Federal Tax Tips

advertisement

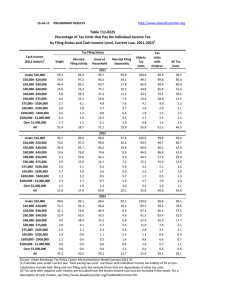

Tax Saving Tips and Updates for 2015 Uncertainty is a word that captures the federal tax environment. With the 2016 U.S. election cycle in full bloom, it is difficult to determine which reform or extension bills will be enacted by a partisan Congress, or when. Given that uncertainty, tax planning can be tough. This brochure should help you get through what we do know will affect your tax posture for 2015. Please note: The PICPA worked carefully to prepare this guide, but it cannot be used as official tax advice that would protect taxpayers from penalty due to the complexity of tax law, individual taxpayer facts and circumstances, and changes enacted after this writing. We encourage taxpayers to seek advice from our member CPAs about the items contained in this brochure, as well as other tax issues and planning opportunities. Filing Basics Filing Status Taxpayers can file as single, married filing jointly, married filing separately, head of household, or qualifying widow(er) if the circumstances legally support the status chosen. If you are married and filing jointly, you can take advantage of certain tax deductions, tax credits, and benefits not available to couples filing separately. Unmarried taxpayers may file as single or, if they qualify, head of household. Rates For 2015, the top rate is 39.6 percent for single taxpayers making more than $413,200, head of households making more than $439,000, and married filing jointly taxpayers and surviving spouses making more than $464,850 (or $232,425 if married filing separately). Below that, the ordinary income tax rates are 10, 15, 25, 28, 33, and 35 percent, with different brackets for each type of filer. The Affordable Care Act includes additional Medicare taxes for 2015 on earned income and unearned income. For earned income, the Medicare contribution tax rate on wages, compensation, or self-employment income is an additional 0.9 percent, if that type of income exceeds certain thresholds. The threshold levels for 2015 are $250,000 for married filing jointly ($125,000 if married filing separately) and $200,000 for all other taxpayer filing statuses. For unearned income, see the “Net Investment Income Tax” section in this brochure. Exemptions For 2015, the exemption amount has increased to $4,000 for yourself, your spouse, and each of your dependents who are qualifying children or relatives. The exemption is subject to phase-outs beginning at $258,250 (single), $284,050 (head of household), $154,950 (married filing separately), and $309,900 (married filing jointly); with a complete phase-out at $380,750 (single) and $432,400 (married filing jointly). Deductions The standard deduction amounts have increased slightly for 2015 as follows: $6,300 if single or married filing separately, $12,600 for married filing jointly or qualifying widow(er), and $9,250 for head of household. Taxpayers who are 65 and older or are blind receive an additional standard deduction of $1,250 for married filing jointly or separately, or $1,550 for single or head of household. For individuals claimed as a dependent on another tax return, the 2015 standard deduction is the greater of $1,050 or $350 plus earned income, not to exceed the standard deduction amount for those who are not dependents. The American Tax Relief Act (ATRA) of 2012 reduced itemized deductions by 3 percent of any excess adjusted gross income (AGI) over $258,250 (single), $284,050 (head of household), $154,950 (married filing separately), and $309,900 (married filing jointly). ATRA also increased the AGI limitation floor from which you can claim unreimbursed medical expense deductions from 7.5 percent of AGI to 10 percent of AGI before such deductions can be claimed. There is a temporary exemption through 2016 for individuals age 65 and older and their spouses, allowing them to continue using the prior www.picpa.org/resources Tax Saving Tips and Updates for 2015 7.5 percent AGI limitation. The 2 percent floor for unreimbursed business expenses and the 10 percent floor for casualty losses in excess of insurance reimbursements also apply in 2015. Mileage and vehicle costs can be significant considerations in computing itemized deductions as well. For 2015, the business mileage rate is $0.575 per mile. The medical and moving mileage rate is $0.23, and the charity mileage rate is $0.14 per mile. Retirement Savings Tax Breaks IRAs You may contribute up to $5,500 to a traditional or Roth IRA in 2015. Those 50 or older at year-end can make an additional catch-up contribution of $1,000. Contributions to traditional IRAs may be deductible depending on several factors, including filing status, and the deductible amounts are phased out at higher levels of AGI. Nondeductible contributions are also allowed up to the applicable limits. Distributions are fully taxable as ordinary income, unless there were historical nondeductible contributions. Roth IRA contributions are not deductible, but earnings accumulate tax-deferred and may be withdrawn tax-free and penalty-free if you meet certain requirements. Allowable contributions, however, are phased out at higher levels of AGI, depending on filing status. Employer-Sponsored 401(k)s Pretax contributions to traditional 401(k) plans reduce taxable