Global Production Factoryless Goods Producers (FGPs) Mark de Haan 9th AEG Meeting

Mark de Haan 9th AEG Meeting")

Global Production

Factoryless Goods Producers (FGPs)

Mark de Haan

9th AEG Meeting

8-10 September 2014, Washington DC

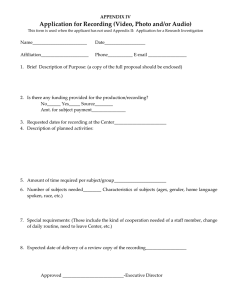

A factoryless goods producer arrangement

Consumer

(domestic or abroad)

= information (IPP related)

= transactions in goods

Principal,

GFP

Final consumer product

(domestic economy)

Intermediate product

Contract producer

(abroad) blueprints of production

IPP investment

Material inputs

Starting point of the paper

Previous conclusions of the AEG at its 8 th meeting are the following:

– FGPs are manufacturers, i.e. goods producers, and should not be classified as traders (following ISIC Rev.4);

– FGPs should be identified in ISIC subclasses separate from ‘regular’ manufacturers;

– Boundary between FGPs en traders depends on IPP inputs and other ‘FGP specific’ inputs (e.g. innovation, supply chain management, marketing)

Two key issues presented in this paper

1. Recording of output and international trade flows within a factoryless goods production arrangement, from the perspective of the FGP and contract manufacturer;

2. Delineation of FGPs within the global production arrangements typology:

‐ Factoryless goods production

‐ Merchanting

‐ Goods sent for processing

4

1. Recording of output and trade flows

Output of the FGP; good or trade margins?

– Special case of manufacturing;

– Which implies the FGP’s main activity is connected to physical transformation (providing the blueprints);

– BPM6 (par.10.42): merchant as organiser of a global manufacturing process…..

– IPP services dominate substantially the value added of

FGPs which exceeds the notion of a trade margin

The FGP’s output is a good

Purchases from the contract producer are intermediate consumption

5

1. Recording of output and trade flows

Output of the contract producer under a factoryless arrangement; a good or a service?

– Principal owns (some of) the material inputs: contract producer provides a manufacturing service.

– Principal owns the IPP inputs: contract producer provides..?

Factoryless versus Processing, key differences:

‐ Contractor owns material inputs and inventories;

‐ Contractor takes more risks and plays a more active role (than under a processing arrangement).

6

1. Recording of output and trade flows

…in favour of recording a service:

– The contract producer is not the economic owner of the manufactured goods

– The contract producer plays a similar role as under a goods sent for processing arrangement: i.e. factoryless is a special case of processing

– A good cannot be produced twice. As the physical characteristics are not changed by the FGP, the transaction between the contract producer and the FGP must be a service.

7

1. Recording of output and trade flows

…in favour of recording a good:

– FGPs are not unique in exerting control over a supplier’s output

– Recording a service leads to blurred production accounts

– In economic terms the contract producer’s output differs from the final consumer good (‘a good cannot be produced twice’)

– Under a factoryless arrangement the contact producer faces additional risks with regard to input prices and holding inventories.

The contract producer’s output is a good

8

1. Recording of output and trade flows

Recording of international trade flows

2 options:

1. Goods under general merchandise?

2. …or net exports of goods under merchanting?

– Net recording does not align very well to a gross recording of output and intermediate consumption

– BPM6, par.10.42 does not really apply to FGPs

The international flows are to be recorded under general merchandise

9

2. Delineation of FGPs

1. Factoryless versus merchanting

Are companies mainly active in branding also FGPs?

– Reselling goods under the principal’s brand name;

– Is branding transformative or merely to be associated with retailing?

– 2008 SNA research agenda: marketing assets and a broader scope on innovation (product design, which is at present not measured under R&D).

Proposed decision rule: FGPs are substantive IPP investors and >50% of their value added is connected to

IPP, innovation, supply chain management and marketing

10

2. Delineation of FGPs

2. Factoryless versus goods sent for processing

– All goods shipped to (foreign) contractors for processing are not subject to ownership transfer and thus subject to a processing arrangement

Goods sent for processing contains all arrangements under which at least part of the material inputs are provided by the principal.

Source of confusion, also in terms of observation: a narrow and broad view on FGPs

11

A summary of decision points:

Output of the FGP reflects full value of the manufactured good;

Contractor owns the good prior to being transacted;

The international flows are to be recorded under general merchandise;

Delineating FGPs from traders: FGPs are substantive IPP investors and >50% of value added is connected to IPP, innovation, supply chain management and marketing;

Goods sent for processing contains all arrangements under which at least part of the material inputs are provided by the principal.

12