive year, more acceptances than Endura PGL LED EV LED Series Altitude LED LED Highbay any other company 20 Products -34- 64 awards/recognitions in last 24 months 2013 INVESTOR DAY Relight/Retrofit Kevin Poyck Relight/Retrofit Market Focus Compelling ROI = 1 to 3 Years 81% Lighting and Controls Energy Savings 2.2 M Pre-1980 Lighting Maintenance Savings .5 M Some update since 1980 Utility Rebates EPAct Tax Incentives 19% 2.7M Pre-1980 Commercial Buildings -36- Relight/Retrofit helps offset new construction softness 2013 INVESTOR DAY Relight/Retrofit Market Focus Multiple Market Channels Energy Service Companies National Accounts Electrical Distribution -37- Access to Relight/Retrofit through multiple channels 2013 INVESTOR DAY Relight/Retrofit Market Focus Relight/Retrofit LED Fixtures Complete Product Solutions Indoor / Outdoor/Parking Garage • Solid State Lighting • Lighting Controls Systems Financing Programs e-poc LED LLT LED Lensed Troffer Cimarron LED LED Highbay D2 Retrofit LED Downlight LEDGarage Wireless Lighting Controls -38- Well positioned to penetrate Relight/Retrofit markets 2013 INVESTOR DAY Residential Lighting Jim Decker Residential Lighting Focus Progress Lighting Sales Channel Shift 2006 Current -40- Diversified market channel coverage 2013 INVESTOR DAY Residential Lighting New Construction Markets Single Family • Market Recovery • National Agreements • Regional/Local Agreements Multifamily • Demographics driving growth • Strong market through 2014 Light Commercial • Assisted Living • Hospitality -41- Well positioned for residential rebound 2013 INVESTOR DAY Residential Lighting Remodel Market Internet • Build brand with key internet retailers • Driving Search Engine Results • Social Media to Consumers Home Centers • Core Vendor − All Stores − Special Order/HD.com Showrooms • Premier National Showroom Chain – Primary Lighting Supplier • Merchandising Services – Leverage premier brands -42- Multi channel market coverage 2013 INVESTOR DAY Residential Lighting Innovations Residential LED Fixtures New Low Cost LED Technology • Low cost adder to incandescent • Scalable module approach • Warm, even light distribution • Dimmable • Multiple Product Applications Close to Ceiling Recessed Downlight Close to Ceiling Wall Sconce Outdoor Lantern -43- New alternative to compact fluorescent 2013 INVESTOR DAY 2013 Strategic Objectives Serving our Customers • Superior Customer Support Capabilities • Enhance Service Through Technology Operating with Discipline • Continuous Cost Reduction • Lean Six Sigma • Inventory/Supply Chain Management Growing the Enterprise • Sales Force Optimization • New Technology Penetration • Acquisitions Developing our • Customer Centric Culture • Talent Management People -44- Key initiatives to drive growth and operating performance 2013 INVESTOR DAY Talent Management Recruitment and Onboarding • Target position pipeline • College Internship and Recruitment Program Training and Development • Development plans for High Potentials • Customer Centric Culture Training Motivate and Retain • Management Mentoring Program • Annual Talent Review and Succession Planning -45- Ongoing focus on increasing talent 2013 INVESTOR DAY HLI Platform Timeline 2014-15 2013 2012 C&I C&I C&I • Weak new construction • Strong NPD sales/LED adoption • Sales agent churn Residential • Improving market conditions • Diversified channel model • Increased share Relight/Retrofit • Improving market conditions • Accelerate NPD/LED sales • Sales agent churn Residential • Market continues to strengthen • Major NPD launch • Continued share gain Relight/Retrofit • Favorable market conditions • LED cost curve supports growth • Double digit growth • Strengthen lighting package with complementary acquisitions • LED sales >30% adoption • Share gain Residential • Leverage improved market conditions • LED products adoption • Share gain Relight/Retrofit • Favorable market conditions • New products focus on total cost of ownership • Share gain • Continued market growth • Well positioned across channels • Share gain -46- Continuous performance improvement 2013 INVESTOR DAY 2013 Plan Summary Remain a leading industry player #1 Specification Brands #1 Residential Brands Targeted Market Penetration Market driven organization Focused on greatest opportunities for growth New Product Technology Development Increase Market Share Enhance OP Margins Superior Customer Support Cost Reduction Relight / Retrofit Residential Market Rebound Growth