wages. Matching contributions and income earned within your plan are tax-deferred until distributed. The employee contribution limit for 2015 is $18,000. Employees age 50 or older may make an additional catch-up contribution of $6,000 for 2015. Distributions are fully taxable as ordinary income. Roth 401(k) contributions are made with after-tax dollars. Earnings accumulate tax-deferred, and may be withdrawn tax-free and penalty-free if you meet certain requirements. Taxpayers are generally allowed to roll www.picpa.org/resources over certain pretax qualified retirement accounts such as traditional IRAs and 401(k)s to designated Roth IRA accounts. Such rollovers are generally taxable on the amount of pretax contributions in the traditional plan. Due to the complexity of all the rules related to retirement plans, you should consult with your CPA if you are receiving, or are about to receive, retirement account distributions. Saver’s Credit To encourage taxpayers to contribute to qualified retirement plans, Congress provides a “saver’s credit.” For individual elective contributions up to $2,000, there is up to a 50 percent credit, for a maximum credit of $1,000. The credit is phased out, however, for higher-income taxpayers. Tax Breaks and Other Considerations for Homeowners Interest, Points, and Certain Taxes Home mortgage interest on up to $1 million of home acquisition loans secured by your principal residence or second home is fully deductible. You also may deduct interest on up to a $100,000 home equity loan or line of credit. Points paid to secure a loan for the purchase or improvement of a principal residence usually are fully deductible in the year paid. However, points paid to refinance an existing mortgage must generally be deducted over the life of the loan. Real estate taxes and state and local property taxes on tangible property are also deductible, as are your state and local income taxes. Exclusion of Certain Capital Gains upon Sale If you sell your principal residence, you can exclude up to $250,000 in gains ($500,000 if married and filing jointly). To qualify, you generally must have owned and used your home as a principal residence for at least two years during the five-year period ending on the date of sale. Limitations may apply if you had any “nonqualified use.” First-Time Homebuyer Tax Credit Pay Back Taxpayers who claimed a firsttime homebuyer credit on a home acquired in 2008, 2009, or 2010 may have to repay the credit under certain circumstances, including a subsequent sale to a related party, an abandonment or destruction of the home, or conversion of the home to a business or rental property. Home Loan Forgiveness Could Now Be Taxable Another provision that expired Jan. 1, 2015, had allowed homeowners who received mortgage relief to avoid hav- Tax Saving Tips and Updates for 2015 ing that amount included in their taxable income. Unless Congress passes an extenders package, any such relief in 2015 could be taxable. Energy Tax Credit Incentives There is a 30 percent tax credit (generally without limit) available through 2016 of the cost of alternative energy equipment that you installed on or in your main or second home. Qualified equipment includes solar hot water heaters, solar electric equipment, and wind turbines. Additionally, if an extenders bill passes, there may be a 10 percent credit up to $500 for qualifying energy-efficient improvements. Child- and Education-Related Tax Breaks Child Tax Credit The Child Tax Credit is still worth $1,000 for each qualifying dependent child who is under age 17 at the end of 2015, and it may be partially refundable. The credit, however, phases out when modified AGI exceeds certain levels. Child and Dependent Care Credit Parents who, in order to work, pay for the care of a dependent under age 13, whether the care is provided outside or inside the home, may be eligible for a nonrefundable tax credit of between 20 percent to 35 percent of qualifying expenses, depending on income level. For 2015, the maximum amount of qualifying expenses on which the credit can be claimed is the lesser of the amount of qualifying expenditures, $3,000 for the care of one dependent or $6,000 for at least two qualifying children, or the taxpayer’s earned income. Earned Income Tax Credit If a taxpayer has any earned income, whether there is a qualifying child or not, there may be a refundable earned income credit of up to $6,242, depending on filing status, number of qualifying children, amount of earned income, and AGI amount. It is refundable. Education Tax Benefits An American Opportunity Tax Credit of up to $2,500 per qualifying student for qualifying expenditures is available for each of the first four years of college, and up to 40 percent of the credit is refundable if total tax is cut to zero. Additionally, a Lifetime Learning Credit of 20 percent of up to $10,000 of eligible expenses per year is available for undergraduate, graduate, and professional degree courses. Both credits phase out for higher income individuals, and you cannot claim both credits for the same student in the same tax year. There is also a deduction for AGI, available even if you don’t itemize, of up to $2,500 for qualifying student loan interest, although it also phases out for higher income taxpayers. If an extenders bill passes, there