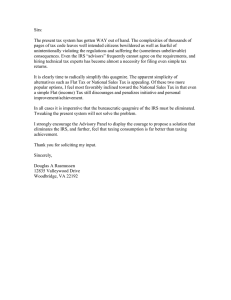

Taxing Times, Volume 11, Issue 3, October 2015

advertisement