Solid State Lighting Lighting Controls -47- Key initiatives to drive growth and operating performance 2013 INVESTOR DAY 10 Minute Break Electrical Systems Gary Amato Craig Soucy John Szupiany Business Overview ($Billions) Electrical Segment Segment Platform ELECTRICAL SYSTEMS Addressable Market Size $ 12.0 2012 Sales $ 1.4 Connectors, Grounding & Tooling Business Units Wiring Systems Lighting Power Systems Harsh & Hazardous Industrial Commercial Construction -50- 2013 INVESTOR DAY 2013 Strategic Objectives Serving our Customers • World class experience • Building high quality, innovative new products • E-Commerce and VMI capabilities Operating with Discipline • Strategy is successful • The playbook is working • SAP integrations – pace accelerating Growing the Enterprise • Speed with certainty • Increase importance to our distribution partners • Acquisitions • Energized team with expanding bench strength Developing our • Focus on increasing engineering talent People • India expanding competencies -51- Key initiatives to drive growth and operating performance 2013 INVESTOR DAY Serving Our Customers New product expansion • NPVI more visible KPI for BURNDY • View from 1 and 3 Year Perspective • Promote as competitive advantage Marketing theme and ad campaign • New Marketing Tag Line Connecting Power to your World • More Hubbell presence in all media • Ads focus on major project successes SMALL HYDENT UNIRAP EXOTHERMIC SPACERS &VIBRATION SUBSTATION CM&R MECHANICAL -52- 2013 INVESTOR DAY Key Initiatives Harsh & Hazardous Invest in US and World certifications Invest in training • Milano – Italian and Middle Eastern Engineers Houston, TX • New Demo Center in Dubai Reading, PA New product development Dubai - NEW! • LED lighting • VOIP communications • Wireless security Acquisitions • Vantage explosion proof connectors -53- Global focus 2013 INVESTOR DAY Harsh & Hazardous LED Developments Generation II Now Available Generation IIa Q4 2012 Generation III Q1 2013 Vaportight, Dust Ignition Proof, and Emergency KFL Floodlight Q3 2012 -54- 1 Team Hubbell 2013 INVESTOR DAY Explosion Proof Global Control Station Hazardous location applications Globally rated • • • North America Europe International Multi brand marketing strategy Developed via One Hubbell synergy • • • • Killark Hawke Hubbell Wiring Hubbell Asia Limited Launch scheduled for 2013 -55- 2013 INVESTOR DAY Harsh & Hazardous NPD WiFi Telephones and Amplified Speakers • IEEE 802.11 Compliant • Camera Telephones VOIP Hazardous Phones IEC and ATEX Zone UL Class I DIV 1 New GUI for Plant Wide Systems Ethernet, IP and CANBUS Technology -56- Many exciting opportunities 2013 INVESTOR DAY Connectivity Growth Opportunities National Oilwell Varco (NOV) • Vantage Connector certifications (divisional) required Other oil & gas service companies • Requiring U.S. divisional certifications Nuclear power reactor sites • Duke Energy (McGuire 1 & 2 + Catawba 1 & 2) • Duke also has Oconee 1, 2 & 3 • There are approx. 104 reactor sites in the U.S. alone -57- Significant upside 2013 INVESTOR DAY Key Initiatives – Industrial Electrical Fire Pump Controller DC-DC Solid State Magnet Controls ICD/Cableform new product development • Metron fire pump controller • Cableform smart crane diagnostics • Joint ICD/Cableform solid state magnet controls Smart Crane Display ICD/Gleason New Market Development • East oil/gas market, joint efforts with H&H Stage Cable Reel • Entertainment industry: Gleason cable reels • DC DevSolar energy market (DC devices) -58- Building a bigger business 2013 INVESTOR DAY High Voltage HV Bottom of Larger Transformer Cycle • UHVDC New Technology • New Products for Distribution Testing Where are we winning On Site Testing of cable AC + DC Geographic Opportunity -59- Medium and longer term prospects strong 2013 INVESTOR DAY Wiring/Commercial Construction/Connectors John Szupiany Key Initiatives – Cross Sell NPD Investments - yielding higher than average OP - share gain Power, data, AV, delivery systems growth strategy Next gen commercial device life cycle planning One Hubbell cross platform sales and development Continue leadership in high margin industrial products -61- Back on the offensive after years on defense 2013 INVESTOR DAY Key Initiatives – Commercial Construction Leverage Hubbell Position in Distribution Retail • Cross sell products/brands into “Big-Box” Electrical distribution • Create product line and brand synergies TAYMAC acquisition • All we thought it would be • Largest WP offering available • Buy more because Hubbell owns it • Big-Box: Same Hubbell “Halo” Can do more deals like this in this space! -62- Hubbell acquires another #1 brand 2013 INVESTOR DAY Key Initiatives – Connectors, Grounding, Tools Wiley acquisition in adjacent space New Additions • Continental - Grounding • More possible Ignition Systems & Other Accessories Exothermic Molds Plastic Connectors Geothermal Connectors ACSR Cutting and Crimping Tools Exciting new products -63- Increasing our value with electrical distributors 2013 INVESTOR DAY Acquisitions Craig Soucy Acquisitions – Increased Capability Have added dedicated resources • Added to business and corporate level • Ideas from everywhere Developed detailed integration playbook • First 60 days with milestones Faster systems integrations by an experienced team Speed with Certainty – without compromise! -65- Cycle time for closing deals has accelerated – more capable organization 2013 INVESTOR DAY BURNDY to Hubbell #1 Brand Sourcing Savings Pull Through Big Box New Utility Vitality ERP System Safety Culture 1+1>2 -66- Acquisition sum is greater than the parts 2013 INVESTOR DAY BURNDY Acquisitions • Connectors used in solar applications • Grounding applications Ignition Systems & Other Accessories Exothermic Molds Both Brands Add Value to Our Distribution Partners -67- Closing their own deals – more opportunities exist 2013 INVESTOR DAY Developing Our People – India Growth 2012-2013 FTE Growth 200 $22,100 180 $20,700 $18,900 Raise Maturity Level Per FTE Cost 160 Operational and productivity improvement Quality – CMMI, ISO Risk Management – continuity planning 140 120 100 HBES 80 HBBS 60 40 20 Service Expansion for Company Increase engineering to meet demand SAP business support team Increase transactional support 0 Jan-12 Dec-12 Jul-13 Expand Competencies Engineering – BIM, FEA, Casting, etc. Sourcing – India suppliers network India as a Market – Sales and distribution network People, Process / Continuous Improvement Management development program Customer focus initiative Training – Project management. SAP, inventor -68- 2013 INVESTOR DAY HES Platform Timeline 2013 2012 Acquisitions- more -faster BURNDY: - 100M+ Year - Accretive - Look for big one - Expanded - Acquiring on it’s own • Wiley, Continental Wiring back on the offensive - Shared selling - Shared NPD - Operational cooperation Harsh and Hazardous - Very strong - NPD Pipeline - LED –Controls-Wireless Industrial - Bottom of the cycle - Acquisitive - NPD India Strategy-In place - Cross Hubbell Operations Business systems Engineering HAL China - Cross Hubbell - Adding HLI, HEP, HES - Project Sandlot 2014-15 Higher Sales with margin expansion Positive Cycle Peaks - Late 2013 - Accelerates 14-15 Multiple $10-$50M acquisitions Motivated, matrixed, localized management team Eliminate Silos SAP FASTER - Acquisition in 150 days Commercial Construction - Strong - Acquisitive -69- Proven track record of achievement 2013 INVESTOR DAY Financial Review Bill Sperry Full Year 2012 Summary Sales increased 6% compared to 2011 • Both segments contributed • Acquisitions contributed 2% Margin improvement of 70 bps • Price net of commodity cost was a tailwind Free cash flow equal to net income Increased Dividend twice during the year Closed on 4 acquisitions during the year -71- Steady execution 2013 INVESTOR DAY Full Year 2012 Results ($Millions except EPS) Sales (a) FY 11 FY 12 $2,872 $3,044 Variance +6% Operating Profit Margin % $424 14.8% $472 15.5% +11% +70 bps Tax Rate 30.7% 31.6% +90 bps Net Income $268 $300 +12% EPS - Diluted $4.42 $5.00 +13% Free Cash Flow (a) $280 $300 +7% Non-GAAP Financial measure – see appendix 1 -72- Record sales and earnings in 2012 2013 INVESTOR DAY Full Year 2012 Electrical Segment Results ($Millions) Sales $2,200 Markets + 6% $2,115 • Industrial mixed: up due to higher energy markets $2,004 • Higher residential demand $2,000 • Non-residential aided by strong renovation • Acquisitions added 2% $1,800 FY 11 FY 12 Operating Profit Performance + 8% $320 $300 $304 14.4% • Price realization and lower commodity costs • Higher costs in excess of productivity $282 $280 $260 16% 14% • Less favorable product mix 14.1% 12% $240 FY 11 FY 12 Operating Profit Operating Profit % -73- Modest market growth with margin expansion 2013 INVESTOR DAY Full Year 2012 Power Segment Results ($Millions) +7% Sales $1,000 $900 Markets $930 • Increased distribution spending $867 • Transmission projects active $800 • Price added 2% $700 $600 FY 11 FY 12 Operating Profit $200 20% $168 $175 $150 $125 Performance +19% 18% $142 18.1% • Increased sales • Price realization and productivity in excess of cost increases 16% 16.3% 14% $100 FY 11 Operating Profit FY 12 Operating Profit % -74- Strong revenue growth and margin expansion 2013 INVESTOR DAY Full Year 2012 Cash Flow ($Millions) FY 2011 FY 2012 Net Income Depreciation and Amortization Changes in Working Capital Other Net Cash Provided By Operating Activities $268 $68 ($22) $21 $335 $300 $67 ($45) $27 $349 Capex ($55) ($49) $280 $300 Free Cash Flow (a) Key Drivers: • Higher net earnings • Increased working capital primarily due to volume (a) Non-GAAP Financial measure – see appendix 1 -75- Free cash flow met target of equal to net income 2013 INVESTOR DAY Capital Deployment Cash Deployment ($Millions) ∼ 2% Sales $49 $140M Invested ∼$200M Returned To Shareholders $91 $122 $76 2012 Capex Acquisition Dividend Share Repurchases $100 - $300 30 – 50% of Net Income Offset Options + Future -77- 2013 INVESTOR DAY Acquisitions Last 18 Months • Connectors used in solar applications • Capacitor switches • Sectionalizer cabinets • Burndy add-on • Fire pump controls • Bring volume into legacy footprint • Industrial controls • Hazardous location plugs and connectors • Pipe and electrical connectors • Extends reach in steel and mining markets • Weatherproof enclosures • Strong product design • Good response from distributors -78- Have been active – looking to invest more 2013 INVESTOR DAY Outlook Order Trends Q1 2013 QTD rebounded from weak December Non-residential • New Construction • Relight/Retrofit Industrial • Energy markets • Industrial production • High voltage test equipment Utility • Transmission • Distribution Residential • Housing recovery continues -80- Early indicators positive 2013 INVESTOR DAY 2013 Outlook – End Market Growth Estimated % - Hubbell Sales 2 to 4% Utility 0-2% Industrial Residential 10% Nonresidential 1 to 3% Modest overall growth expected in end markets -81- 2013 INVESTOR DAY 2013 Outlook – Segment Sales Growth Segments (2012 Sales) Power 4 to 6% • Transmission grows at slower rate • Distribution at GDP • Favorable acquisition 3 to 5% • Non-residential slow recovery • Residential strong • Industrial mixed 31% Electrical 69% -82- 3 to 5% overall sales increase expected 2013 INVESTOR DAY 2013 Operating Margin Improvement + Organic Volume 15.5% Price + Productivity Offset Cost Increases 15.9% - Acquisitions 2012 2013E -83- Continued margin expansion expected; strong contribution from base 2013 INVESTOR DAY Outlook – 2013 Sales expected to increase approximately 3-5% compared to 2012 • Expect slower start before economy starts to improve in 2H 2013 Operating margin expected to increase by approximately 40 bps • Acquisitions not additive to margin in first full year • Assume pricing to offset any commodity cost increases Free cash flow expected to equal net income Tax rate expected to be approximately 31.5% • Two year benefit of R&D Tax credit included -84- Anticipate another strong year in 2013 2013 INVESTOR DAY Conclusion Dave Nord Hubbell Strategic Objectives Reliable Electrical Solutions Our Strategic Objectives Are The Critical Few Serving Our Customers Operating with Discipline Growing the Enterprise Developing Our People -86- 2013 INVESTOR DAY Where we are heading… Today OP Margin EPS • Participate in secular growth • Rapid new product cycle • Accelerated acquisitions $4B+ 15.5% • Operating with discipline • Streamline footprint • Productivity initiatives 17+% $5.00 • Generate attractive returns 10+% CAGR $3B Sales 2017 -87- Transforming into a larger more profitable organization 2013 INVESTOR DAY Appendix Appendix 1 Reconciliation of Non-GAAP Financial Measures Free Cash Flow Hubbell Incorporated Reconciliation of Net Cash Provided By Operating Activities (GAAP) to Free Cash Flow Free Cash Flows ($Millions): Net Cash Provided By Operating Activities Capital Expenditures Free Cash Flow Twelve Months Ended December 31, 2011 $ $ $ 335 (55) 280 Twelve Months Ended December 31, 2012 $ $ $ 349 (49) 300 Notes: Management believes that free cash flow provides useful information regarding Hubbell’s ability to generate cash without reliance on external financings. In addition, management uses free cash flow to evaluate the resources available for investments in the business, strategic acquisitions and further strengthening the balance sheet. -89- 2013 INVESTOR DAY