may also be an alternative tuition deduction of up to $4,000, and a teacher’s maximum $250 deduction. Tax Considerations for Investors Capital Gain and Loss Planning Planning when to realize capital gains or losses can be extremely beneficial. Such planning should consider the continued risk (or benefit) of holding an investment longer, current and future cash needs, the “wash sale” rules that disallow certain losses, and current vs. future tax rates. For 2015, net capital losses (including any net capital loss carryovers) are still fully deductible against current year capital gains. If capital losses exceed capital gains, you can still deduct up to $3,000 in net capital losses against ordinary income ($1,500 if married filing separately). Any remaining capital losses can still be carried over indefinitely to successive tax years to offset capital gains in the future. Rates on Capital Gains and Dividends For 2015, there is a top (preferential) rate of 20 percent on net long-term capital gains and dividends. Specifically, the preferential tax rate is 0 percent to the extent the income would have been taxed in the 10 percent or 15 percent tax rate bracket if it were ordinary income; 20 percent to the extent the income would have been taxed in the 39.6 percent tax rate bracket if it were ordinary income; and 15 percent for all other taxpayers. (Note, there are different rates on gains from certain assets such as collectibles, depreciable real property, and qualified smallbusiness stock.) Interest income and short-term capital gains (i.e., held 12 www.picpa.org/resources Tax Saving Tips and Updates for 2015 Section 179 Expense Section 179 expense election for acquiring new or used tangible personal property in a business is $25,000 in 2015. The limitation is reduced dollar-for-dollar if acquisitions exceed $200,000, and is limited to the business’s taxable income. months or less) continue to be taxed at ordinary rates, now as high as 39.6 percent in 2015. local income taxes properly allocable to items included in net investment income. Net Investment Income Tax The health care law brought with it an additional 3.8 percent tax on certain net investment income if a taxpayer’s modified AGI exceeds certain threshold levels. For 2015, these levels are $250,000 for married filing jointly (or $125,000 if married filing separately) and $200,000 for all other filing statuses. In general, net investment income includes, but is not limited to, interest, dividends, capital gains (after offset of capital losses), rental and royalty income, certain annuities, and income from businesses that are passive activities to the taxpayer, including gains on their sale. Kiddie Tax Children’s unearned income may be subject to tax at the parents’ highest applicable marginal rates for the type of unearned income. This is known as the “Kiddie Tax.” For 2015, any net unearned income over $2,100 will be taxed at the applicable parental rates if the child is in one of these three categories as of year-end: under age 18, age 18 and does not have earned income exceeding 50 percent of his or her support, and age 19 through 23 and is a full-time student who does not have earned income exceeding 50 percent of his or her support. The amount exempt from tax and the amount taxed at the child’s rate increases to $1,050 in 2015 from $1,000 in 2014. The net investment income tax will not apply to any amount of gain that is excluded from gross income for regular income tax purposes, such as the exclusion of the first $250,000 ($500,000 in the case of a married couple) of gain recognized on the sale of a principal residence. To calculate your net investment income, your investment income is reduced by certain expenses properly allocable to the income, such as investment interest expense, investment advisory and brokerage fees, expenses related to rental and royalty income, and state and Change in Business Return Due Dates As part of a short-term highway funding bill, Congress changed certain tax return due dates as follows: partnership returns are now due on the 15th day of the third month following year-end (like S corps), and C corps are due the 15th day of the fourth month following year-end. There also were changes to extended due dates. These changes are generally effective for tax years beginning after Dec. 31, 2015. Changes to Filing Deadline Typically the deadline for filing your income tax return with the IRS is April 15. However, due to a legal holiday in the District of Columbia, the filing deadline for 2015 is Monday, April 18, 2016. NOTE This text was prepared in August 2015. Additional legislation may be passed before year-end. The PICPA offers resources for a variety of financial topics. Visit www.picpa.org/resources to learn more. Other Tax Considerations Alternative Minimum Tax (AMT) AMT exemptions for 2015 are $53,600 for single and head of household filers; $83,400 for married people filing jointly and qualifying widows or widowers; and $41,700 for married people filing separately. The amounts are phased out 25 cents for each dollar of AMT income over those thresholds. The Pennsylvania Institute of Certified Public Accountants, with more than 22,000 members, advocates to strengthen the accounting profession and serve the public interest. 8904/15 www.picpa.org/resources