Document 17736008

advertisement

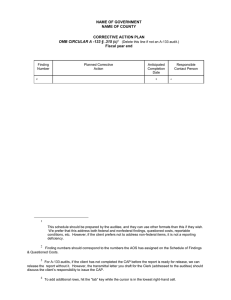

[ENTITY NAME] [COUNTY NAME] COUNTY CORRECTIVE ACTION PLAN 1 2 CFR § 200.511(c) [Fiscal year end] Finding Number 2 Planned Corrective Action Anticipated Completion Date Responsible Contact Person 3 1 2 CFR 200, Subpart F, § 511(c) (Uniform Guidance) requires the auditee to prepare a corrective action plan (CAP). This is an example of a corrective action plan but auditees can use other formats. Notes: The CAP should address both federal audit findings and all findings related to the financial statements which are required to be reported in accordance with Government Auditing Standards included in the current year auditor’s report. The CAP must provide the name(s) of the contact person(s) responsible for corrective action, the corrective action planned, and the anticipated completion date. If the auditee does not agree with the audit findings or believes corrective action is not required, then the corrective action plan must include an explanation and specific reasons. See also the AICPA Single Audit Guide, Chapters 20 & 23 as well as 2 CFR 200, Subpart F, § 511(c), for additional guidance. 2 Finding numbers should correspond to the numbers the auditor assigned on the Schedule of Findings [and Questioned Costs]. 3 To add additional rows, hit the “tab” key while the cursor is in the lowest right-hand cell.